The Theory of the Firm under Perfect Competition (Microeconomics) — Important Questions

59 questions

With answersCBSE format

SUMMARY: This chapter explores the functioning and characteristics of firms operating under perfect competition in microeconomic theory. KEY TOPICS: perfect competition, price taker, market equilibrium, short-run supply curve, long-run supply curve, profit maximization, normal profit, shutdown point, entry and exit of firms, allocative efficiency.

In the long run, if firms in a perfectly competitive industry are making supernormal profits, which of the following sequences correctly describes the adjustment process?

DGovernment intervenes → price is fixed → normal profit restored

Check answerHide answer

Correct answer: Option 2 — New firms enter → supply increases → price falls → normal profit restored

Short Answer Questions10 questions

Q163 Marks

State any four features of a perfectly competitive market.

View sample solutionHide solution

(i) A very large number of buyers and sellers so that no individual can influence the market price. (ii) Homogeneous product — every unit is a perfect substitute for every other. (iii) Free entry and exit of firms in the long run. (iv) Perfect knowledge of prices among all buyers and sellers. A fifth feature often listed: perfect factor mobility.

Q173 Marks

Why is AR equal to MR and both equal to price for a competitive firm?

View sample solutionHide solution

A competitive firm is a price-taker; the market price is constant for it no matter how much it produces. Total revenue = P × Q, so average revenue (TR / Q) = P. Since each extra unit is sold at the same P, marginal revenue (ΔTR / ΔQ) also equals P. Therefore P = AR = MR, giving a perfectly elastic (horizontal) demand curve facing the individual firm.

Q183 Marks

Differentiate between shut-down point and break-even point.

View sample solutionHide solution

Shut-down point: the minimum of AVC; at any price below AVC the firm cannot even cover variable costs and will stop production in the short run. Break-even point: the minimum of ATC; at this price the firm just covers total cost and earns normal profits only. Between these two points the firm continues to produce to cover variable costs and part of fixed costs.

Q193 Marks

State the condition for producer's equilibrium in a perfectly competitive firm.

View sample solutionHide solution

Two conditions: (i) Marginal cost equals marginal revenue — MC = MR. For a competitive firm MR = P, so the condition becomes MC = P. (ii) MC must be rising at the point of equilibrium (i.e. MC cuts MR from below). These together ensure profit maximisation rather than profit minimisation.

Q203 Marks

Why is a perfectly competitive firm's supply curve the part of its MC curve above AVC?

View sample solutionHide solution

In short-run equilibrium the firm produces where MR = MC. Since MR = P, the firm produces the output dictated by its MC curve at each price — but only when P ≥ AVC (otherwise it shuts down and supplies zero). So the supply curve is the rising portion of MC at and above the minimum AVC (the shut-down point); below AVC the supply is zero.

Q213 Marks

What is meant by a 'price taker' in a perfectly competitive market?

View sample solutionHide solution

A price taker is a firm that has no control over the price of the product it sells. It accepts the market price as given, determined by the forces of market demand and supply. Since individual firms are too small relative to the market, they cannot influence the price.

Q223 Marks

State any two characteristics of a perfectly competitive market.

View sample solutionHide solution

Two key characteristics of a perfectly competitive market are: (1) There are a large number of buyers and sellers, so no single participant can influence the market price. (2) The product sold by all firms is homogeneous, meaning goods are identical and perfect substitutes for each other.

Q233 Marks

What is meant by 'normal profit' in the context of perfect competition?

View sample solutionHide solution

Normal profit refers to the minimum level of profit necessary to keep a firm in its current line of production in the long run. It is considered part of the firm's total cost (opportunity cost of the entrepreneur). When a firm earns only normal profit, its economic profit is zero.

Q243 Marks

Explain the condition for profit maximization under perfect competition.

View sample solutionHide solution

A firm maximizes profit when it produces at the output level where Marginal Cost (MC) equals Marginal Revenue (MR), i.e., MC = MR. In perfect competition, MR equals the market price (P), so the condition becomes MC = P. Additionally, the MC curve must be rising at this point to ensure it is a maximum and not a minimum.

Q253 Marks

What is the shutdown point for a firm in the short run under perfect competition?

View sample solutionHide solution

The shutdown point is the price level at which a firm is indifferent between producing and shutting down temporarily. This occurs when the market price equals the minimum Average Variable Cost (AVC). If the price falls below the minimum AVC, the firm cannot cover its variable costs and should shut down production in the short run.

Long Answer Questions6 questions

Q266 Marks

Explain the short-run equilibrium of a firm under perfect competition using diagrams (verbal description).

View sample solutionHide solution

The firm is a price-taker, facing a perfectly elastic (horizontal) demand curve at the market price P. So AR = MR = P. The firm chooses output where MC cuts MR from below: MC = MR = P. Three possible outcomes in the short run: (1) Supernormal profits — if P > ATC at equilibrium output; represented by the rectangle between P and ATC over output Q. (2) Normal profits — if P = ATC at equilibrium; total revenue just covers total cost including normal profit. (3) Losses — if AVC ≤ P < ATC, firm minimises losses by producing and covering part of fixed costs. (4) Shut-down — if P < AVC, firm stops producing. Short-run equilibrium is self-enforcing in that, given the market price, the firm has no incentive to change output. It can become long-run equilibrium only after entry and exit of firms change the market price.

Q276 Marks

Explain the long-run equilibrium of a firm and industry under perfect competition.

View sample solutionHide solution

In the long run, all inputs are variable and entry and exit of firms are costless. A competitive firm's long-run equilibrium requires: P = LMC = minimum LAC, and simultaneously P = SMC = SAC so that short-run and long-run plans coincide. Why does this obtain? If existing firms make supernormal profits, new firms enter, market supply rises and price falls until only normal profits remain. Conversely, if firms incur losses, some exit, supply contracts and price rises until losses disappear. At long-run equilibrium every firm earns only normal profits; it produces at the minimum of its long-run average cost — productively efficient; and P = LMC — allocatively efficient. The industry is said to be in a position where it has the optimal number of firms, each of optimal size. This remains the benchmark against which other market structures are evaluated.

Q286 Marks

Derive the supply curve of a firm under perfect competition from its marginal cost curve.

View sample solutionHide solution

At every price P the competitive firm produces where P = MC and MC is rising. So at price P1 output Q1 = MC−1(P1); at a higher price P2 output Q2 > Q1. Plot price on the Y-axis and output on the X-axis: the locus (P, Q) we trace is simply the rising portion of MC. However, the firm will not produce at any price below the minimum AVC — at such prices it does better to shut down (producing zero and bearing only the fixed costs rather than both fixed and some variable costs). Therefore the supply curve is the portion of MC at and above the minimum AVC (the shut-down point), becoming discontinuous at that point — quantity supplied is zero below AVC and jumps to the corresponding Q at or above it. This is the conceptual basis of the upward-sloping market supply curve in competitive markets.

Q296 Marks

Distinguish between short-run and long-run equilibrium of a firm under perfect competition.

View sample solutionHide solution

Short-run equilibrium: (i) At least one factor is fixed, so we work with SAC / SAVC / SMC. (ii) The firm may earn supernormal profits, normal profits, or losses; it may even shut down if P < minimum AVC. (iii) The number of firms in the industry is fixed — no new entry or exit in the short run. (iv) Equilibrium condition: P = MR = SMC and SMC rising. Long-run equilibrium: (i) All inputs are variable; the firm uses LAC and LMC. (ii) Entry of new firms drives down supernormal profits; exit of firms drives up the price; only normal profits remain. (iii) The firm produces at the minimum LAC, implying productive efficiency. (iv) Equilibrium condition: P = LMC = LAC = SMC = SAC, so both long-run and short-run plans coincide at the normal-profit-only output.

Q306 Marks

Explain why firms earn only normal profits in long-run competitive equilibrium.

View sample solutionHide solution

Normal profit is the minimum return an entrepreneur requires to stay in business — the opportunity cost of entrepreneurship. In the long run entry and exit are free. If existing firms earn supernormal profits (price above LAC), their profits act as a signal; new firms enter the industry, market supply rises and price falls. This continues until supernormal profits are competed away and price just equals minimum LAC. Similarly, losses cause exit, supply falls and price rises until losses disappear. The only steady state is P = minimum LAC where firms earn precisely normal profits. Thus long-run competitive equilibrium is both productively efficient (lowest possible unit cost) and allocatively efficient (P = LMC), while leaving firms with just enough to remain in the industry.

Q316 Marks

Explain the concept of a 'price taker' in a perfectly competitive market. Why is a firm under perfect competition unable to influence the market price, and what does its demand curve look like?

View sample solutionHide solution

In a perfectly competitive market, a firm is called a 'price taker' because it has no control over the price of the product it sells. This is because there are a large number of buyers and sellers in the market, and each individual firm supplies only a very small fraction of the total market output. As a result, no single firm can influence the market price by changing its level of output. The price is determined by the forces of market demand and market supply, and every firm must accept this price as given.

Since the firm accepts the market price as fixed, it can sell any quantity it wishes at that price. This means the demand curve faced by an individual firm under perfect competition is a horizontal straight line (perfectly elastic) at the prevailing market price. This is in contrast to a monopoly or oligopoly where the firm faces a downward-sloping demand curve. The perfectly elastic demand curve reflects the fact that if the firm raises its price even slightly above the market price, it will lose all its customers, as buyers can purchase the same product from other sellers at the lower market price.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): A firm under perfect competition is a price-taker.

Reason (R): Each firm is too small relative to the market to influence the market price.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): The demand curve facing a perfectly competitive firm is perfectly elastic.

Reason (R): The firm can sell any quantity at the prevailing market price.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): In long-run competitive equilibrium, firms earn only normal profits.

Reason (R): Free entry and exit competes away any supernormal profit or loss.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): A perfectly competitive firm's supply curve is its entire marginal-cost curve.

Reason (R): The firm chooses output where price equals marginal cost as long as price is at least as high as minimum AVC.

Show explanationHide explanation

Correct answer: Option 4 —

A is false, but R is true.

Q361 Mark

Assertion (A): Short-run equilibrium of a competitive firm requires P = MC with MC rising.

Reason (R): Together, these are the first- and second-order conditions for profit maximisation.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): Under perfect competition, a firm is called a price taker.

Reason (R): In perfect competition, there are a large number of buyers and sellers, and each firm sells a homogeneous product, so no single firm can influence the market price.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): A perfectly competitive firm maximizes profit by producing the output level where MR equals MC.

Reason (R): In perfect competition, the market price is always greater than marginal revenue for every unit sold.

Show explanationHide explanation

Correct answer: Option 3 —

A is true, but R is false.

Q391 Mark

Assertion (A): In the long run under perfect competition, firms earn only normal profit.

Reason (R): The free entry and exit of firms in the long run drives economic profit to zero, leaving firms with only normal profit.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: In perfect competition, the product is homogeneous across sellers.

Statement 2: Advertising is largely meaningless for a firm producing a homogeneous product.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: The demand curve faced by an individual firm in perfect competition is perfectly elastic.

Statement 2: The market demand curve for the industry is downward sloping.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: At the shut-down point the firm just covers its total variable cost.

Statement 2: Fixed costs in the short run are sunk and do not influence the shut-down decision.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Long-run equilibrium of a competitive firm requires P = LMC = LAC = SMC = SAC.

Statement 2: At this position only normal profits are earned.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Supernormal profits in the short run attract new firms into the industry in the long run.

Statement 2: Sustained losses cause some existing firms to exit the industry in the long run.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: Under perfect competition, a firm is a price taker because it has no control over the market price.

Statement 2: Under perfect competition, a firm can influence the market price by changing its output level.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q461 Mark

Statement 1: In the short run, a perfectly competitive firm will shut down if the market price falls below the minimum average variable cost.

Statement 2: The shutdown point occurs where price equals minimum average total cost.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q471 Mark

Statement 1: A perfectly competitive firm maximizes profit by producing the output level where marginal cost equals marginal revenue.

Statement 2: Under perfect competition, marginal revenue is always equal to the market price.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Case Study / Passage Questions4 questions

Q483 Marks

In a city mandi hundreds of small farmers sell rice of the same quality. No individual farmer can influence the market price — it is determined by the total demand and supply across all farmers. Each farmer decides only how much to bring to the mandi each morning.

Each individual farmer in the mandi acts as a:

APrice setter

BPrice taker

CMonopolist

DOligopolist

The demand curve facing each farmer is:

APerfectly elastic (horizontal)

BDownward sloping

CUpward sloping

DVertical

Why does the individual farmer face a perfectly elastic demand curve?

Show answersHide answers

1. Option 2 — Price taker

2. Option 1 — Perfectly elastic (horizontal)

3. Because each farmer's contribution is a tiny fraction of total supply, any individual quantity change has negligible effect on the market price. From the individual farmer's point of view the market price is a given parameter — selling more does not force the price down, and selling less does not push it up. Hence the demand curve facing the farmer is horizontal at the market price.

Q493 Marks

A competitive firm faces a market price of ₹40 per unit. At its profit-maximising output the firm's ATC is ₹30 and AVC is ₹25. It produces 1000 units.

The firm earns a profit per unit of:

A₹10 loss per unit

B₹10 profit per unit

C₹5 profit per unit

D₹5 loss per unit

Total supernormal profit for 1000 units is:

A₹10 000

B₹20 000

C₹30 000

D₹40 000

What will happen in the long run if the firm earns supernormal profits?

Show answersHide answers

1. Option 2 — ₹10 profit per unit

2. Option 1 — ₹10 000

3. Supernormal profits act as a signal to potential entrants. In the long run new firms enter the industry, market supply shifts rightward, price falls, and supernormal profits shrink. Entry continues until only normal profits remain — P = minimum LAC. The market clears at a lower price and a larger total output.

Q503 Marks

A factory has daily ATC of ₹50 per unit (including ₹20 of AFC) and daily AVC of ₹30 per unit. The prevailing market price has fallen to ₹25 per unit.

The firm should:

AContinue producing and earn profit

BContinue and minimise loss

CShut down and save variable costs

DExpand capacity

The shut-down price for this firm is:

A₹25

B₹30

C₹50

D₹20

Why should the firm shut down in this situation?

Show answersHide answers

1. Option 3 — Shut down and save variable costs

2. Option 2 — ₹30

3. At P = ₹25 < AVC = ₹30, the firm cannot even cover its variable costs; producing would add a loss on top of the fixed-cost loss. Shutting down limits the loss to the fixed costs (₹20 per unit of original capacity). Conceptually, a firm continues to operate in the short run as long as P ≥ AVC; below that, shut-down is rational.

Q514 Marks

In a perfectly competitive market, there are a large number of buyers and sellers trading identical products. No single buyer or seller can influence the market price. Each firm is a price taker, meaning it accepts the market price as given and decides only how much to produce. The demand curve faced by an individual firm is perfectly elastic (horizontal) at the prevailing market price. The firm's total revenue increases proportionally with output, and marginal revenue equals average revenue, both equal to the market price. This structure ensures that no firm earns supernormal profit in the long run, as free entry and exit of firms drives profits to zero, leaving firms earning only normal profit.

In a perfectly competitive market, the demand curve faced by an individual firm is:

ADownward sloping

BUpward sloping

CPerfectly elastic (horizontal)

DPerfectly inelastic (vertical)

In perfect competition, which of the following relationships holds true?

AMR > AR

BMR < AR

CMR = AR = Price

DMR = AR > Price

Why is a firm in a perfectly competitive market called a 'price taker'?

What happens to profit levels in a perfectly competitive market in the long run due to free entry and exit?

Show answersHide answers

1. Option 3 — Perfectly elastic (horizontal)

2. Option 3 — MR = AR = Price

3. A firm in a perfectly competitive market is called a 'price taker' because it cannot influence the market price on its own. Due to a large number of buyers and sellers and homogeneous products, each firm must accept the prevailing market price as given and can only decide the quantity to produce.

4. In the long run, due to free entry and exit of firms, supernormal profits attract new firms into the market, increasing supply and driving down prices until profits return to zero (normal profit). Similarly, losses cause firms to exit, reducing supply and raising prices until remaining firms earn normal profit.

Table-Based Questions4 questions

Q523 Marks

Study the revenue schedule of a competitive firm at P = ₹10 and answer:

Quantity

Price (₹)

TR (₹)

AR (₹)

MR (₹)

1

10

10

10

10

2

10

20

10

10

3

10

30

10

10

4

10

40

10

10

For a perfectly competitive firm:

AAR > MR

BAR = MR = P

CAR < MR

DAR and MR fluctuate

The AR curve of a competitive firm is:

ADownward sloping

BHorizontal at the market price

CUpward sloping

DVertical

Why does TR rise linearly with output in perfect competition?

Show answersHide answers

1. Option 2 — AR = MR = P

2. Option 2 — Horizontal at the market price

3. Because the firm can sell any quantity at the market price, TR rises linearly: TR = P × Q. Average revenue is price and is constant across outputs; marginal revenue is also price because each extra unit brings in the same amount. Hence AR = MR = P — the single most important structural feature of a competitive firm.

Q533 Marks

Study the short-run vs long-run equilibrium comparison and answer:

Item

Short-run

Long-run

At least one fixed factor

Yes

No

Profit outcome

Can be supernormal / normal / loss

Normal profit only

Firms enter / exit

No

Yes

Equilibrium condition

P = SMC, SMC rising

P = LMC = minimum LAC

A firm can earn supernormal profits in the:

AShort-run

BLong-run

CBoth

DNeither

Entry and exit of firms occur in the:

AShort-run

BLong-run

CEither

DNeither

Why does entry and exit drive long-run profits to the normal level?

Show answersHide answers

1. Option 1 — Short-run

2. Option 2 — Long-run

3. In the short run the number of firms is fixed, so supernormal profits or losses can persist. In the long run, entry and exit are free: profits attract entrants; losses drive out weak firms. The process continues until price equals minimum LAC and each firm earns only normal profit — the productive and allocative-efficiency benchmark of perfect competition.

Q546 Marks

Observe the following table showing the cost and revenue data of a firm under perfect competition and answer the questions below:

Output (Units)

Total Revenue (₹)

Total Cost (₹)

Profit/Loss (₹)

0

0

20

-20

1

10

28

-18

2

20

34

-14

3

30

38

-8

4

40

44

-4

5

50

50

0

6

60

58

2

7

70

68

2

8

80

80

0

Q556 Marks

The following table shows the Marginal Cost (MC) and Market Price (P) for a firm under perfect competition. Analyze the data and answer:

Output (Units)

Market Price (₹)

Marginal Cost (₹)

Decision

1

15

8

Expand

2

15

10

Expand

3

15

13

Expand

4

15

15

Equilibrium

5

15

18

Reduce

6

15

22

Reduce

Picture-Based Questions4 questions

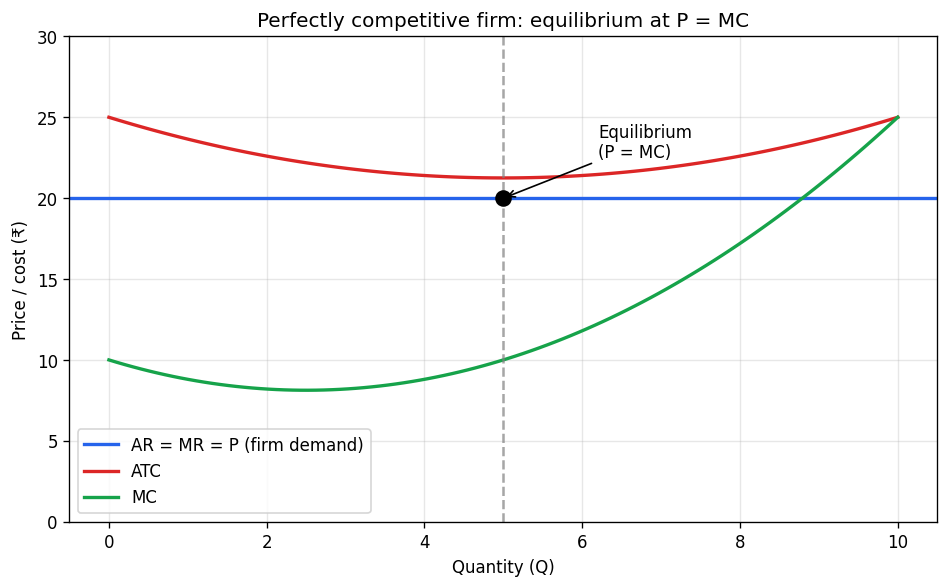

Q563 Marks

Study the equilibrium of a perfectly competitive firm and answer:

The AR = MR curve of the firm is:

AUpward sloping

BDownward sloping

CHorizontal at the market price

DVertical

The profit-maximising condition is reached where:

AP = AR

BP = MC

CP < AVC

DQ = 0

Why is the firm's demand curve perfectly elastic?

Show answersHide answers

1. Option 3 — Horizontal at the market price

2. Option 2 — P = MC

3. A perfectly competitive firm is a price-taker; it can sell any quantity at the market price without influencing that price. Therefore the price line acts as the firm's demand curve and equals both AR and MR. In long-run equilibrium the ATC curve is tangent to this price line at its minimum, so firms earn only normal profits.

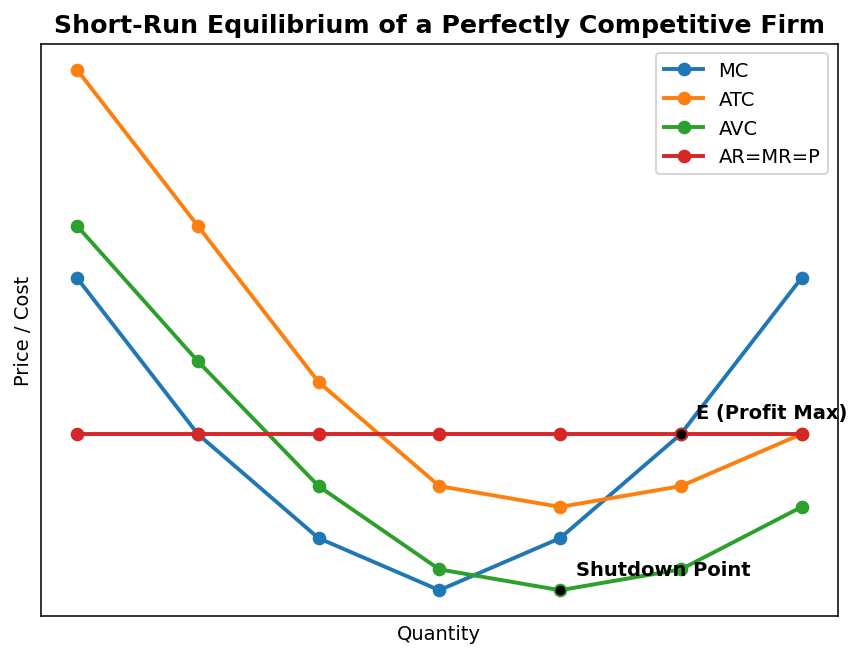

Q574 Marks

Based on the given graph showing the short-run equilibrium of a firm under perfect competition, answer the following:

At what condition does a perfectly competitive firm maximize its profit in the short run?

AP = ATC

BMR = MC

CAR = AVC

DTR = TC

In the graph, the AR = MR = P line is horizontal. What does this indicate about the firm's pricing power?

AThe firm is a price maker

BThe firm can set any price it wants

CThe firm is a price taker and accepts the market price

DThe firm earns supernormal profit always

Identify the shutdown point from the graph and explain its significance for the firm.

If the market price (P) is above the ATC curve at the equilibrium output, the firm earns:

ANormal profit

BSupernormal (abnormal) profit

CLoss

DZero economic profit

Show answersHide answers

1. Option 2 — MR = MC

2. Option 3 — The firm is a price taker and accepts the market price

3. The shutdown point is where the MC curve intersects the minimum of the AVC curve. If the market price falls below the minimum AVC, the firm cannot cover its variable costs and should shut down production in the short run to minimize losses.

4. Option 2 — Supernormal (abnormal) profit

Q584 Marks

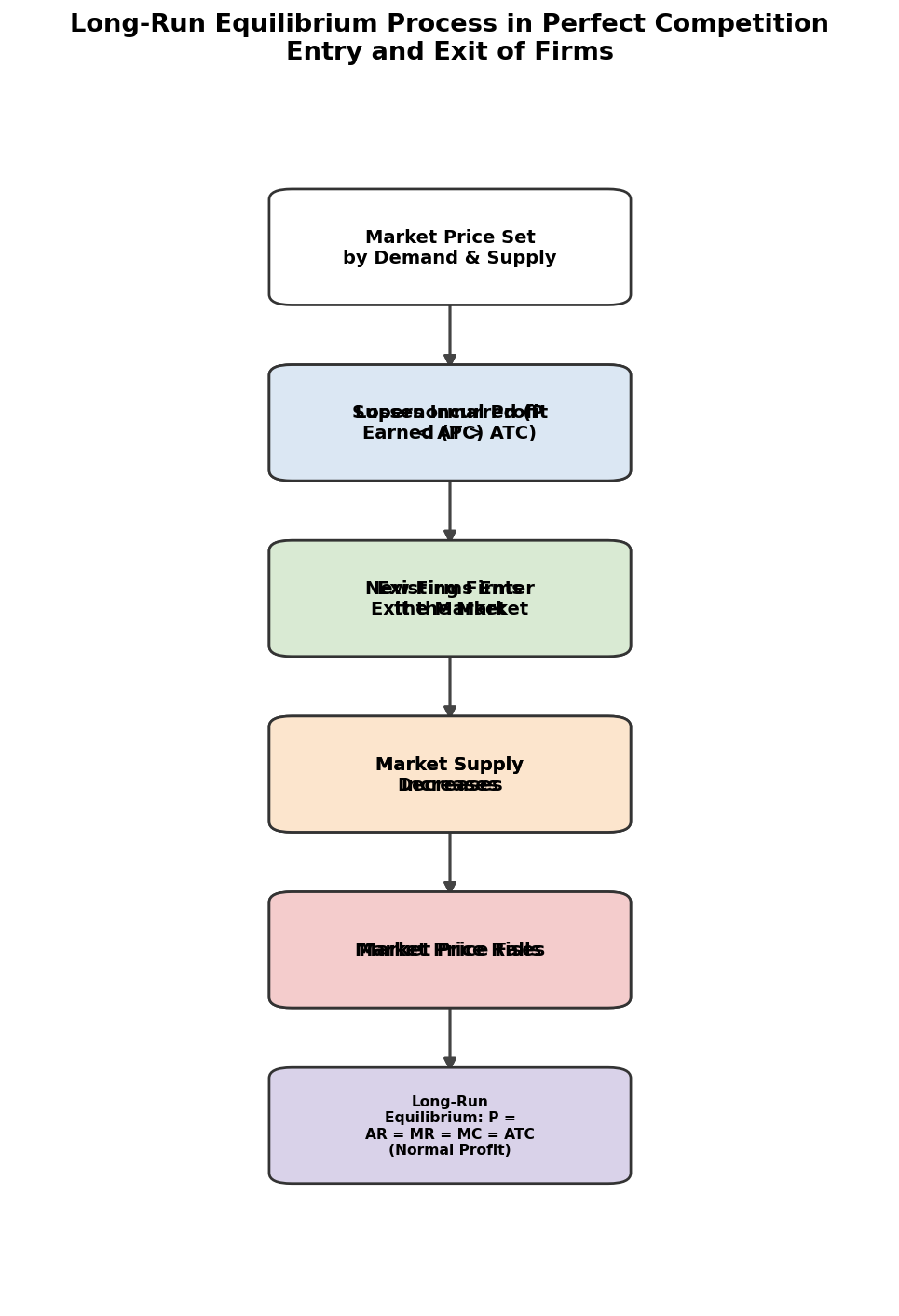

Based on the given flowchart showing the process of long-run equilibrium under perfect competition, answer the following:

According to the flowchart, what happens when firms earn supernormal profit in the short run under perfect competition?

AExisting firms exit the market

BNew firms enter the market

CMarket supply decreases

DMarket price rises

What is the long-run equilibrium condition shown at the bottom of the flowchart? Explain its economic significance.

If firms are incurring losses in the short run, what sequence of events leads to long-run equilibrium as shown in the flowchart?

AEntry of firms → Supply increases → Price falls → Normal profit

BExit of firms → Supply decreases → Price rises → Normal profit

CExit of firms → Supply increases → Price falls → Normal profit

DEntry of firms → Supply decreases → Price rises → Normal profit

What is 'normal profit' in the context of the long-run equilibrium of a perfectly competitive firm?

Show answersHide answers

1. Option 2 — New firms enter the market

2. The long-run equilibrium condition is P = AR = MR = MC = ATC. This means firms earn only normal profit (zero economic profit). It is significant because it ensures allocative efficiency (P = MC) and productive efficiency (P = minimum ATC), with no incentive for further entry or exit.

3. Option 2 — Exit of firms → Supply decreases → Price rises → Normal profit

4. Normal profit is the minimum level of profit required to keep a firm in its current line of production. It is included in the total cost (as opportunity cost of the entrepreneur). In long-run equilibrium, TR = TC (including normal profit), so economic profit is zero.

Q594 Marks

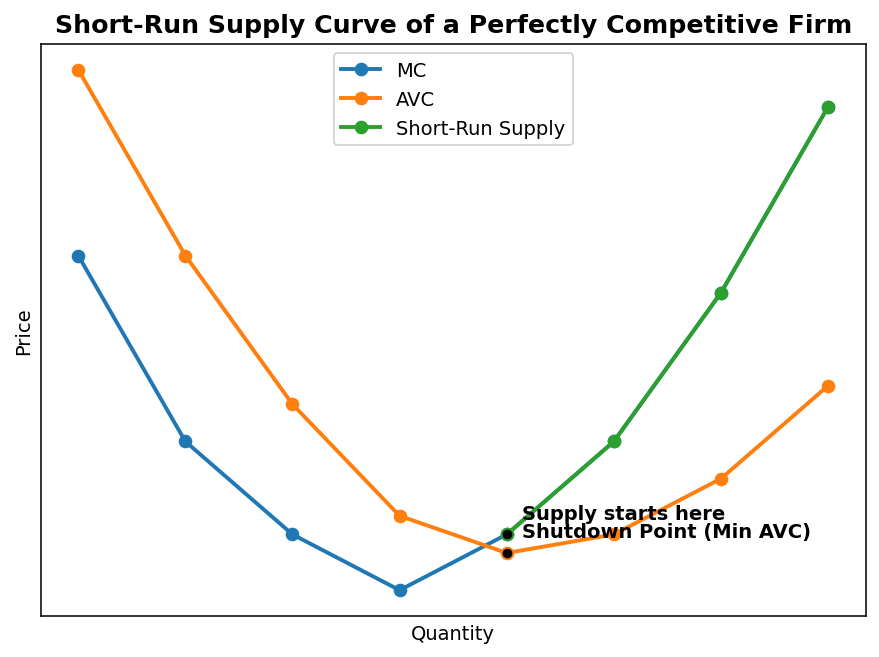

Based on the given graph showing the short-run supply curve of a perfectly competitive firm, answer the following:

The short-run supply curve of a perfectly competitive firm is the portion of the MC curve that lies:

AAbove the minimum point of ATC

BBelow the minimum point of AVC

CAt or above the minimum point of AVC

DEqual to the AR curve

Why does the short-run supply curve of a perfectly competitive firm slope upward?

At a price below the minimum AVC, a rational firm under perfect competition will:

AContinue producing to cover fixed costs

BIncrease production to earn more revenue

CShut down production in the short run

DExit the market permanently

Distinguish between the shutdown point and the break-even point of a firm in the short run.

Show answersHide answers

1. Option 3 — At or above the minimum point of AVC

2. The short-run supply curve slopes upward because it follows the MC curve above the minimum AVC. As output increases, marginal cost rises due to the law of diminishing marginal returns. Since a price-taking firm supplies where P = MC, a higher price induces greater quantity supplied, giving an upward slope.

3. Option 3 — Shut down production in the short run

4. The shutdown point is where P = minimum AVC; below this price, the firm stops production in the short run. The break-even point is where P = minimum ATC; at this price, the firm earns normal profit (zero economic profit). At prices between minimum AVC and minimum ATC, the firm produces but incurs losses.