Reconstitution of Partnership: Admission of a Partner — Important Questions

58 questions

With answersCBSE format

SUMMARY: This chapter focuses on the changes in the financial structure and accounting treatment when a new partner is admitted into an existing partnership firm. KEY TOPICS: new profit sharing ratio, sacrifice ratio, goodwill treatment, revaluation of assets and liabilities, adjustment of capital accounts, balance sheet preparation, accounting treatment of reserves, adjustment of accumulated profits and losses, capital adjustment methods, journal entries for admission of a partner

Why is goodwill valued at the time of admission of a partner?

View sample solutionHide solution

On admission the existing partners' profit-sharing ratio decreases (they 'sacrifice' part of their share to accommodate the new partner). Goodwill represents the firm's ability to earn excess profits over a normal return — built up over time by the existing partners. The new partner therefore must compensate the old partners for the sacrificed share by paying premium for goodwill in proportion to the sacrifice. This compensation is shared among old partners in the SACRIFICING RATIO.

Q173 Marks

Distinguish between sacrificing ratio and gaining ratio.

View sample solutionHide solution

Sacrificing ratio: the ratio in which OLD partners give up part of their share for the benefit of the new partner; arises on admission. Computed as Old share − New share (positive means sacrifice). Gaining ratio: the ratio in which CONTINUING partners gain from the share of a retiring or deceased partner; arises on retirement/death. Computed as New share − Old share (positive means gain). Goodwill compensation flows to sacrificing partners (admission) or from gaining partners to retiring partner.

Q183 Marks

List the various methods of valuing goodwill.

View sample solutionHide solution

(1) Average profit method — goodwill = average of past profits × number of years' purchase. (2) Super profit method — goodwill = super profit × number of years' purchase, where super profit = average profit − normal profit. (3) Capitalisation of average profit method — goodwill = capitalised value of average profit (at normal rate) − net assets. (4) Capitalisation of super profit method — goodwill = super profit × (100 / normal rate). The choice of method depends on availability of data and the nature of business.

Q193 Marks

How is goodwill brought in by the new partner treated when paid in cash?

View sample solutionHide solution

When the new partner brings in cash for goodwill (premium for goodwill): (1) Cash A/c Dr (with the goodwill amount); To Premium for Goodwill A/c. (Being premium received from new partner.) (2) Premium for Goodwill A/c Dr; To Old Partners' Capital A/c (in their sacrificing ratio). (Being premium distributed to old partners as compensation for sacrifice.) The premium does NOT inflate goodwill on the books — it is purely a transfer to compensate sacrificing partners.

Q203 Marks

What is meant by hidden goodwill and how is it computed?

View sample solutionHide solution

Hidden goodwill arises when the new partner brings capital for his share but the deed does not specify the goodwill explicitly. Working: (i) Compute total capital of new firm based on new partner's capital and his share — total firm capital = new partner's capital × (1 / new partner's share). (ii) Total capital of old partners after admission should be (1 − new partner's share) × total firm capital. (iii) Compare total of OLD partner balances (after revaluation profit/loss adjustment but before goodwill) with the implied figure from step (ii). (iv) The difference is the hidden goodwill — distributed to old partners in sacrificing ratio.

Q213 Marks

Explain the concept of new profit sharing ratio and how it is determined when a new partner is admitted.

View sample solutionHide solution

The new profit sharing ratio is the ratio in which the partners will share the profits and losses of the firm after the admission of a new partner. It is determined by considering the existing partners' profit sharing ratio and the contribution of the new partner, taking into account any sacrifices made by the existing partners.

Q223 Marks

What is the sacrifice ratio and how is it calculated during the admission of a new partner?

View sample solutionHide solution

The sacrifice ratio is the ratio in which existing partners agree to sacrifice their share of profits to accommodate the new partner. It is calculated by determining the difference between the old profit sharing ratio and the new profit sharing ratio for each existing partner.

Q233 Marks

Describe the accounting treatment for revaluation of assets and liabilities upon the admission of a new partner.

View sample solutionHide solution

Upon the admission of a new partner, assets and liabilities are revalued to reflect their current market values. Any increase or decrease in the value of assets or liabilities is recorded in the revaluation account, and the resulting profit or loss is distributed among the existing partners in their old profit sharing ratio.

Q243 Marks

How are accumulated profits and losses adjusted in the capital accounts when a new partner is admitted?

View sample solutionHide solution

Accumulated profits and losses are adjusted in the capital accounts by transferring the balance of these reserves to the partners' capital accounts in their old profit sharing ratio. This ensures that the new partner does not benefit from past profits or losses of the firm.

Q253 Marks

What journal entries are necessary for recording the admission of a new partner?

View sample solutionHide solution

The necessary journal entries include: 1) Recording the cash or assets brought in by the new partner; 2) Adjusting goodwill if applicable; 3) Revaluing assets and liabilities; and 4) Adjusting the capital accounts of existing partners to reflect the changes in profit sharing ratios.

Long Answer Questions6 questions

Q266 Marks

A and B are partners sharing profits in 3:2. They admit C for 1/4 share. Goodwill of the firm is valued at ₹100000. C brings ₹40000 cash for capital and ₹25000 cash for goodwill. Pass journal entries.

View sample solutionHide solution

C's share = 1/4. Sacrificing ratio: A old 3/5 new (3/5 × 3/4) = 9/20; A sacrifices 3/5 − 9/20 = 12/20 − 9/20 = 3/20. B old 2/5 new (2/5 × 3/4) = 6/20; B sacrifices 2/5 − 6/20 = 8/20 − 6/20 = 2/20. Sacrificing ratio A:B = 3:2 (same as old ratio). Journal entries: (1) Cash A/c Dr 65000; To C's Capital A/c 40000; To Premium for Goodwill A/c 25000. (Being capital and premium brought in by C.) (2) Premium for Goodwill A/c Dr 25000; To A's Capital A/c 15000 (3/5); To B's Capital A/c 10000 (2/5). (Being premium distributed to old partners in sacrificing ratio.)

Q276 Marks

X and Y are partners sharing 5:3. They admit Z for 1/4 share. Z is unable to bring goodwill in cash. Goodwill of the firm is valued at ₹120000. Pass journal entries assuming Z's share of goodwill is to be adjusted through capital accounts.

View sample solutionHide solution

Z's share = 1/4. Sacrificing ratio = old (5:3) since old partners sacrifice in old ratio (assuming Z gets share equally from both). Z's share of goodwill = 120000 × 1/4 = ₹30000. Adjustment: debit Z's capital with his share of goodwill and credit old partners in sacrificing ratio (5:3). Journal entry: Z's Capital A/c Dr 30000; To X's Capital A/c (5/8 of 30000) 18750; To Y's Capital A/c (3/8 of 30000) 11250. (Being Z's share of goodwill adjusted through capital accounts since Z could not bring goodwill in cash.) Note: only Z's share of goodwill is adjusted not full 120000.

Q286 Marks

Explain Revaluation Account and its purpose with a numerical example: assets revalued — Building +₹20000, Machinery −₹5000; liabilities — Provision for doubtful debts +₹3000.

View sample solutionHide solution

Revaluation Account is prepared at admission/retirement/death to record changes in the values of assets and liabilities so the new partner is not affected by historical valuations. Format: Dr — losses (decrease in assets, increase in liabilities); Cr — gains (increase in assets, decrease in liabilities). For the data: Cr (gain) Building 20000; Dr (loss) Machinery 5000; Dr (loss) Provision for doubtful debts 3000. Net: Profit on revaluation = 20000 − 5000 − 3000 = ₹12000. This profit is transferred to OLD partners' capital accounts in their OLD profit-sharing ratio (since the gain belongs to the period before admission). The new asset/liability values appear on the new balance sheet.

Q296 Marks

Discuss treatment of accumulated profits/losses and reserves at the time of admission of a partner.

View sample solutionHide solution

Accumulated profits/losses and reserves on the books before admission belong to the OLD partners (they were earned before the new partner joined). At admission they should be transferred to old partners' capital accounts in the OLD profit-sharing ratio. Examples: General Reserve, Profit and Loss A/c (Cr balance), Workmen's Compensation Reserve, Investment Fluctuation Reserve. Journal entry — General Reserve A/c Dr; P&L A/c (Cr) Dr; To Old Partners' Capital A/c (in old ratio). For accumulated losses: Old Partners' Capital A/c Dr; To P&L A/c. The reserves are NOT carried forward to the new firm — they are distributed first.

Q306 Marks

Explain the various methods of valuing goodwill with a numerical example: average profits last 3 years are ₹50000, ₹60000, ₹55000; capital employed ₹500000; normal rate of return 10%. Compute goodwill by (a) average profits method (3 years' purchase) and (b) super profits method (3 years' purchase).

View sample solutionHide solution

Average profit = (50000 + 60000 + 55000) / 3 = ₹55000. (a) Average profits method: Goodwill = Average profit × No. of years' purchase = 55000 × 3 = ₹165000. (b) Super profits method: Normal profit = Capital employed × Normal rate = 500000 × 10% = 50000. Super profit = Average profit − Normal profit = 55000 − 50000 = 5000. Goodwill = Super profit × No. of years' purchase = 5000 × 3 = ₹15000. The two methods give different valuations because the super profits method nets out the normal return and only values the EXCESS earning capacity. The average profits method treats the entire profit as goodwill base hence higher valuation.

Q316 Marks

Differentiate between sacrificing ratio and gaining ratio in tabular form.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): Goodwill is valued at the time of admission of a new partner.

Reason (R): The new partner gains a share at the cost of old partners and must compensate them.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Sacrificing ratio determines the share of goodwill compensation to each old partner.

Reason (R): The amount of sacrifice differs from old partner to old partner depending on the change in their respective shares.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): Revaluation Account profits are transferred to old partners' capital accounts.

Reason (R): Increase or decrease in asset/liability values arose from operations of the period before admission.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Premium for goodwill brought in cash by the new partner is transferred to old partners.

Reason (R): The premium compensates old partners for sacrificing part of their profit share.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Reserves and accumulated profits are distributed before the new partner is admitted.

Reason (R): These belong to the old partners; the new partner has not contributed to building them.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): The new profit sharing ratio is determined by the agreement among all partners at the time of admission.

Reason (R): The new partner's share in profits is based on the existing partners' consent.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): Goodwill can be calculated based on the average profit of the firm.

Reason (R): Goodwill is always based on the future profitability of the firm.

Show explanationHide explanation

Correct answer: Option 3 —

A is true, but R is false.

Q391 Mark

Assertion (A): The sacrifice ratio is calculated to determine how much profit each old partner is sacrificing.

Reason (R): The sacrifice ratio is used to allocate goodwill among old partners.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: Goodwill represents the firm's ability to earn super profits.

Statement 2: Goodwill is intangible but valuable to the firm.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Sacrificing ratio is computed as old share minus new share.

Statement 2: A positive value indicates sacrifice; zero or negative indicates no sacrifice.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Revaluation Account records changes in asset and liability values.

Statement 2: Profit or loss on revaluation goes to old partners in the old profit-sharing ratio.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Hidden goodwill arises when goodwill is not explicitly mentioned in the deed.

Statement 2: It is computed by comparing the implied total capital from the new partner's contribution with the actual total of old partners' capitals.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Goodwill can be valued by average profit super profit and capitalisation methods.

Statement 2: The choice depends on the reliability of profit data and the agreed normal return.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: The new profit sharing ratio is determined by the existing partners' agreement.

Statement 2: Goodwill is not considered when calculating the new profit sharing ratio.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q461 Mark

Statement 1: When a new partner is admitted, the existing partners may have to sacrifice part of their profit share.

Statement 2: The sacrifice ratio is calculated based on the new profit sharing ratio only.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: Goodwill can be adjusted in the capital accounts of the partners upon admission of a new partner.

Statement 2: The revaluation of assets and liabilities is mandatory for all partnerships upon admission of a new partner.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Case Study / Passage Questions4 questions

Q483 Marks

A and B are partners sharing profits in 3:2. They admit C for 1/4 share. The goodwill of the firm is valued at ₹120000. C brings ₹50000 cash for capital and ₹30000 cash for goodwill. Compute the sacrificing ratio and pass entries for the goodwill.

The sacrificing ratio of A and B is:

A3:2

B2:3

CEqual

DOld ratio

Distribution of premium for goodwill (₹30000) to A and B:

AA ₹18000 B ₹12000

BA ₹15000 B ₹15000

CA ₹12000 B ₹18000

DRandom

Pass the journal entries for capital and goodwill.

Show answersHide answers

1. Option 1 — 3:2

2. Option 1 — A ₹18000 B ₹12000

3. Sacrificing ratio: (i) A's old share 3/5; new share = 3/5 × (1 − 1/4) = 3/5 × 3/4 = 9/20; A sacrifices 3/5 − 9/20 = 12/20 − 9/20 = 3/20. (ii) B's old share 2/5; new share = 2/5 × 3/4 = 6/20; B sacrifices 2/5 − 6/20 = 8/20 − 6/20 = 2/20. Sacrificing ratio = 3:2 (same as old since they sacrifice in old ratio). C's share of goodwill = 30000 (cash brought) which is distributed in sacrificing ratio: A 18000 (3/5) and B 12000 (2/5). Journal entries: (1) Cash A/c Dr 80000; To C's Capital 50000; To Premium for Goodwill 30000. (2) Premium for Goodwill A/c Dr 30000; To A's Capital 18000; To B's Capital 12000.

Q493 Marks

M/s Sun Traders past 4 years' profits were ₹60000, ₹70000, ₹80000, ₹90000. Capital employed is ₹400000 and the normal rate of return in the industry is 15%. The new partner is to be admitted with goodwill valued by appropriate methods.

Average annual profit for goodwill calculation =

A₹70000

B₹75000

C₹80000

D₹100000

Super profit (excess over normal return) =

A₹15000

B₹0

C₹6000

D₹60000

Compute goodwill by all four methods.

Show answersHide answers

1. Option 2 — ₹75000

2. Option 1 — ₹15000

3. Average profit = (60000 + 70000 + 80000 + 90000) / 4 = ₹75000. Normal profit (at 15% on capital employed of 400000) = 400000 × 15% = ₹60000. Super profit = Average profit − Normal profit = 75000 − 60000 = ₹15000. Goodwill by methods: (1) Average profit method (3 years' purchase) = 75000 × 3 = ₹225000. (2) Super profit method (3 years' purchase) = 15000 × 3 = ₹45000. (3) Capitalisation of average profit = 75000 / 0.15 = ₹500000; less capital employed 400000 = goodwill ₹100000. (4) Capitalisation of super profit = 15000 / 0.15 = ₹100000. Different methods give different valuations because they differ in what they treat as goodwill base — average profit method is most generous; super profit method is more conservative.

Q503 Marks

X and Y are partners sharing 5:3. They admit Z for 1/4 share. On admission they revalue: Building (book value 200000) to 250000; Machinery (book value 80000) to 70000; create Provision for Doubtful Debts ₹3000 on debtors of ₹50000.

Profit/loss on revaluation is shared in:

AOld ratio

BNew ratio

CEqual

DSacrificing ratio

Net profit on revaluation =

AProfit ₹37000

BLoss ₹37000

CProfit ₹47000

DLoss ₹3000

Prepare the Revaluation Account.

Show answersHide answers

1. Option 1 — Old ratio

2. Option 1 — Profit ₹37000

3. Revaluation Account: Dr (loss items) Machinery (decrease 10000); Provision for Doubtful Debts (3000); Total Dr 13000. Cr (gain items) Building (increase 50000); Total Cr 50000. Net Profit on Revaluation = 50000 − 13000 = ₹37000. Distribution to OLD partners (X and Y) in OLD ratio (5:3 — Z gets nothing as the gain belongs to before-admission period): X = 37000 × 5/8 = 23125; Y = 37000 × 3/8 = 13875. New asset/liability values appear on the new balance sheet. Z is admitted at the new revalued figures so his contribution is fairly priced.

Q513 Marks

When a new partner is admitted into an existing partnership, it often leads to a re-evaluation of the firm's assets and liabilities. This process is crucial as it ensures that the new partner's capital contribution reflects the true value of the partnership. For instance, if the firm has appreciated assets, the revaluation will increase the overall capital of the partnership, which can affect the profit-sharing ratios among the partners. Additionally, the existing partners may need to sacrifice a portion of their profit share to accommodate the new partner, which is calculated through the sacrifice ratio. Goodwill, representing the firm's reputation and customer loyalty, must also be considered and valued appropriately during this transition. The adjustments in capital accounts and the preparation of a revised balance sheet are essential steps to finalize the admission process.

What is the purpose of re-evaluating assets and liabilities when a new partner is admitted?

ATo increase the firm's liabilities

BTo reflect the true value of the partnership

CTo decrease the capital of existing partners

DTo eliminate goodwill from the balance sheet

Explain the concept of sacrifice ratio in the context of admitting a new partner.

Which of the following is NOT considered during the admission of a new partner?

ARevaluation of assets

BAdjustment of capital accounts

CDistribution of accumulated losses

DChange in business location

Show answersHide answers

1. Option 2 — To reflect the true value of the partnership

2. The sacrifice ratio is the proportion in which existing partners give up their share of profits to accommodate the new partner's share.

3. Option 4 — Change in business location

Table-Based Questions4 questions

Q523 Marks

Compare goodwill valuation methods:

Method

Formula

When to use

Average profit

Average profit × No. of years' purchase

Simple, when stable profits

Super profit

Super profit × No. of years' purchase

When excess over normal return

Capitalisation of average profit

(Average profit / Normal rate) − Capital employed

Capital-intensive firms

Capitalisation of super profit

Super profit × (100 / Normal rate)

When normal rate is reliable

Which method gives the highest goodwill valuation?

AAverage profit method

BSuper profit method

CCapitalisation methods

DAll depend on context

Which method requires knowledge of normal rate of return?

AAverage profit only

BSuper profit only

CBoth with normal return

DRandom

Why might different parties prefer different valuation methods?

Show answersHide answers

1. Option 4 — All depend on context

2. Option 3 — Both with normal return

3. Each method has trade-offs. Average profit method is simple and gives higher valuations (treats entire profit as goodwill base). Super profit method is more conservative (only excess over normal return is goodwill). Capitalisation methods convert profit to a notional firm value at the normal rate; goodwill is the excess over actual capital employed (or actual capital at the same rate). Choice depends on (i) data availability — average needs only profit history; super profit needs capital employed and normal rate; (ii) industry conventions; (iii) parties' agreement. Often more than one method is computed and the parties negotiate around them.

Q533 Marks

Treatment of accumulated profits/losses on admission:

Item

Treatment

Distributed in

General Reserve

Distributed to old partners before admission

Old ratio

P&L A/c (Cr balance)

Distributed to old partners

Old ratio

P&L A/c (Dr balance — accumulated loss)

Charged to old partners' capitals

Old ratio

Workmen Compensation Reserve (no liability)

Distributed to old partners

Old ratio

Investment Fluctuation Reserve

Distributed to old partners

Old ratio

Accumulated profits and reserves at admission are:

ACarry forward in new firm

BDistribute to old partners

CDistribute equally

DRandom

These are distributed in the:

AOld ratio

BNew ratio

CCapital ratio

DSacrificing ratio

Why are reserves and accumulated profits distributed to old partners only?

Show answersHide answers

1. Option 2 — Distribute to old partners

2. Option 1 — Old ratio

3. Reserves and accumulated profits/losses on the books before admission belong to the OLD partners — they were earned before the new partner joined. They are distributed to old partners' capital accounts in the OLD profit-sharing ratio. Journal entries: For Cr balance (profits and reserves): General Reserve A/c Dr; P&L A/c Dr (Cr balance); To Old Partners' Capital A/c (in old ratio). For Dr balance (losses): Old Partners' Capital A/c Dr; To P&L A/c. The reserves are NOT carried forward to the new firm. After distribution the books are 'cleaned' so that the new partner's contribution is correctly computed and the new firm starts fresh.

Q546 Marks

A and B are partners sharing 3:2. They admit C for 1/4 share. Compute the sacrificing ratio.

Quantity

Value

A's old share

3/5

B's old share

2/5

C's share at admission

1/4

C is admitted equally from A and B

Yes

Q556 Marks

M/s Sun Traders past 4 years' profits and capital data are below. Compute goodwill by all four methods.

Year

Profit

2020-21

₹60000

2021-22

₹70000

2022-23

₹80000

2023-24

₹90000

Capital employed

₹400000

Normal rate of return

15%

Years' purchase

3

Picture-Based Questions3 questions

Q562 Marks

Based on the given chart, answer the following:

What is the total goodwill amount calculated?

A60000

B80000

C100000

D20000

How much goodwill is attributed to the new partner?

What percentage of profit does Partner A receive?

A50%

B30%

C20%

D40%

How is the profit sharing ratio determined?

Show answersHide answers

1. Option 1 — 60000

2. 20000

3. Option 1 — 50%

4. Based on the agreement between partners

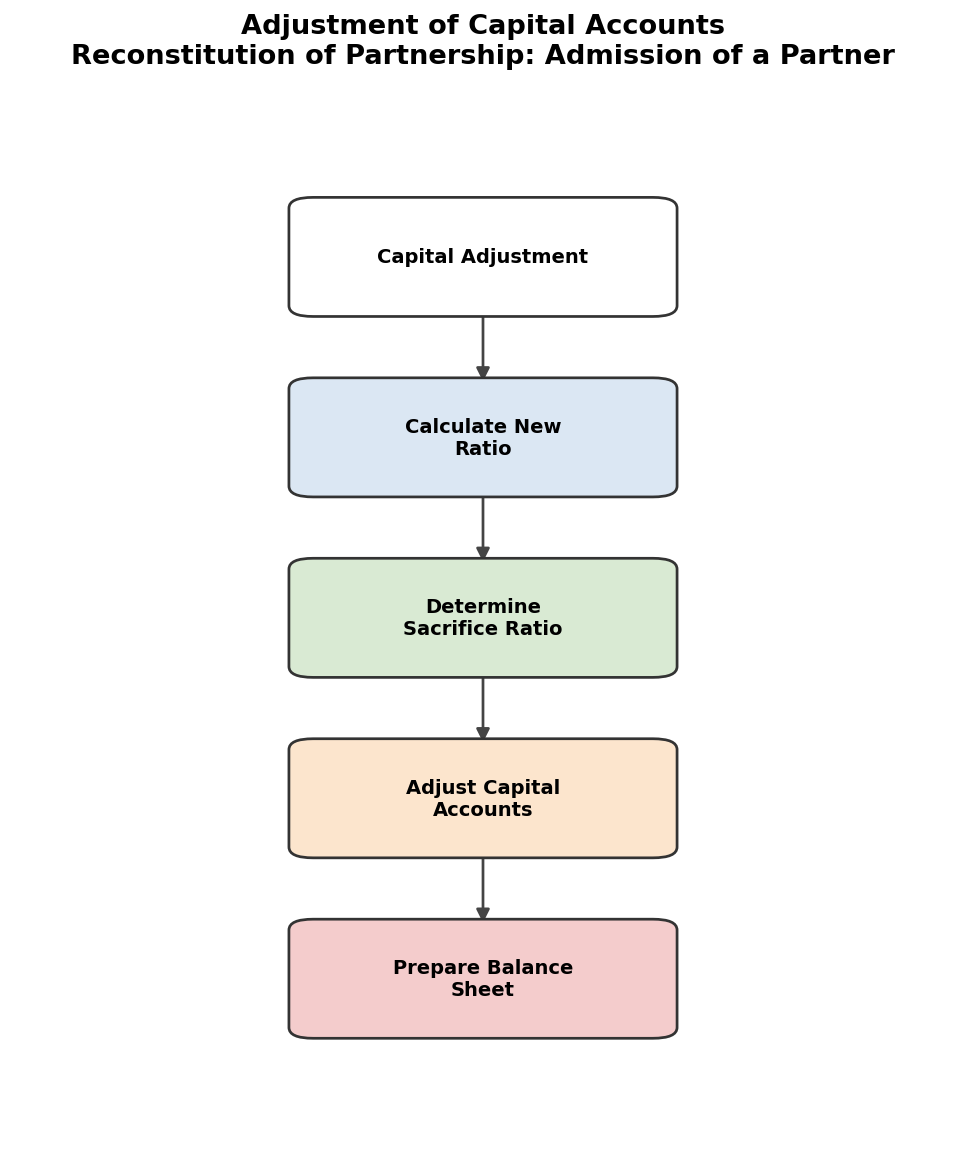

Q572 Marks

Based on the given flowchart, answer the following:

What is the first step in the capital adjustment process?

APrepare Balance Sheet

BCalculate New Ratio

CDetermine Sacrifice Ratio

DAdjust Capital Accounts

What is the final step in the flowchart?

What is the first step in the goodwill treatment process?

ACalculate Goodwill

BIdentify Goodwill

CAdjust Capital Accounts

DRecord in Books

What is the last step in the flowchart?

Show answersHide answers

1. Option 2 — Calculate New Ratio

2. Prepare Balance Sheet

3. Option 2 — Identify Goodwill

4. Record in Books

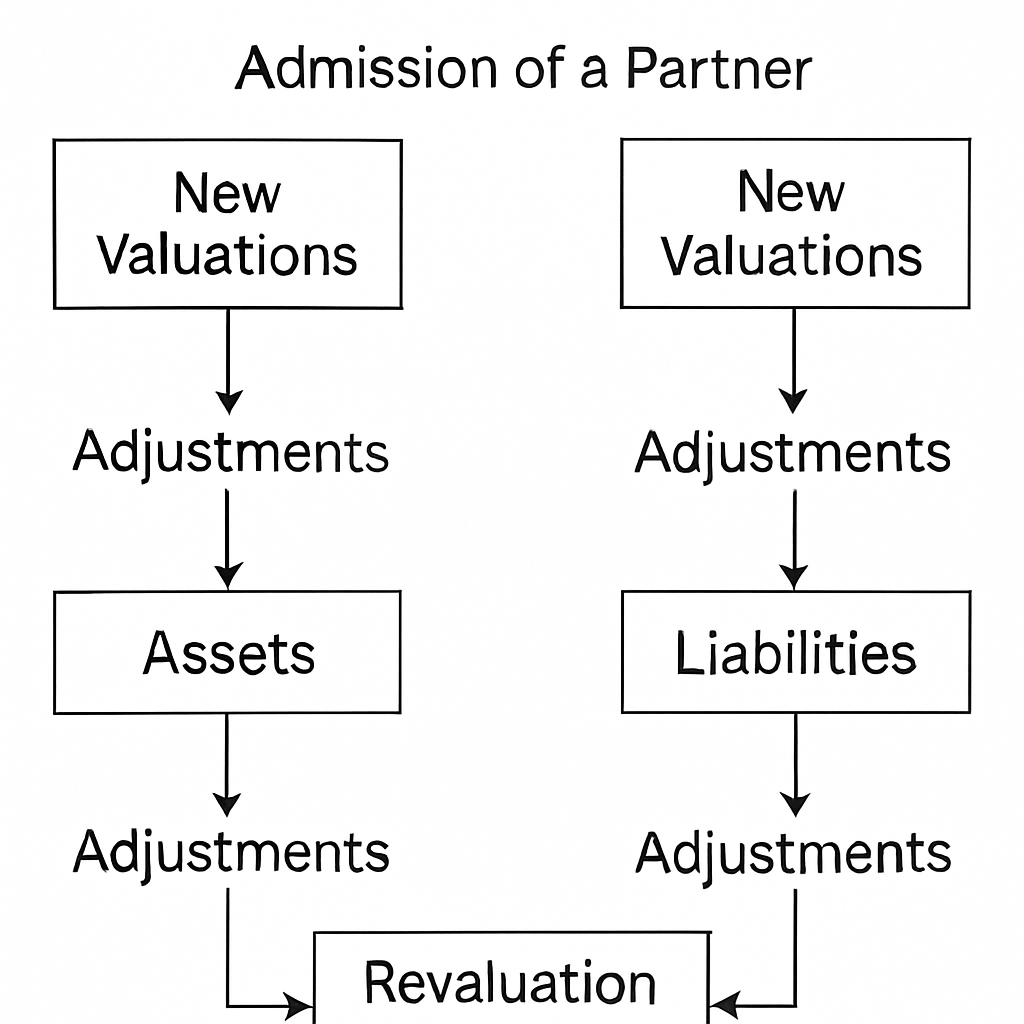

Q582 Marks

Based on the given diagram of revaluation of assets, answer the following:

What is the purpose of revaluation of assets?

ATo increase liabilities

BTo reflect true value

CTo reduce capital

DTo eliminate goodwill

Name one asset that may be revalued during this process.