1. Option 3 — Perfectly elastic (horizontal)

2. Option 2 — Price = Marginal Cost

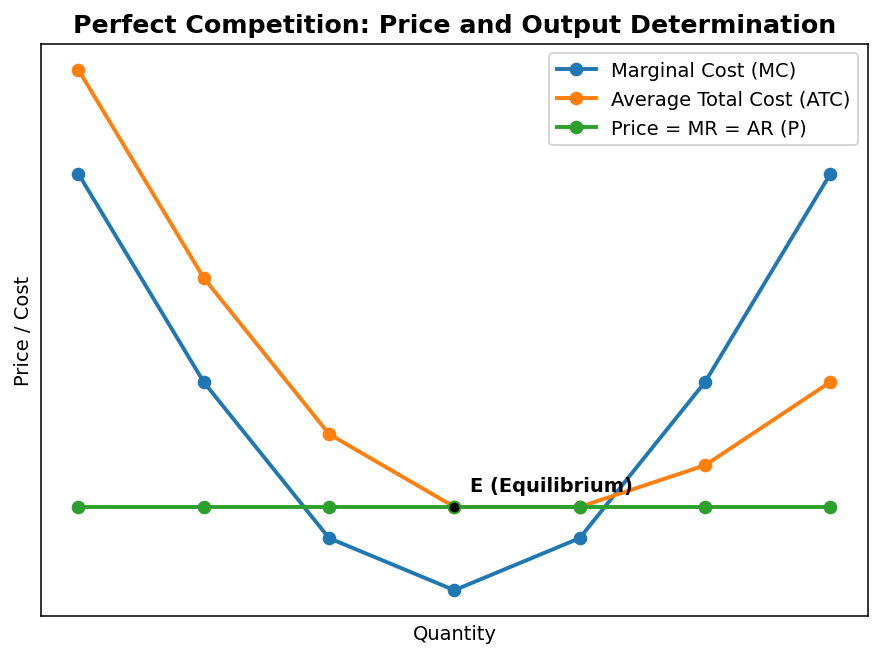

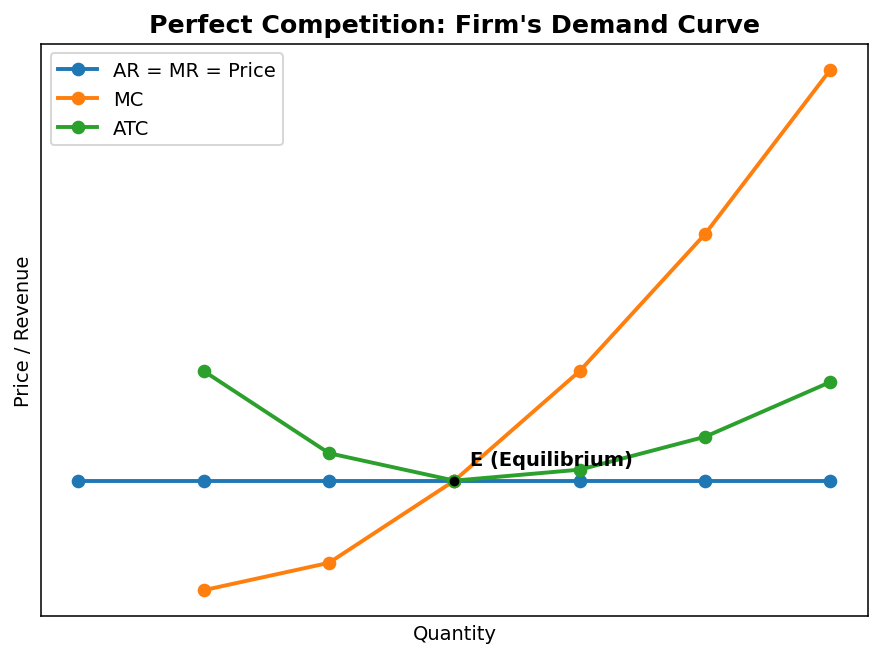

3. At equilibrium point E, Price equals the minimum of ATC (P = ATC), which means the firm earns normal profit (zero economic profit). There is neither supernormal profit nor loss.

4. In the long run, there are no barriers to entry in perfect competition. Supernormal profits attract new firms into the industry, increasing supply, which drives the price down until only normal profits remain (P = minimum ATC).

5. Option 3 — MR = MC

6. Option 3 — The firm is earning supernormal (abnormal) profit

7. In monopoly, the firm faces a downward-sloping demand curve (AR curve). To sell an additional unit, the monopolist must lower the price for all units sold, not just the last one. Therefore, the revenue gained from the extra unit (MR) is less than the price charged (AR). This is why MR lies below AR throughout.

8. Yes, a monopolist can earn supernormal profits even in the long run. This is because high barriers to entry (such as legal restrictions, patents, control over key resources, or economies of scale) prevent new firms from entering the market and competing away the profits. Unlike perfect competition, there is no mechanism to erode monopoly profits in the long run.

9. Option 3 — Downward sloping but relatively elastic

10. Option 2 — Rs. 25

11. In the long run, supernormal profits attract new firms into the market (since entry barriers are low in monopolistic competition). As more firms enter, the demand for each existing firm's product decreases and becomes more elastic. This continues until each firm earns only normal profit (Price = AC), and supernormal profits are eliminated.

12. Product differentiation means each firm sells a product that is slightly different from its rivals in terms of quality, branding, packaging, or features. Because consumers perceive these differences, they may prefer one brand over another and are willing to pay a slightly higher price for it. This gives the firm some control over its price (market power), unlike perfect competition where all products are identical and firms are pure price takers.