Reconstitution of Partnership: Retirement and Death of a Partner — Important Questions

58 questions

With answersCBSE format

SUMMARY: This chapter focuses on the accounting treatment and adjustments required when a partner retires or dies in a partnership firm. KEY TOPICS: retirement of a partner, calculation of new profit-sharing ratio, goodwill adjustment, revaluation of assets and liabilities, settlement of retiring partner's dues, death of a partner, executor's account, joint life policy, adjustment of accumulated profits and losses.

At the time of retirement the retiring partner's share of goodwill is paid by:

AOld partners

BContinuing partners (in gaining ratio)

COutsiders

DBank

Check answerHide answer

Correct answer: Option 2 — Continuing partners (in gaining ratio)

Q31 Mark

Joint life policy is taken to:

ACover legal fees

BProvide funds in case of death of a partner

CPay tax

DEarn profit

Check answerHide answer

Correct answer: Option 2 — Provide funds in case of death of a partner

Q41 Mark

Profit/loss to date of death of a partner is computed using:

ATotal profit method

BTime basis or sales basis

CRandom method

DCash basis

Check answerHide answer

Correct answer: Option 2 — Time basis or sales basis

Q51 Mark

On retirement the amount due to retiring partner that is not paid in cash is transferred to:

ACapital A/c

BLoan A/c

CReserve

DDrawings

Check answerHide answer

Correct answer: Option 2 — Loan A/c

Q61 Mark

What is the new profit-sharing ratio after a partner retires, if the remaining partners decide to share profits equally?

A1:1

B2:1

C3:2

D1:2

Check answerHide answer

Correct answer: Option 1 — 1:1

Q71 Mark

When a partner retires, how is the goodwill of the firm typically adjusted?

ABy paying cash to the retiring partner

BBy transferring the goodwill to the remaining partners

CBy recording it as a liability

DBy writing it off completely

Check answerHide answer

Correct answer: Option 2 — By transferring the goodwill to the remaining partners

Q81 Mark

In the case of a partner's death, the profit or loss up to the date of death is usually calculated based on which method?

ACash basis

BAccrual basis

CHybrid basis

DRealisation basis

Check answerHide answer

Correct answer: Option 2 — Accrual basis

Q91 Mark

Which of the following is NOT a typical adjustment made when a partner retires?

ARevaluation of assets

BSettlement of liabilities

CDistribution of accumulated profits

DIssuing new shares

Check answerHide answer

Correct answer: Option 4 — Issuing new shares

Q101 Mark

What is the purpose of creating an executor's account when a partner dies?

ATo distribute the partner's share of profits

BTo settle the deceased partner's debts

CTo manage the estate of the deceased

DTo record the goodwill of the firm

Check answerHide answer

Correct answer: Option 3 — To manage the estate of the deceased

Q111 Mark

When calculating the gaining ratio, which of the following is considered?

AThe amount of capital contributed by each partner

BThe change in profit-sharing ratios among the remaining partners

CThe total assets of the partnership

DThe liabilities of the partnership

Check answerHide answer

Correct answer: Option 2 — The change in profit-sharing ratios among the remaining partners

Q121 Mark

Which of the following statements about joint life policies is true?

AThey are paid to the estate of the deceased partner

BThey are shared equally among all partners

CThey are not considered in partnership accounts

DThey are treated as personal assets of the partners

Check answerHide answer

Correct answer: Option 1 — They are paid to the estate of the deceased partner

Q131 Mark

How is the amount due to a retiring partner who is not paid in cash recorded in the books?

AAs a liability

BAs an asset

CAs an expense

DAs a provision

Check answerHide answer

Correct answer: Option 1 — As a liability

Q141 Mark

What happens to the accumulated profits and losses of a partnership when a partner retires?

AThey are wiped off

BThey are distributed among the remaining partners

CThey are transferred to the retiring partner

DThey remain unchanged

Check answerHide answer

Correct answer: Option 2 — They are distributed among the remaining partners

Q151 Mark

Which of the following is a common method for valuing goodwill when a partner retires?

AAverage profit method

BNet asset method

CCapitalisation method

DAll of the above

Check answerHide answer

Correct answer: Option 4 — All of the above

Short Answer Questions10 questions

Q163 Marks

Distinguish between gaining ratio and sacrificing ratio.

View sample solutionHide solution

Sacrificing ratio (admission): old share − new share; the ratio in which old partners give up part of their share to the new partner. Gaining ratio (retirement/death): new share − old share; the ratio in which continuing partners gain from the share given up by the retiring/deceased partner. Goodwill compensation flows in the relevant ratio: at admission to sacrificing partners; at retirement from gaining partners (continuing) to the retiring partner.

Q173 Marks

Why is goodwill calculated at retirement of a partner?

View sample solutionHide solution

On retirement the retiring partner gives up his share of profit to the continuing partners. He has been part of the firm during the period when goodwill was built up. The continuing partners gain his share and must compensate him for it. The retiring partner's share of goodwill is computed as: Total goodwill × Retiring partner's share. This amount is debited to continuing partners' capital accounts in the gaining ratio and credited to the retiring partner's capital account.

Q183 Marks

Explain how the share of profit/loss to date of death is computed.

View sample solutionHide solution

When a partner dies during the year his share of profit/loss from the start of the year to the date of death must be calculated and credited/debited to his capital account. Two methods: (1) Time basis — assume profits accrue uniformly: share of profit = previous year's profit × (months elapsed / 12) × deceased partner's share. (2) Sales basis (turnover basis) — profit accrues in proportion to sales: share of profit = previous year's profit × (sales to date of death / annual sales) × deceased partner's share. Time basis is simpler; sales basis is more accurate when profits and sales are highly correlated.

Q193 Marks

How is the joint life policy treated at the time of death of a partner?

View sample solutionHide solution

A joint life policy (JLP) is taken on the lives of all partners; the firm pays the premium. On death of a partner the maturity/insurance amount is received by the firm. Treatment: (1) Bank A/c Dr (with insurance amount); To JLP A/c. (Being insurance amount received.) (2) JLP A/c Dr (excess over surrender value if any); To Partners' Capital A/c (in old ratio). (Being JLP profit transferred.) The deceased partner's share of the JLP is credited to his capital account.

Q203 Marks

List the items credited to the executor's account on death of a partner.

View sample solutionHide solution

Items credited to the executor's account (representing the deceased partner): (1) Capital balance on date of death; (2) Share of accumulated profits and reserves; (3) Share of profit on revaluation of assets and liabilities; (4) Share of profit/loss to date of death; (5) Share of goodwill from continuing partners; (6) Share of joint life policy; (7) Salary or interest on capital up to date of death; (8) Drawings (if any) deducted (debited). The total represents the amount payable to the executor — settled through cash/bank or transferred to a loan account.

Q213 Marks

What is the significance of calculating the new profit-sharing ratio when a partner retires?

View sample solutionHide solution

The new profit-sharing ratio is significant as it determines how the remaining partners will share the profits and losses of the firm after the retirement of a partner. It reflects the adjustments made to the equity among the partners and ensures fair distribution based on their new contributions or agreements.

Q223 Marks

Describe the process of revaluation of assets and liabilities when a partner retires.

View sample solutionHide solution

Revaluation of assets and liabilities involves assessing the current market value of the firm's assets and liabilities at the time of a partner's retirement. Any increase or decrease in value is adjusted in the capital accounts of the partners, ensuring that the retiring partner receives their fair share based on the updated values.

Q233 Marks

What adjustments are made for accumulated profits and losses upon the retirement of a partner?

View sample solutionHide solution

Upon the retirement of a partner, accumulated profits and losses are adjusted in the capital accounts of the remaining partners. The retiring partner's share of these accumulated profits or losses is calculated and settled, ensuring that the financial position of the firm reflects the accurate contributions of each partner.

Q243 Marks

How is the goodwill of the firm calculated at the time of a partner's retirement?

View sample solutionHide solution

Goodwill is calculated based on the average profits of the firm over a specified period, usually three to five years, multiplied by a certain number of years' purchase. This value is then adjusted among the remaining partners and the retiring partner, reflecting their respective shares in the firm.

Q253 Marks

Explain the term 'executor's account' in the context of a partner's death.

View sample solutionHide solution

An executor's account is a financial statement prepared to settle the affairs of a deceased partner. It includes all assets, liabilities, and the share of profits or losses up to the date of death, ensuring that the deceased partner's dues are accurately calculated and paid to their legal heirs or executors.

Long Answer Questions6 questions

Q266 Marks

P, Q and R are partners sharing 4:3:2. R retires. Goodwill of the firm is valued at ₹90000. The new ratio of P and Q is 5:4. Pass journal entries for goodwill treatment.

View sample solutionHide solution

R's share of goodwill = 90000 × 2/9 = ₹20000. Gaining ratio of P and Q = New − Old. P: new 5/9 − old 4/9 = 1/9. Q: new 4/9 − old 3/9 = 1/9. Gaining ratio = 1:1. Journal entry: P's Capital A/c Dr 10000 (1/2 of 20000); Q's Capital A/c Dr 10000 (1/2 of 20000); To R's Capital A/c 20000. (Being R's share of goodwill borne by P and Q in gaining ratio 1:1.) Total firm goodwill is not raised in books — only the retiring partner's share is adjusted via continuing partners' capital accounts.

Q276 Marks

X, Y and Z are partners sharing equally. X dies on 30 June 2024. The previous year's profit was ₹120000. Sales for that year were ₹600000; sales from 1 April to 30 June 2024 were ₹150000. Compute X's share of profit to date of death by (a) time basis and (b) sales basis.

View sample solutionHide solution

(a) Time basis: Period 1 April to 30 June 2024 = 3 months. X's share of profit = 120000 × (3/12) × (1/3) = 120000 × 0.25 × 0.333 = ₹10000. Assumes profits accrue uniformly through the year. (b) Sales basis: X's share of profit = 120000 × (150000 / 600000) × (1/3) = 120000 × 0.25 × 0.333 = ₹10000. Both methods give the same answer in this case because sales also accrued uniformly (3/12 of annual sales in 3 months). When sales are seasonal the two methods give different results — sales basis is preferred since profits track sales more closely than time.

Q286 Marks

A, B and C are partners sharing 3:2:1. C retires. The firm's balance sheet on retirement date shows: goodwill ₹30000 (previously valued); machinery ₹50000 (revalued at ₹60000); investments ₹40000 (revalued at ₹35000); creditors ₹20000 (provision needed ₹2000). Show Revaluation Account and explain treatment of existing goodwill.

View sample solutionHide solution

Existing goodwill of ₹30000 must be WRITTEN OFF first by debiting all partners' capital accounts in old ratio (3:2:1): A 15000; B 10000; C 5000. (Goodwill is not raised in books at retirement — only adjusted between continuing and retiring partners.) Revaluation Account: Cr (gain) Machinery 10000 (50000→60000); Dr (loss) Investments 5000; Dr (loss) provision for creditors 2000. Net profit on revaluation = 10000 − 5000 − 2000 = ₹3000. Distributed to ALL partners (including retiring) in old ratio: A 1500; B 1000; C 500. C's capital account is then settled with all due credits and the balance paid in cash or transferred to loan account.

Q296 Marks

Explain how the retiring partner is paid: the various methods of settlement.

View sample solutionHide solution

The amount due to the retiring partner (capital balance + accumulated profits + revaluation profit + goodwill share + JLP share − drawings) can be settled in several ways: (1) Lump sum cash payment — entire amount paid immediately; reduces firm cash. (2) Transfer to retiring partner's loan account — converts capital obligation into a loan; the firm pays interest (typically 6% p.a. unless otherwise agreed); paid in instalments. (3) Annuity — equal periodic payments for a fixed term; capital and interest combined. (4) Combination — part lump sum and part loan/annuity. The choice depends on the firm's cash availability and the retiring partner's preference. The accounting entry: Retiring Partner's Capital A/c Dr; To Cash/Bank A/c (cash portion); To Retiring Partner's Loan A/c (deferred portion).

Q306 Marks

Discuss the treatment of joint life policy at retirement and at death of a partner.

View sample solutionHide solution

Joint Life Policy (JLP) is taken to provide funds at retirement or death. Two accounting approaches: (1) Premium charged to P&L A/c — JLP premium is treated as expense; on retirement the surrender value is shared by all partners in old ratio; on death the maturity amount is shared similarly. (2) JLP shown as an asset — premium is debited to JLP A/c; surrender value adjusted yearly; on retirement surrender value distributed to all partners; on death maturity (typically higher than surrender) distributed. At retirement the partner gets his share of the surrender value (his share of the asset). At death the deceased partner's share of maturity goes to his executor; continuing partners get their respective shares too. JLP smooths the financial impact of partner exits.

Q316 Marks

Compare admission of a partner and retirement of a partner with the help of a table.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): Gaining ratio is computed as new share minus old share.

Reason (R): The continuing partners' shares increase when one partner retires; the difference shows the gain.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): The retiring partner's share of goodwill is paid by continuing partners in the gaining ratio.

Reason (R): Continuing partners gain the retiring partner's share so they must compensate him for the share of goodwill earned during his tenure.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): A joint life policy is taken to provide funds in the event of death of a partner.

Reason (R): The maturity amount can be used to pay the deceased partner's executor without straining firm cash.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): The deceased partner's share of profit to date of death is computed and credited to his capital account.

Reason (R): The share belongs to the deceased's estate and must be paid to the executor.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Amount due to retiring partner not paid immediately is transferred to a loan account.

Reason (R): Such amounts earn interest at 6% per annum unless otherwise agreed.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): The new profit-sharing ratio is determined after the retirement of a partner.

Reason (R): The new profit-sharing ratio reflects the remaining partners' agreement on how future profits will be shared.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): Goodwill is not adjusted when a partner retires from the partnership.

Reason (R): Goodwill represents the value of the business and is adjusted to reflect the retiring partner's share.

Show explanationHide explanation

Correct answer: Option 4 —

A is false, but R is true.

Q391 Mark

Assertion (A): The executor's account is prepared to settle the dues of a deceased partner.

Reason (R): The executor's account helps in distributing the deceased partner's share among the legal heirs.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: A partner can retire by giving notice or as per agreement.

Statement 2: Death dissolution and admission also reconstitute the partnership.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: The continuing partners share the retiring partner's share in the gaining ratio.

Statement 2: If the new ratio is not given the gaining ratio is taken as the old ratio of continuing partners.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Goodwill at retirement is computed using the same methods as at admission.

Statement 2: Average profit and super profit methods are commonly used.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: The executor's account represents the deceased partner.

Statement 2: The executor receives all amounts due to the deceased.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: JLP can be treated as an asset or as expense charged to P&L.

Statement 2: Both methods provide some financial cushion at retirement or death.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: Goodwill is not considered during the retirement of a partner.

Statement 2: The new profit-sharing ratio is determined after the retirement of a partner.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q461 Mark

Statement 1: The profit-sharing ratio must be recalculated after a partner's death.

Statement 2: Revaluation of assets is not necessary upon the retirement of a partner.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q471 Mark

Statement 1: The retiring partner's dues must be settled immediately upon retirement.

Statement 2: Accumulated profits and losses are adjusted in the new profit-sharing ratio.

Show answerHide answer

Correct answer: Option 4 —

Both statements are false.

Case Study / Passage Questions4 questions

Q483 Marks

P, Q and R are partners sharing 4:3:2. P retires. The new ratio of Q and R is 5:4. Goodwill of the firm is valued at ₹90000. P's share of goodwill is to be paid by Q and R in their gaining ratio.

Gaining ratio of Q and R =

AEqual

B1:1

C5:4

D4:3

P's share of goodwill and its payment:

AP's share = 4/9 = 4/9 × 90000 = ₹40000

BP's share = 4/9 × 90000 = ₹40000

CP's share is ₹40000 paid by Q ₹20000 and R ₹20000

DBoth 2 and 3

Pass the journal entry for goodwill treatment at retirement.

Show answersHide answers

1. Option 2 — 1:1

2. Option 4 — Both 2 and 3

3. P's share = 4/9. Old shares Q = 3/9 R = 2/9. New shares Q = 5/9 R = 4/9. Gaining ratio (new − old): Q gains 5/9 − 3/9 = 2/9; R gains 4/9 − 2/9 = 2/9. Gaining ratio = 1:1. P's share of goodwill = 90000 × 4/9 = ₹40000. Q's share of payment = 40000 × (1/2) = 20000; R's share = 40000 × (1/2) = 20000. Journal entry: Q's Capital A/c Dr 20000; R's Capital A/c Dr 20000; To P's Capital A/c 40000. The total firm goodwill (90000) is NOT recorded in the books — only the retiring partner's share is settled through capital adjustments.

Q493 Marks

X Y and Z are partners sharing equally. X dies on 30 September 2023 (end of Q2). The previous year's profit was ₹120000. The firm uses time basis for computing profit to date of death.

The method specified is:

ATime basis

BSales basis

CStock basis

DRandom

X's share of profit to 30 September is:

A₹10000

B₹20000

C₹40000

D₹120000

Calculate X's share of profit to date of death and explain the treatment.

Show answersHide answers

1. Option 1 — Time basis

2. Option 2 — ₹20000

3. Time basis assumes profits accrue uniformly throughout the year. From 1 April 2023 to 30 September 2023 = 6 months = 0.5 of the year. Estimated profit for the half-year (extrapolating prior year) = 120000 × 0.5 = ₹60000. X's share (1/3 of the firm) = 60000 × 1/3 = ₹20000. This amount is credited to X's capital account. Alternative: sales basis would use actual sales to date of death vs annual sales of prior year. Both methods are estimates — the firm's actual profit for the period may differ. The deceased's executor receives this amount as part of the final settlement along with capital balance reserves goodwill share and JLP.

Q503 Marks

M/s Crown Stores took a Joint Life Policy of ₹500000 on the lives of all 3 partners A B and C (sharing 3:2:1). The premium for the year was ₹15000. The firm treats JLP as an asset (carries it on balance sheet at surrender value). Surrender value at year-end is ₹120000.

If JLP is treated as an asset it appears on balance sheet at:

ACharge to P&L

BAsset on balance sheet

CLiability

DCash equivalent

At retirement of a partner the firm receives:

AMaturity amount

BSurrender value

CInsurance amount

DPremium paid

Discuss the two methods of JLP treatment and the implication at retirement vs death.

Show answersHide answers

1. Option 2 — Asset on balance sheet

2. Option 2 — Surrender value

3. JLP treatment options: (1) Charge premium to P&L A/c — premium is expensed yearly; on retirement firm receives surrender value (shared by all in old ratio); on death firm receives maturity (shared similarly). (2) Treat JLP as an asset — premium paid is debited to JLP A/c; surrender value adjusted yearly; balance sheet shows JLP at current surrender value. On retirement: surrender value is realised and shared by all in old ratio (3:2:1) — A 60000 B 40000 C 20000. On death (say A dies): maturity amount ₹500000 is received. After deducting surrender value already booked the gain is shared. Typically the deceased's share of the gain is credited to his executor; the rest to surviving partners. JLP smooths the financial impact of partner exits.

Q513 Marks

In a partnership firm, the retirement of a partner necessitates several accounting adjustments to ensure fairness among the remaining partners. When a partner retires, the firm must first calculate the new profit-sharing ratio among the continuing partners. This ratio is essential for determining how profits and losses will be shared moving forward. Additionally, the goodwill of the firm must be adjusted to reflect the retiring partner's share, which is often valued and compensated accordingly. Furthermore, a revaluation of the firm's assets and liabilities is conducted to ascertain their current values, which may differ from their book values. This process ensures that the retiring partner receives a fair settlement based on the updated financial position of the firm. Finally, any accumulated profits or losses must be adjusted in the accounts to reflect the changes brought about by the retirement.

What is the first step that needs to be taken when a partner retires?

ACalculate the goodwill

BCalculate the new profit-sharing ratio

CRevalue the assets and liabilities

DDistribute accumulated profits

Explain the significance of adjusting goodwill when a partner retires.

Why is it necessary to revalue the assets and liabilities of the firm upon a partner's retirement?

Show answersHide answers

1. Option 2 — Calculate the new profit-sharing ratio

2. Adjusting goodwill is significant as it ensures that the retiring partner is compensated fairly for their share of the firm's intangible assets, reflecting their contribution to the firm's value.

3. Revaluing assets and liabilities is necessary to provide an accurate financial position of the firm, ensuring that the retiring partner receives a fair settlement based on the current values.

Table-Based Questions4 questions

Q523 Marks

Items credited to executor's account on death of a partner:

Item

Treatment

Capital balance on date of death

Credit to executor

Share of accumulated profits and reserves

Credit (in old ratio)

Share of revaluation profit

Credit (in old ratio)

Share of goodwill from continuing partners

Credit (paid by gaining partners)

Share of joint life policy

Credit (in old ratio)

Share of profit to date of death

Credit (estimated)

Salary/interest up to date of death

Credit

The executor's account receives:

AGoodwill share

BCapital balance

CSalary up to death

DAll of these

Share of goodwill is paid in:

AOld ratio

BNew ratio

CCapital ratio

DEqual

Explain the computation of the amount payable to the executor.

Show answersHide answers

1. Option 4 — All of these

2. Option 1 — Old ratio

3. The executor represents the deceased partner's estate. The amount payable to the executor is computed by adding all items due to the deceased and deducting any items receivable from him (typically drawings only). The total is settled either as a lump sum from the firm's cash or transferred to a loan account on which interest is paid (typically 6% p.a.). The specific calculation: capital balance (after revaluation profit goodwill share JLP share profit to death and any unpaid salary) less drawings = amount payable. The executor account is then closed — credit when payment is made (Cash Loan A/c) and Dr to Executor's A/c.

Q533 Marks

Settlement methods for retiring/deceased partner's claim:

Method

Description

Cash impact

Lump sum cash

Entire amount paid immediately

Large outflow

Loan account

Balance transferred to retiring partner's loan; interest paid

Smoothed over time

Annuity

Equal periodic payments for fixed term

Predictable

Combination

Part lump sum, part loan/annuity

Tailored to firm's cash position

Asset transfer

Specific asset given in lieu of cash

No cash outflow

Methods of settling retiring partner include:

ALump sum

BLoan

CAnnuity

DAll of these

Default interest rate on retiring partner's loan account =

A5%

B6%

C8%

DNo interest

Why is settlement through loan account often preferred over lump sum?

Show answersHide answers

1. Option 4 — All of these

2. Option 2 — 6%

3. The retiring partner's claim can be settled in several ways. Lump sum cash gives the partner immediate liquidity but reduces firm cash sharply. Transfer to loan account (typically at 6% p.a. interest) allows the firm to pay over time. Annuity provides equal periodic payments. Combination is common — part of the claim in cash, the rest in loan or annuity. Asset transfer is rare but possible if both parties agree. The choice depends on firm's cash availability and the retiring partner's preferences. The accounting entries reflect each: capital A/c is debited and cash/loan/annuity A/c is credited. Section 37 of the Partnership Act 1932 specifies the default interest rate of 6% p.a. on outstanding amounts due to retiring partners.

Q546 Marks

P Q and R are partners sharing 4:3:2. P retires. New ratio of Q and R is 5:4. Compute gaining ratio and P's share of goodwill.

Quantity

Value

P's old share

4/9

Q's old share

3/9

R's old share

2/9

Q's new share

5/9

R's new share

4/9

Goodwill of firm

₹90000

Q556 Marks

X dies on 30 September 2023. Previous year's profit was ₹120000. The firm shares profits equally and uses time basis for profit to date of death.

Quantity

Value

Date of death of X

30 September 2023

Period elapsed

6 months

Previous year's profit

₹120000

Profit-sharing ratio

1:1:1

Picture-Based Questions3 questions

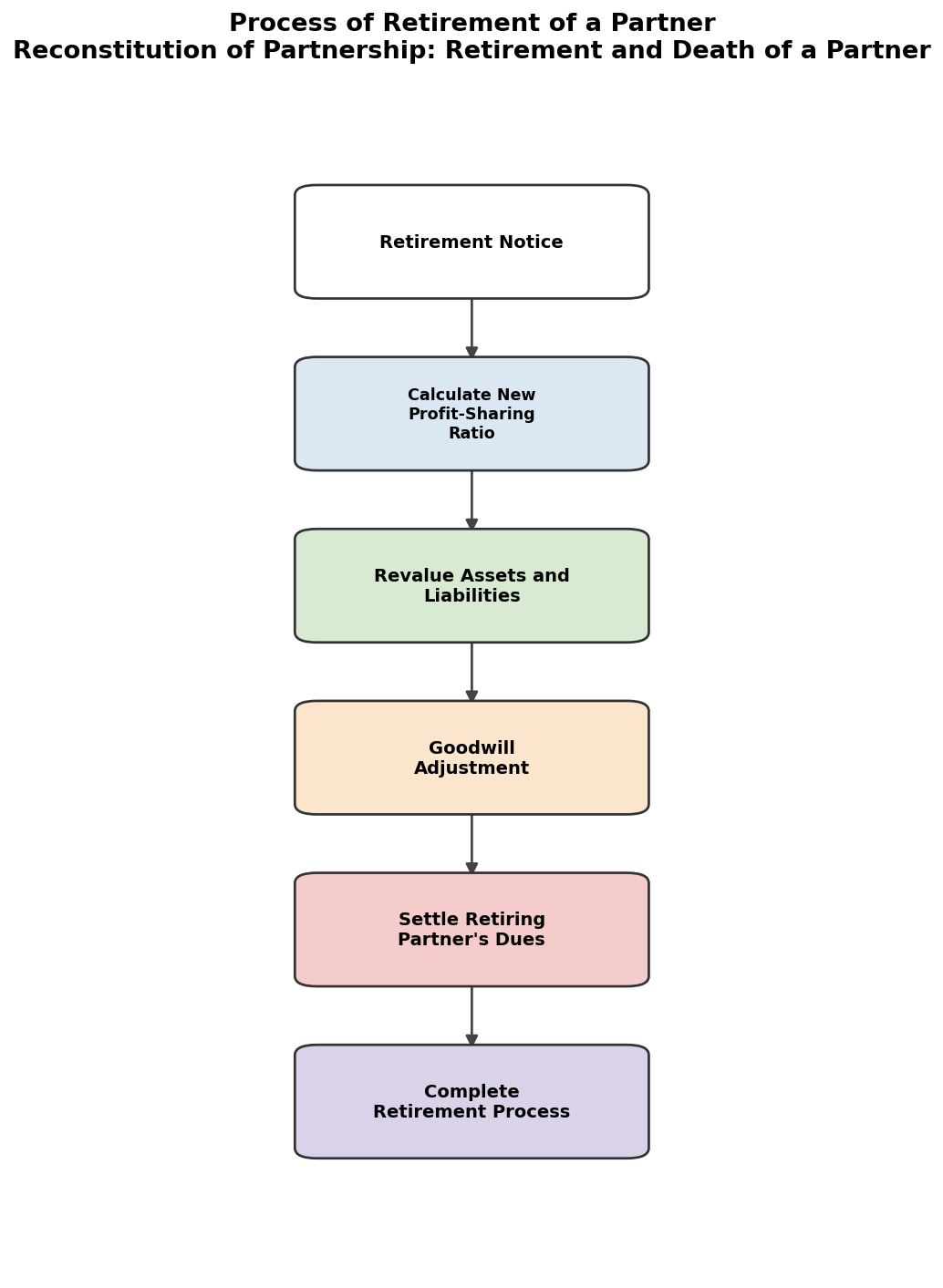

Q563 Marks

Based on the given flowchart, answer the following:

What is the first step in the process?

ACalculate New Profit-Sharing Ratio

BRevalue Assets and Liabilities

CRetirement Notice

DGoodwill Adjustment

What follows after calculating the new profit-sharing ratio?

ASettle Retiring Partner's Dues

BRevalue Assets and Liabilities

CGoodwill Adjustment

DComplete Retirement Process

Describe the importance of goodwill adjustment in the retirement process.

What is the first step in settling a retiring partner's dues?

ACalculate Share of Goodwill

BIdentify Dues

CDetermine Revalued Assets

DSettle Cash/Assets

What follows after calculating the share of goodwill?

AIdentify Dues

BSettle Cash/Assets

CDetermine Revalued Assets

DComplete Settlement

Discuss the implications of not settling a retiring partner's dues promptly.

Show answersHide answers

1. Option 3 — Retirement Notice

2. Option 2 — Revalue Assets and Liabilities

3. Goodwill adjustment ensures that the retiring partner receives their fair share of the firm's goodwill.

4. Option 2 — Identify Dues

5. Option 3 — Determine Revalued Assets

6. It can lead to legal disputes and financial instability in the partnership.

Q573 Marks

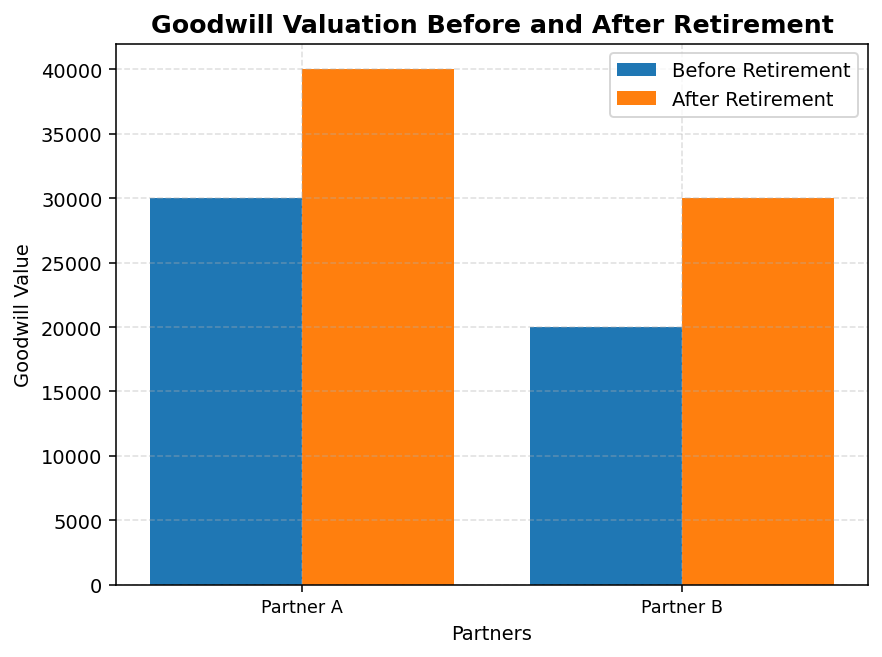

Based on the given chart, answer the following:

Which partner's goodwill value increased the most after retirement?

APartner A

BPartner B

CPartner C

DNone

What is the total goodwill value before retirement?

Calculate the percentage increase in Partner A's goodwill value after retirement.

What percentage of profit does Partner A receive after retirement?

A50%

B30%

C20%

D40%

If the total profit is 100, what is Partner B's share?

Explain how the profit-sharing ratio is affected by the retirement of a partner.

Show answersHide answers

1. Option 1 — Partner A

2. 65000

3. 33.33%

4. Option 1 — 50%

5. 30

6. The remaining partners' shares increase, redistributing the profits among them.

Q583 Marks

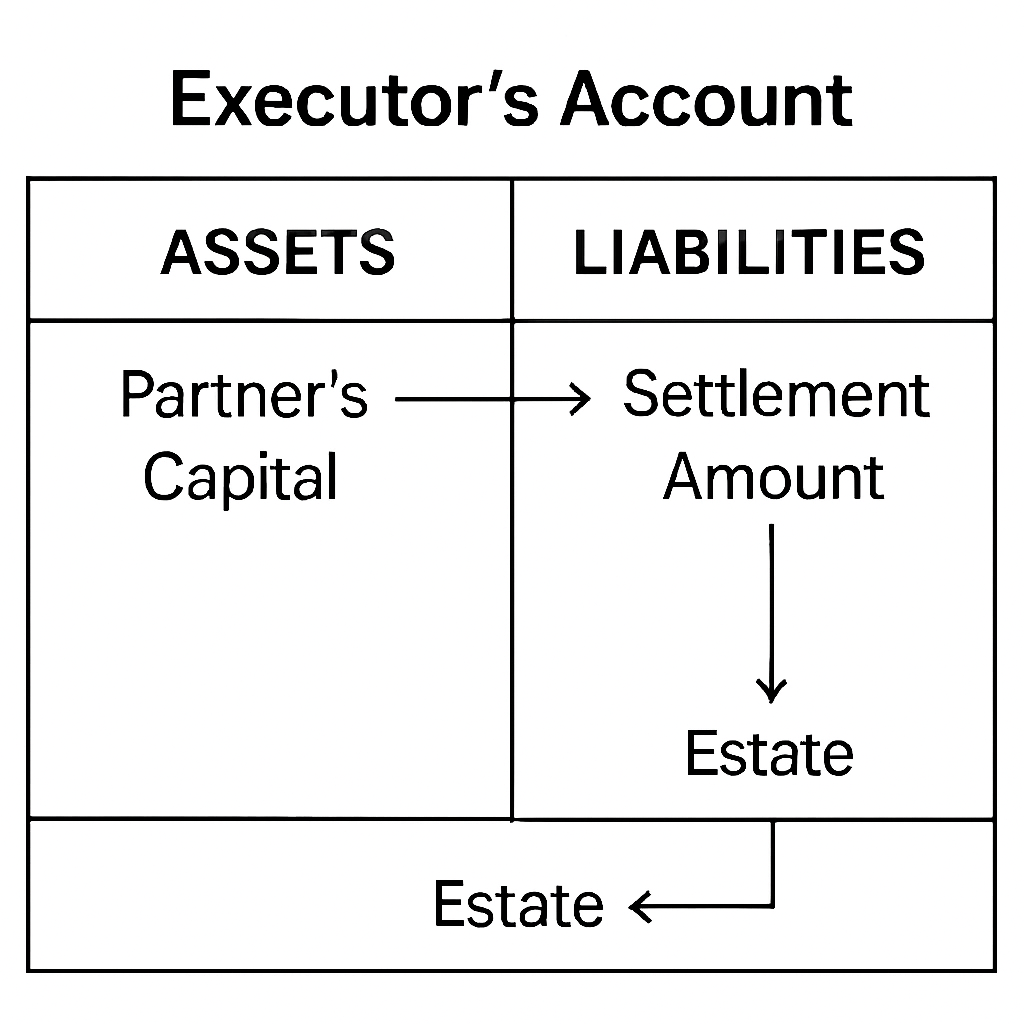

Based on the given diagram of the executor's account, answer the following:

What is the primary purpose of the executor's account?

ATo record daily transactions

BTo settle the deceased partner's dues

CTo calculate profits

DTo manage cash flow

List two components that should be included in the executor's account.

Explain how the executor's account affects the remaining partners.

Show answersHide answers

1. Option 2 — To settle the deceased partner's dues

2. Assets and Liabilities

3. It ensures that the remaining partners are aware of the financial obligations and settlements due to the deceased partner.