Production and Costs (Microeconomics) — Important Questions

59 questions

With answersCBSE format

SUMMARY: The chapter "Production and Costs" in Class 11 Economics explores the theory of production and the various costs associated with it in microeconomic terms. KEY TOPICS: production function, short-run and long-run production, law of variable proportions, returns to scale, cost concepts, fixed and variable costs, total cost, average cost, marginal cost, economies and diseconomies of scale.

Correct answer: Option 3 — Marginal product is zero

Q21 Mark

Average Fixed Cost (AFC) curve:

ARises continuously with output

BFalls continuously and approaches zero

CIs U-shaped

DIs horizontal

Check answerHide answer

Correct answer: Option 2 — Falls continuously and approaches zero

Q31 Mark

Marginal Cost (MC) curve cuts Average Cost (AC) curve at:

AMaximum of AC

BMinimum of AC

CAny point

DThe origin

Check answerHide answer

Correct answer: Option 2 — Minimum of AC

Q41 Mark

Returns to scale are studied in the:

AShort run

BLong run

CMarket period

DVery short run

Check answerHide answer

Correct answer: Option 2 — Long run

Q51 Mark

Total Variable Cost (TVC) is:

AZero at zero output

BConstant at all output levels

CNegative at high output

DEqual to TFC

Check answerHide answer

Correct answer: Option 1 — Zero at zero output

Q61 Mark

Which of the following best defines a production function?

AThe relationship between the cost of inputs and the price of outputs

BThe relationship between physical inputs and the maximum output that can be produced

CThe relationship between total revenue and total cost of a firm

DThe relationship between the number of workers and their wages

Check answerHide answer

Correct answer: Option 2 — The relationship between physical inputs and the maximum output that can be produced

Q71 Mark

In the short run, which of the following is considered a fixed factor of production?

ALabour

BRaw materials

CCapital (machinery)

DElectricity consumed in production

Check answerHide answer

Correct answer: Option 3 — Capital (machinery)

Q81 Mark

The Law of Variable Proportions states that as more units of a variable factor are added to a fixed factor, the marginal product will eventually:

AIncrease continuously

BRemain constant throughout

CFirst increase, then diminish

DDiminish from the very first unit

Check answerHide answer

Correct answer: Option 3 — First increase, then diminish

Q91 Mark

Which of the following cost concepts refers to the addition to total cost when one more unit of output is produced?

AAverage Fixed Cost

BAverage Variable Cost

CMarginal Cost

DTotal Variable Cost

Check answerHide answer

Correct answer: Option 3 — Marginal Cost

Q101 Mark

If a firm doubles all its inputs and output more than doubles, this situation is known as:

AConstant returns to scale

BDecreasing returns to scale

CDiminishing returns to a factor

DIncreasing returns to scale

Check answerHide answer

Correct answer: Option 4 — Increasing returns to scale

Q111 Mark

Average Fixed Cost (AFC) curve is typically shaped as a:

AU-shaped curve

BRectangular hyperbola

CStraight horizontal line

DStraight line with a positive slope

Check answerHide answer

Correct answer: Option 2 — Rectangular hyperbola

Q121 Mark

When Marginal Cost (MC) is less than Average Total Cost (ATC), what happens to ATC as output increases?

AATC rises

BATC remains constant

CATC falls

DATC becomes equal to MC immediately

Check answerHide answer

Correct answer: Option 3 — ATC falls

Q131 Mark

In the long run, the distinction between fixed and variable costs:

ABecomes more pronounced

BRemains the same as in the short run

CDisappears, as all costs become variable

DDisappears, as all costs become fixed

Check answerHide answer

Correct answer: Option 3 — Disappears, as all costs become variable

Q141 Mark

A firm's Total Cost (TC) is ₹10,000 when output is zero and ₹15,000 when output is 100 units. Which of the following statements is correct?

ATotal Fixed Cost is ₹15,000 and Total Variable Cost is ₹10,000

BTotal Fixed Cost is ₹10,000 and Total Variable Cost is ₹5,000

CTotal Fixed Cost is ₹5,000 and Total Variable Cost is ₹10,000

DTotal Fixed Cost is zero and Total Variable Cost is ₹15,000

Check answerHide answer

Correct answer: Option 2 — Total Fixed Cost is ₹10,000 and Total Variable Cost is ₹5,000

Q151 Mark

Economies of scale in production arise primarily because of which of the following reasons?

AIncrease in the price of variable inputs as output expands

BSpecialisation of labour, bulk buying of inputs, and efficient use of capital as output increases

CDiminishing marginal productivity of labour in the short run

DRising marginal costs due to overutilisation of fixed factors

Check answerHide answer

Correct answer: Option 2 — Specialisation of labour, bulk buying of inputs, and efficient use of capital as output increases

Short Answer Questions10 questions

Q163 Marks

Distinguish between short run and long run in production.

View sample solutionHide solution

Short run is a time period in which at least one factor of production — typically capital — is fixed while others (usually labour) are variable. Long run is a period long enough for all factors to be varied; there is no distinction between fixed and variable inputs. The short run determines the law of variable proportions; the long run determines returns to scale.

Q173 Marks

State the law of variable proportions.

View sample solutionHide solution

When successive units of a variable input are combined with a fixed amount of other inputs, the marginal product of the variable input first rises, reaches a maximum and then declines, and may eventually become negative. The law holds in the short run and underlies the U-shape of short-run cost curves.

Q183 Marks

Distinguish between fixed cost and variable cost with one example of each.

View sample solutionHide solution

Fixed cost does not change with the level of output in the short run — e.g. rent on factory building, annual insurance premium. Variable cost changes directly with output — e.g. cost of raw materials, power, wages of casual labour. Together they sum to total cost: TC = TFC + TVC.

Q193 Marks

Explain the relationship between Average Product (AP) and Marginal Product (MP).

View sample solutionHide solution

When MP > AP, AP is rising; when MP < AP, AP is falling; when MP = AP, AP is at its maximum. The MP curve therefore cuts the AP curve at AP's maximum point. The logic is that the marginal value 'pulls' the average: any additional unit with above-average productivity raises the average, and below-average pulls it down.

Q203 Marks

Why is the Average Variable Cost (AVC) curve U-shaped in the short run?

View sample solutionHide solution

Because of the law of variable proportions. Initially, extra units of the variable input are spread more efficiently over the fixed factor and AVC falls. Beyond the optimal combination the fixed factor gets overburdened — marginal product of the variable input declines, so cost per unit of output rises and AVC increases. The U-shape reflects first increasing and then decreasing returns.

Q213 Marks

Define production function and state its two main types.

View sample solutionHide solution

A production function shows the technical relationship between inputs used and the maximum output produced from them. The two main types are the short-run production function, where at least one input is fixed, and the long-run production function, where all inputs are variable.

Q223 Marks

Distinguish between fixed costs and variable costs with one example each.

View sample solutionHide solution

Fixed costs are costs that do not change with the level of output in the short run, such as rent of a factory. Variable costs are costs that change directly with the level of output, such as expenditure on raw materials.

Q233 Marks

What is meant by the short run in production theory?

View sample solutionHide solution

The short run is a time period in which at least one factor of production, usually capital, remains fixed and cannot be changed. Only variable inputs like labour can be altered to change the level of output during this period.

Q243 Marks

State the law of variable proportions and identify the three stages it describes.

View sample solutionHide solution

The law of variable proportions states that as more units of a variable input are added to a fixed input, the marginal product of the variable input first increases, then decreases, and eventually becomes negative. The three stages are increasing returns, diminishing returns, and negative returns to the variable factor.

Q253 Marks

What is marginal cost? How is it related to total variable cost?

View sample solutionHide solution

Marginal cost is the addition to total cost when one more unit of output is produced. Since total fixed cost does not change with output, marginal cost equals the change in total variable cost for each additional unit of output produced.

Long Answer Questions6 questions

Q266 Marks

Explain the three stages of the law of variable proportions.

View sample solutionHide solution

Stage I — Increasing returns to the variable factor: MP rises and then equals AP at the point where AP is maximum. Total product rises at an increasing rate; the fixed factor is under-utilised and gets more efficiently combined with the variable factor. Stage II — Diminishing returns: AP and MP both fall but MP remains positive and below AP. Total product continues to rise but at a decreasing rate and reaches its maximum at the end of Stage II. A rational producer operates in this stage because extra units of the variable input still add positively to output. Stage III — Negative returns: MP becomes negative; total product falls. Too much of the variable factor is combined with the fixed factor so productivity drops and output declines. A rational producer never operates in Stage I (inefficient use of fixed factor) or Stage III (negative returns); Stage II is the relevant zone for production decisions.

Q276 Marks

Draw and explain the relationship between Total Product (TP), Average Product (AP) and Marginal Product (MP) curves.

View sample solutionHide solution

Imagine labour on the X-axis and output on the Y-axis. TP rises at an increasing rate, passes through a point of inflection, rises at a decreasing rate, reaches a maximum, and finally falls. AP and MP are derived from TP: AP = TP / L; MP = ΔTP / ΔL. Both AP and MP rise, reach a maximum, and then fall. Key relationships: (i) When MP > AP, AP is rising; (ii) when MP < AP, AP is falling; (iii) MP = AP at the maximum of AP. (iv) MP becomes zero at the maximum of TP, and negative beyond it. (v) The law of variable proportions underlies the inverted-U shape of both MP and AP. Implications: the rational range of production is Stage II — where MP is positive and declining, AP is falling but still positive, TP is rising at a decreasing rate.

Q286 Marks

Discuss returns to scale — increasing, constant, and decreasing.

View sample solutionHide solution

Returns to scale analyse how output responds when all inputs increase by the same proportion, in the long run. (1) Increasing returns to scale — if all inputs double and output more than doubles, the firm enjoys increasing returns. Caused by economies of scale: specialisation, indivisibilities of capital, managerial efficiency, bulk-discount on inputs, learning-by-doing. (2) Constant returns to scale — if output rises exactly in the same proportion as inputs, returns are constant; usually because economies and diseconomies balance. (3) Decreasing returns to scale — if output rises less than in proportion to inputs, the firm faces decreasing returns; caused by diseconomies of scale: managerial limitations, co-ordination problems, bureaucracy, over-extended control. Real-world production functions typically show increasing returns at small scales, constant at medium scales and decreasing at very large scales, giving a U-shaped long-run average cost curve.

Q296 Marks

Explain the concept and derivation of the firm's short-run cost curves — AFC, AVC, ATC and MC.

View sample solutionHide solution

Start with TC = TFC + TVC. Divide by output Q to get: AFC = TFC / Q — a rectangular hyperbola that falls continuously as output rises and approaches zero but never touches the axis. AVC = TVC / Q — U-shaped because of the law of variable proportions: falls as Stage I productivity gains are reaped, reaches a minimum at the most efficient scale of the variable input, then rises. ATC = TC / Q = AFC + AVC — also U-shaped; ATC is always above AVC and the gap between them narrows as AFC shrinks. MC = ΔTC / ΔQ = ΔTVC / ΔQ — U-shaped; MC cuts both AVC and ATC at their respective minimum points. These curves together determine the firm's equilibrium output, shut-down decision and profit status in the short run.

Q306 Marks

Why is the marginal cost curve U-shaped in the short run?

View sample solutionHide solution

MC = ΔTVC / ΔQ. In the short run, as extra units of the variable input are added to the fixed factor the output produced by each extra unit — the marginal product (MP) — first rises and then falls (law of variable proportions). Because MC and MP are inversely related (MC = W / MP for a given wage W), when MP rises MC falls, and when MP falls MC rises. Therefore MC falls initially, reaches a minimum at the point where MP is maximum, and then rises. The resulting U-shape reflects (i) the initial gains from more efficient use of the fixed factor, and (ii) the later overcrowding of the fixed factor by additional variable units. The MC curve is central to supply-curve derivation under perfect competition.

Q316 Marks

Compare fixed and variable factors of production with the help of a table.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): When marginal product exceeds average product, average product is rising.

Reason (R): Marginal product 'pulls' the average product up when it is higher than the average.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Average fixed cost falls continuously as output rises.

Reason (R): Total fixed cost is constant in the short run and is spread over an increasing number of units.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): The marginal cost curve cuts the average variable cost curve at its minimum point.

Reason (R): MC equals AVC at AVC's minimum and lies above it thereafter.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Short-run cost curves are U-shaped because of the law of variable proportions.

Reason (R): All inputs are variable in the short run.

Show explanationHide explanation

Correct answer: Option 3 —

A is true, but R is false.

Q361 Mark

Assertion (A): Returns to scale apply in the long run.

Reason (R): In the long run, all inputs can be varied together.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): In the short run, at least one factor of production remains fixed.

Reason (R): The short run is defined as a period too brief to vary all inputs, so capital or land typically remains constant while labour can be varied.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): Total Fixed Cost (TFC) remains constant regardless of the level of output.

Reason (R): Fixed costs are those costs that do not change with the level of output in the short run, such as rent and insurance premiums.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q391 Mark

Assertion (A): Marginal Cost (MC) is the change in Total Variable Cost when one additional unit is produced.

Reason (R): Since Total Fixed Cost does not change with output, the change in Total Cost due to one more unit equals the change in Total Variable Cost.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: Total product equals the product of average product and the quantity of the variable input.

Statement 2: Average product and marginal product are equal at the point where average product is maximum.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Total fixed cost does not change with the level of output in the short run.

Statement 2: Total variable cost is zero when output is zero.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Marginal cost cuts average variable cost and average total cost at their minima.

Statement 2: Marginal cost is independent of the level of average fixed cost.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Economies of scale drive the downward-sloping portion of the long-run average cost curve.

Statement 2: Diseconomies of scale drive the upward-sloping portion of the long-run average cost curve.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Total revenue is the product of price per unit and the quantity sold.

Statement 2: Marginal revenue is the change in total revenue that results from selling one additional unit.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: The short-run production function refers to a period where at least one factor of production is fixed.

Statement 2: In the long run, all factors of production are variable.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q461 Mark

Statement 1: The Law of Variable Proportions states that as more units of a variable factor are added to a fixed factor, the marginal product always increases.

Statement 2: The Law of Variable Proportions applies only in the long run.

Show answerHide answer

Correct answer: Option 4 —

Both statements are false.

Q471 Mark

Statement 1: Fixed costs remain constant regardless of the level of output produced.

Statement 2: Variable costs are zero when output is zero.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Case Study / Passage Questions4 questions

Q483 Marks

A farmer operates a fixed 5-acre plot of land (the fixed factor). He experiments with different numbers of labourers (the variable factor). Adding the 1st worker raises output by 10 quintals; 2nd by 20; 3rd by 25; 4th by 20; 5th by 10; 6th by 0; 7th worker actually reduces output by 5 quintals.

Total product is maximum at the:

AAt 2nd worker

BAt 3rd worker

CAt 6th worker

DAt 7th worker

The rise in output from worker 1 to worker 3 illustrates:

AConstant returns

BIncreasing returns to the variable factor

CDiminishing returns

DNegative returns

Describe the three stages of the law of variable proportions in this example.

Show answersHide answers

1. Option 3 — At 6th worker

2. Option 2 — Increasing returns to the variable factor

3. Stage I (workers 1-3): MP rises and TP rises at an increasing rate. Stage II (workers 4-6): MP declines but is still non-negative; TP rises at a decreasing rate until the peak at worker 6. Stage III (worker 7 onwards): MP is negative and TP falls. A rational producer operates in Stage II where extra units add positively, but less so than before.

Q493 Marks

A garment firm is considering expanding its operations. If it doubles all inputs — labour, machines, space — output might double (CRS), more than double (IRS), or less than double (DRS). The owner observes three cases at different scales of existing firms in the industry.

When doubling all inputs more than doubles output the firm is enjoying:

AEconomies of scale

BDiseconomies of scale

CLaw of variable proportions

DDivision of labour

Returns to scale apply in the:

AShort-run

BLong-run

CMarket period

DVery-short-run

State any two sources of increasing returns to scale at the startup stage.

Show answersHide answers

1. Option 1 — Economies of scale

2. Option 2 — Long-run

3. Increasing returns at small scales come from specialisation of labour, indivisibility of capital (a machine must be whole), bulk-discounts on inputs, and learning-by-doing. Decreasing returns at very large scales come from managerial diseconomies — coordination, monitoring, bureaucracy. The long-run average cost curve typically shows IRS, then CRS, then DRS as scale grows.

Q503 Marks

A small bakery has a fixed oven and pays rent of ₹10 000 per month (fixed cost). As it bakes more bread, its total variable cost (raw materials, casual wages, fuel) rises. The manager notices that average variable cost first falls, then rises as output increases.

The AFC curve behaves as follows:

ARises continuously

BFalls continuously

CIs U-shaped

DIs horizontal

Marginal cost cuts the average cost curve:

AAt maximum AC

BAt minimum AC

CAt any point

DOnly at zero output

Explain why the AVC curve is U-shaped.

Show answersHide answers

1. Option 2 — Falls continuously

2. Option 2 — At minimum AC

3. U-shape arises from the law of variable proportions. Initially, adding more loaves spreads the fixed oven capacity more efficiently — AVC falls. Beyond the most efficient output level the oven is overstrained — marginal product of further labour drops — so cost per loaf rises and AVC increases. AFC always falls as the fixed cost is spread over more loaves. ATC = AFC + AVC is also U-shaped.

Q514 Marks

A farmer in Punjab uses a fixed piece of land (2 acres) and keeps adding more and more labour to cultivate wheat. Initially, as he adds the first few workers, total output increases at an increasing rate because workers can specialise and divide tasks efficiently. However, after a certain point, adding more workers leads to smaller and smaller increases in output, and eventually, total output may even start to decline. This happens because the fixed factor (land) becomes increasingly scarce relative to the variable factor (labour). This phenomenon is central to understanding short-run production decisions and is one of the most fundamental laws in microeconomics.

The phenomenon described in the passage is known as:

AReturns to Scale

BLaw of Variable Proportions

CLaw of Demand

DEconomies of Scale

In the passage, which factor of production is fixed?

ALabour

BCapital

CLand

DEntrepreneur

What is the stage called when adding more variable inputs leads to a decline in total output?

The initial phase where total output increases at an increasing rate is due to:

ADiminishing marginal returns

BNegative marginal returns

CIncreasing marginal returns due to specialisation

DConstant marginal returns

Show answersHide answers

1. Option 2 — Law of Variable Proportions

2. Option 3 — Land

3. This stage is called the stage of Negative Returns or Stage III of the Law of Variable Proportions, where the Marginal Product (MP) of the variable factor becomes negative, causing Total Product (TP) to fall.

4. Option 3 — Increasing marginal returns due to specialisation

Table-Based Questions4 questions

Q523 Marks

Study the TP AP MP schedule and answer:

Labour (L)

TP

AP

MP

1

10

10

10

2

30

15

20

3

55

18.3

25

4

75

18.8

20

5

85

17

10

6

85

14.2

0

7

80

11.4

-5

TP is at its maximum at the:

A3rd worker

B4th worker

C6th worker

D7th worker

AP reaches its peak at worker number:

A3rd

B4th

C5th

D7th

Describe the MP-AP relationship using the schedule.

Show answersHide answers

1. Option 3 — 6th worker

2. Option 2 — 4th

3. When MP > AP, AP is rising (rows 1-3); when MP < AP, AP is falling (rows 5-7). AP is at its peak at worker 4 where MP = AP = 20 (approximately). Beyond worker 6 MP is negative, so TP falls.

Q533 Marks

Study the short-run cost schedule and answer:

Q

TFC

TVC

TC

AFC

AVC

ATC

MC

1

100

40

140

100

40

140

40

2

100

70

170

50

35

85

30

3

100

95

195

33.3

31.7

65

25

4

100

130

230

25

32.5

57.5

35

5

100

180

280

20

36

56

50

AVC is at its minimum at:

AAt Q = 2

BAt Q = 3

CAt Q = 4

DAt Q = 5

The AFC in the schedule:

ARises continuously

BFalls continuously

CIs U-shaped

DBecomes negative

Explain the behaviour of AFC AVC ATC and MC as output rises.

Show answersHide answers

1. Option 2 — At Q = 3

2. Option 2 — Falls continuously

3. AFC falls because TFC is constant and is spread over a rising output. AVC is U-shaped due to the law of variable proportions — reaches a minimum at Q=3. ATC is also U-shaped and lies above AVC. MC falls, reaches a minimum and then rises, cutting both AVC and ATC at their minima. These typical patterns follow directly from short-run production theory.

Q545 Marks

Compute AC and MC for each output level from the given Total Cost schedule.

Output Q

TC (₹)

1

100

2

140

3

180

4

230

5

290

Q555 Marks

From the Total Product schedule, compute Average Product and Marginal Product.

Labour L

TP

1

10

2

30

3

55

4

75

5

85

6

85

7

80

Picture-Based Questions4 questions

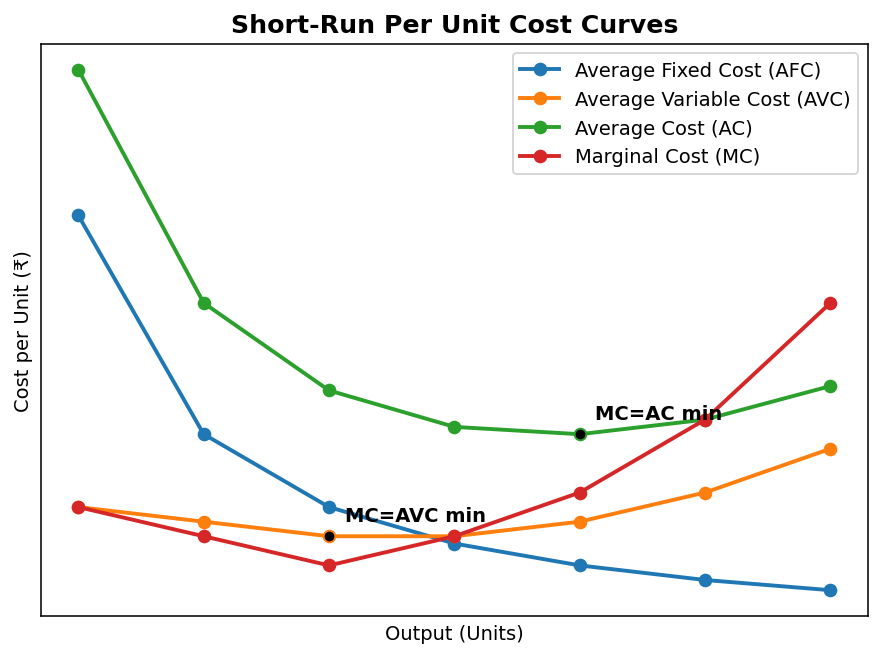

Q563 Marks

Study the short-run cost curves and answer:

Which curve falls continuously as output rises?

AAFC

BAVC

CATC

DMC

The MC curve cuts which curve(s) at the minimum point?

AAFC

BAVC

CATC

DBoth AVC and ATC

Why are the AVC and ATC curves U-shaped?

Show answersHide answers

1. Option 1 — AFC

2. Option 4 — Both AVC and ATC

3. The U-shape of AVC (and hence ATC) arises from the law of variable proportions. Initially, adding more variable input spreads the fixed factor more efficiently, so cost per unit falls. Beyond the optimal combination the fixed factor becomes overutilised, marginal product of the variable input falls, and cost per unit rises — producing the U-shape.

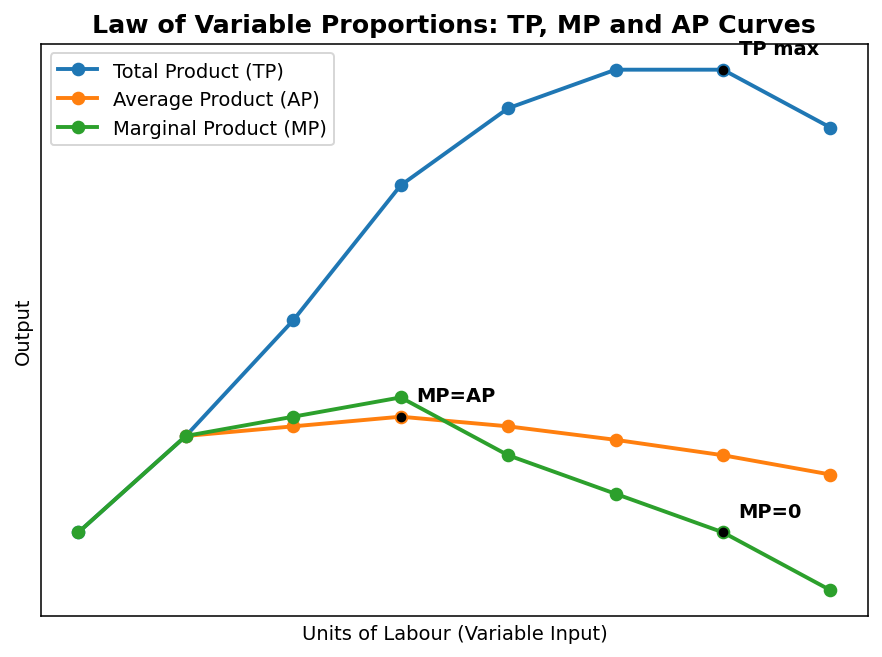

Q574 Marks

Based on the given graph showing the Total Product (TP), Marginal Product (MP), and Average Product (AP) curves, answer the following:

At which unit of labour does the Marginal Product (MP) become zero?

A4th unit

B5th unit

C6th unit

D7th unit

What happens to Total Product (TP) when Marginal Product (MP) becomes negative?

ATP increases at an increasing rate

BTP increases at a decreasing rate

CTP remains constant

DTP starts to decline

Identify the three stages of the Law of Variable Proportions from the graph and state the behaviour of MP in each stage.

At the point where MP = AP (3rd unit), what is the nature of AP?

AAP is falling

BAP is rising

CAP is at its maximum

DAP is zero

Show answersHide answers

1. Option 3 — 6th unit

2. Option 4 — TP starts to decline

3. Stage I (1–3 units): MP is rising (increasing returns to factor). Stage II (3–6 units): MP is positive but falling; TP increases at a decreasing rate (diminishing returns). Stage III (beyond 6 units): MP becomes negative; TP falls (negative returns).

4. Option 3 — AP is at its maximum

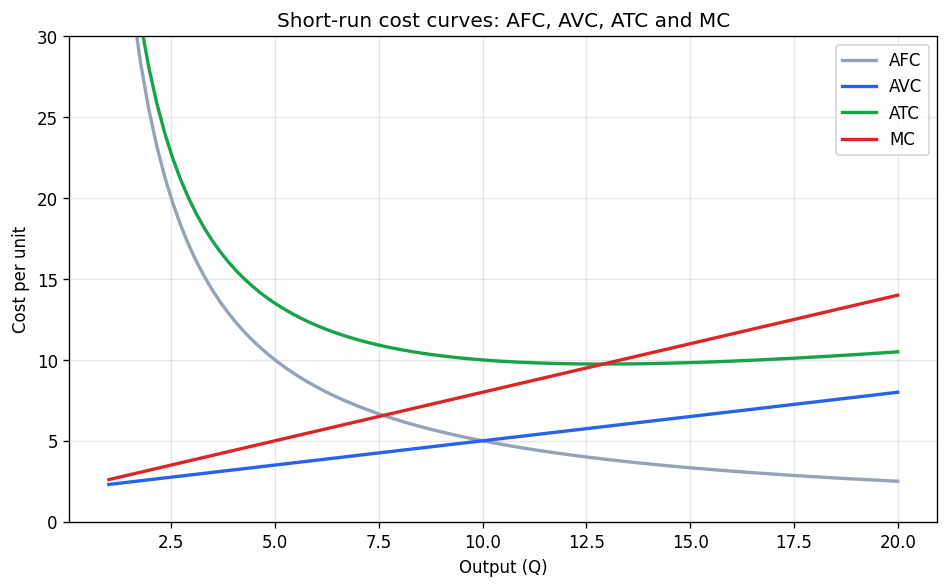

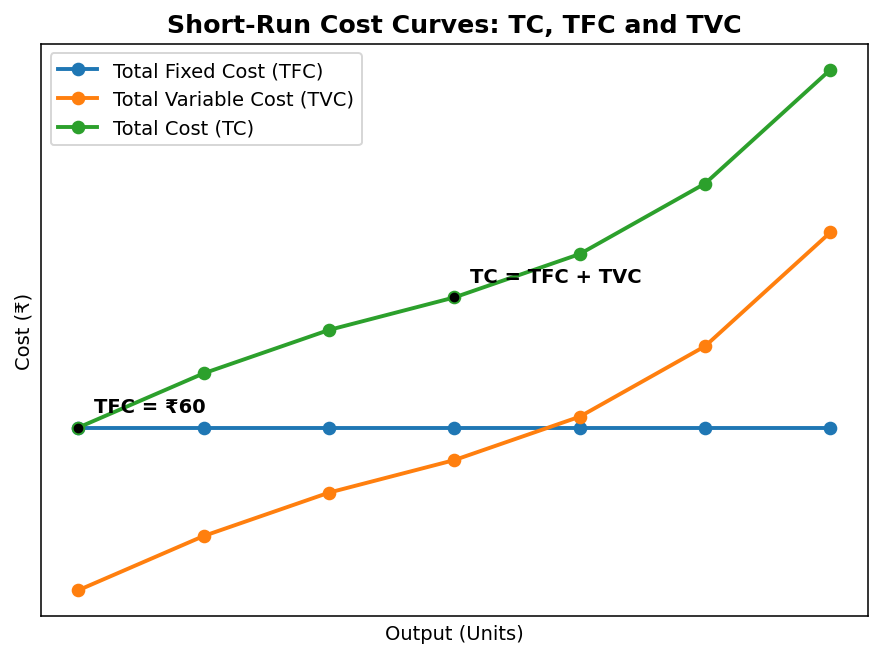

Q584 Marks

Based on the given graph showing Short-Run Cost Curves, answer the following:

Why does the Total Fixed Cost (TFC) curve appear as a horizontal straight line parallel to the X-axis?

ABecause fixed costs increase with output

BBecause fixed costs remain constant regardless of output level

CBecause fixed costs become zero at higher output

DBecause fixed costs are equal to variable costs

What is the value of Total Variable Cost (TVC) when output is zero, and why?

A₹60, because fixed costs are always present

B₹20, because at least one unit is always produced

C₹0, because no variable inputs are used when output is zero

D₹80, because TC is ₹80 at zero output

Calculate the Total Variable Cost (TVC) when output is 4 units, given that TC = ₹124 and TFC = ₹60.

From the graph, the TVC curve is initially concave and then convex to the origin. This shape reflects which economic law?

ALaw of Demand

BLaw of Returns to Scale

CLaw of Variable Proportions

DLaw of Supply

Show answersHide answers

1. Option 2 — Because fixed costs remain constant regardless of output level

2. Option 3 — ₹0, because no variable inputs are used when output is zero

3. TVC = TC – TFC = ₹124 – ₹60 = ₹64. This confirms the value shown in the graph at 4 units of output.

4. Option 3 — Law of Variable Proportions

Q594 Marks

Based on the given graph showing Average Cost (AC), Average Variable Cost (AVC), Average Fixed Cost (AFC), and Marginal Cost (MC) curves, answer the following:

What is the relationship between the Marginal Cost (MC) curve and the Average Cost (AC) curve at the minimum point of AC?

AMC is above AC

BMC is below AC

CMC equals AC

DMC and AC are parallel

Why does the Average Fixed Cost (AFC) curve continuously fall and never touch the X-axis?

From the graph, at which output level does the AVC reach its minimum?

A2nd unit

B3rd unit

C4th unit

D5th unit

Explain why the AC curve is U-shaped.

Show answersHide answers

1. Option 3 — MC equals AC

2. AFC = TFC ÷ Output. Since TFC is constant, as output increases, AFC keeps falling. It never touches the X-axis because TFC is always a positive number; dividing a positive constant by any finite output will never give zero. The AFC curve is a rectangular hyperbola.

3. Option 3 — 4th unit

4. The AC curve is U-shaped due to the Law of Variable Proportions. Initially, AC falls because: (a) AFC falls continuously, and (b) AVC also falls due to increasing returns. After a point, AVC starts rising due to diminishing returns, and its rise outweighs the fall in AFC, causing AC to rise. This gives the AC curve its characteristic U-shape.