Analysis of Financial Statements — Important Questions

58 questions

With answersCBSE format

SUMMARY: The chapter focuses on understanding and interpreting financial statements to assess the financial health and performance of a business. KEY TOPICS: financial statements, comparative statements, common size statements, ratio analysis, liquidity ratios, profitability ratios, solvency ratios, trend analysis, limitations of financial analysis, cash flow analysis

What does liquidity ratio measure in financial statements?

AProfitability of a company

BAbility to meet short-term obligations

CLong-term financial stability

DOverall market performance

Check answerHide answer

Correct answer: Option 2 — Ability to meet short-term obligations

Q71 Mark

Which of the following is a limitation of financial analysis?

AProvides a clear picture of financial health

BBased on historical data

CHelps in decision making

DAssists in performance evaluation

Check answerHide answer

Correct answer: Option 2 — Based on historical data

Q81 Mark

What is the primary purpose of cash flow analysis?

ATo evaluate profitability

BTo assess liquidity

CTo determine solvency

DTo analyze market trends

Check answerHide answer

Correct answer: Option 2 — To assess liquidity

Q91 Mark

In a common-size statement, which of the following is typically used as a base for comparison?

ATotal liabilities

BTotal revenue

CTotal assets

DNet income

Check answerHide answer

Correct answer: Option 3 — Total assets

Q101 Mark

Which ratio indicates a company's ability to cover its long-term debts?

ACurrent ratio

BQuick ratio

CDebt to equity ratio

DReturn on equity

Check answerHide answer

Correct answer: Option 3 — Debt to equity ratio

Q111 Mark

What does a high current ratio indicate?

APoor liquidity position

BStrong liquidity position

CHigh profitability

DLow solvency

Check answerHide answer

Correct answer: Option 2 — Strong liquidity position

Q121 Mark

Which of the following is NOT a profitability ratio?

AGross profit margin

BNet profit margin

CReturn on assets

DCurrent ratio

Check answerHide answer

Correct answer: Option 4 — Current ratio

Q131 Mark

What is the main focus of trend analysis?

AComparing financial statements of different companies

BEvaluating financial performance over time

CAssessing market conditions

DAnalyzing cash flows

Check answerHide answer

Correct answer: Option 2 — Evaluating financial performance over time

Q141 Mark

Which financial statement provides information about a company's revenues and expenses?

ABalance sheet

BIncome statement

CCash flow statement

DEquity statement

Check answerHide answer

Correct answer: Option 2 — Income statement

Q151 Mark

What does the debt to equity ratio measure?

ALiquidity of the company

BProfitability of the company

CFinancial leverage of the company

DOperational efficiency of the company

Check answerHide answer

Correct answer: Option 3 — Financial leverage of the company

Short Answer Questions10 questions

Q163 Marks

What is meant by analysis of financial statements? List its objectives.

View sample solutionHide solution

Analysis of financial statements means systematically examining the figures in the financial statements to assess profitability, liquidity, solvency, and operational efficiency. Objectives: (i) judge the financial performance and position of the enterprise; (ii) compare performance over years (intra-firm) and with other firms (inter-firm); (iii) assess earning capacity; (iv) evaluate solvency and credit-worthiness; (v) help managers in planning and control; (vi) help investors in making investment decisions; (vii) help creditors and lenders assess risk.

Q173 Marks

List the various tools/techniques of financial statement analysis.

View sample solutionHide solution

(1) COMPARATIVE statements — show absolute and percentage changes year-over-year. (2) COMMON-SIZE statements — express every item as a percentage of a base (revenue from operations for P&L; total of equity/liabilities or assets for balance sheet); enables comparison across firms of different sizes. (3) TREND analysis — selects a base year and expresses subsequent years as a percentage of base. (4) RATIO analysis — computes financial ratios (liquidity profitability solvency activity). (5) CASH FLOW analysis — analyses inflows and outflows of cash. (6) FUNDS FLOW analysis — analyses changes in working capital. Each technique reveals different aspects.

Q183 Marks

Distinguish between comparative and common-size statements.

View sample solutionHide solution

Comparative statements: present financial data for two or more periods side by side; show absolute amounts and absolute/percentage CHANGES. Useful for trend analysis. Format: column for each period plus columns for change in absolute terms and as percentage. Common-size statements: express each item as a PERCENTAGE of a common base (revenue for P&L, total of equity & liabilities for balance sheet); show structural composition. Useful for inter-firm comparison and for analysing the relative weight of items within one period. Both can be applied to the balance sheet or the P&L.

Q193 Marks

Explain the limitations of financial statement analysis.

View sample solutionHide solution

Limitations: (1) Based on historical data — does not predict the future. (2) Based on accounting figures — accounting policies (depreciation methods, inventory valuation) affect comparability. (3) Ignores qualitative factors — quality of management employees brand value not captured. (4) Subject to window dressing — manipulating figures to mislead. (5) Inflation effect — historical cost ignores price-level changes. (6) Inter-firm comparison difficult — different accounting policies, sizes, sectors. Despite these limitations, analysis is essential — caveats must be noted but the data still provides useful insights.

Q203 Marks

List the parties interested in financial statement analysis.

View sample solutionHide solution

(1) Investors (shareholders) — return on investment and risk; (2) Lenders/creditors — solvency and ability to repay debt; (3) Management — planning control and strategic decisions; (4) Government and tax authorities — tax compliance and policy formulation; (5) Employees — job security wages and bonuses; (6) Customers — continuity of supply and warranties; (7) Suppliers — credit-worthiness; (8) Researchers and analysts — for academic and market analysis; (9) Competitors — benchmarking. Each user looks at different aspects of the same statements.

Q213 Marks

What are liquidity ratios and why are they important for a business?

View sample solutionHide solution

Liquidity ratios measure a company's ability to meet its short-term obligations. They are important because they indicate the financial health of a business and its capacity to cover immediate liabilities without needing to sell long-term assets.

Q223 Marks

Define profitability ratios and provide an example of one such ratio.

View sample solutionHide solution

Profitability ratios assess a company's ability to generate profit relative to its revenue, assets, or equity. An example is the Net Profit Margin, which shows the percentage of revenue that remains as profit after all expenses are deducted.

Q233 Marks

What is trend analysis in financial statements?

View sample solutionHide solution

Trend analysis involves comparing financial data over multiple periods to identify patterns or trends in performance. This helps stakeholders understand whether a company's financial health is improving or deteriorating over time.

Q243 Marks

Explain the significance of solvency ratios in financial analysis.

View sample solutionHide solution

Solvency ratios assess a company's ability to meet its long-term debts and obligations. They are significant because they provide insights into the financial stability and long-term viability of a business.

Q253 Marks

What is a common-size statement and how is it useful in financial analysis?

View sample solutionHide solution

A common-size statement expresses each line item as a percentage of a base figure, such as total revenue or total assets. This allows for easier comparison between companies of different sizes and helps in analyzing trends over time.

Long Answer Questions6 questions

Q266 Marks

Prepare a comparative balance sheet from the following: 31 Mar 2023 — Equity ₹400000, Reserves ₹100000, LT Borrowings ₹200000, Current Liab ₹50000; 31 Mar 2024 — Equity ₹500000, Reserves ₹150000, LT Borrowings ₹180000, Current Liab ₹60000. (Assets: Fixed assets ₹500000 → ₹650000; Current assets ₹250000 → ₹240000.)

Prepare a common-size P&L statement: Revenue ₹500000; Cost of Materials ₹200000; Employee Benefits ₹100000; Other Expenses ₹50000; Finance Costs ₹20000; Depreciation ₹30000; Tax @25% on profit before tax.

View sample solutionHide solution

Common-size P&L (% of Revenue from Operations): Revenue 500000 (100%); Cost of Materials 200000 (40%); Employee Benefits 100000 (20%); Other Expenses 50000 (10%); Finance Costs 20000 (4%); Depreciation 30000 (6%); Total Expenses 400000 (80%); Profit Before Tax 100000 (20%); Tax @25% × 100000 = 25000 (5%); Profit After Tax 75000 (15%). The percentages reveal the cost structure: 40% of revenue goes to materials (the largest cost), 20% to employees. Compare across firms of different sizes by looking at percentages rather than absolute amounts.

Q286 Marks

Compute trend percentages with 2021 as base year for these revenues: 2021 ₹500000; 2022 ₹600000; 2023 ₹720000; 2024 ₹800000.

View sample solutionHide solution

Trend Percentage = (Year value / Base year value) × 100. Base year (2021) = 100%. 2022 = 600000 / 500000 × 100 = 120%. 2023 = 720000 / 500000 × 100 = 144%. 2024 = 800000 / 500000 × 100 = 160%. Insight: Revenue has grown 60% over 3 years (CAGR of about 17% per year). The trend is upward consistent and accelerating — indicates strong business growth. Trend analysis is best applied to multiple line items (revenue costs profit) and over 5+ years to spot direction and momentum. Useful in identifying turning points and divergence (e.g., revenue growing but profit margin shrinking).

Q296 Marks

Discuss the importance and limitations of comparative statements.

View sample solutionHide solution

Importance: (1) Trend identification — visualises improvement or deterioration year-on-year; (2) Performance evaluation — quick view of growth in revenue, profit, assets; (3) Decision-making aid for investors lenders managers; (4) Identifies areas needing attention (e.g., operating cost rising faster than revenue). Limitations: (1) Only two periods compared at a time — long-term trend requires multiple years; (2) Inter-firm comparison difficult due to size differences (resolved by common-size); (3) Inflation distorts year-on-year comparison if not adjusted; (4) Changes in accounting policies make comparisons unreliable; (5) Qualitative factors (management quality brand) not captured. Comparative statements are most useful WITH other techniques (common-size ratio analysis trend analysis) for a complete picture.

Q306 Marks

Discuss the various users of financial statement analysis and their specific information needs.

View sample solutionHide solution

INVESTORS — focus on profitability (P&L) earnings per share dividend payout return on equity; investment decision (buy/hold/sell). LENDERS/CREDITORS — focus on debt-equity ratio interest coverage current ratio; lend or not, at what rate. MANAGEMENT — uses internal reports for planning control budgeting and strategy; comprehensive view of all metrics. GOVERNMENT — tax computation industry policy formulation revenue forecasts. EMPLOYEES — job security future bonus negotiations. CUSTOMERS — continuity of supply warranty service availability. SUPPLIERS — payment timeliness creditworthiness for extending credit. RESEARCHERS — academic studies industry analysis. COMPETITORS — benchmarking and competitive positioning. Each user prioritises different parts of the analysis.

Q316 Marks

Differentiate between horizontal analysis and vertical analysis of financial statements in tabular form.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): Financial statement analysis helps users assess the financial health of a business.

Reason (R): The analysis processes raw figures into meaningful indicators of profitability liquidity and solvency.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Common-size statements express items as percentages of a base.

Reason (R): Common-size enables comparison across firms of different sizes and across years.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): Comparative statements show absolute and percentage changes year-on-year.

Reason (R): The technique helps identify growth or decline in specific items.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Trend analysis is best done over 5 or more years.

Reason (R): A long base period reveals the general direction of business and helps spot turning points.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Analysis based purely on historical figures has limitations.

Reason (R): Past performance is not always indicative of future performance.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): Liquidity ratios are used to measure a company's ability to meet its short-term obligations.

Reason (R): A higher liquidity ratio indicates better financial health in terms of short-term solvency.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): Profitability ratios provide insights into a company's ability to generate earnings relative to its revenue.

Reason (R): These ratios are calculated using only the income statement figures.

Show explanationHide explanation

Correct answer: Option 2 —

Both A and R are true, but R is not the correct explanation of A.

Q391 Mark

Assertion (A): Solvency ratios assess a company's long-term financial stability.

Reason (R): These ratios are primarily derived from the balance sheet and do not consider cash flow.

Show explanationHide explanation

Correct answer: Option 3 —

A is true, but R is false.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: Comparative and common-size are tools of vertical and horizontal analysis.

Statement 2: Ratio analysis provides indicators of liquidity profitability and solvency.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Common-size statements are useful for inter-firm comparison.

Statement 2: Different firms can be compared on a relative scale rather than absolute size.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Investors lenders and management are key users of analysis.

Statement 2: Each user focuses on different aspects of the financial statements.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Inflation and changes in accounting policies limit comparability.

Statement 2: Such factors can distort year-on-year comparisons.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Quality of management and brand value are not reflected in financial statements.

Statement 2: Hence quantitative analysis must be supplemented with qualitative judgement.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: Liquidity ratios measure a company's ability to meet its short-term obligations.

Statement 2: Profitability ratios assess a company's overall financial health and long-term viability.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q461 Mark

Statement 1: Trend analysis involves comparing financial data over multiple periods to identify patterns.

Statement 2: Common size statements express each line item as a percentage of total revenue.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q471 Mark

Statement 1: Solvency ratios are used to evaluate a company's ability to generate profits.

Statement 2: Cash flow analysis helps in understanding the cash inflows and outflows of a business.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Case Study / Passage Questions4 questions

Q483 Marks

M/s Kapur Industries has these balances. 31 March 2023: Equity Capital ₹400000, Reserves ₹100000, Long-term Borrowings ₹200000, Current Liabilities ₹50000, Fixed Assets ₹500000, Current Assets ₹250000. 31 March 2024: Equity Capital ₹500000, Reserves ₹150000, Long-term Borrowings ₹180000, Current Liabilities ₹60000, Fixed Assets ₹650000, Current Assets ₹240000.

The technique that shows changes year-on-year is:

AComparative statement

BCommon-size statement

CTrend analysis

DCash flow

Equity capital change as percentage =

A+25%

B+50%

C+10%

D−10%

Prepare the comparative balance sheet showing changes.

Show answersHide answers

1. Option 1 — Comparative statement

2. Option 1 — +25%

3. Comparative Balance Sheet showing absolute and percentage changes. Equity Capital 400000→500000 (Δ +100000 +25%); Reserves 100000→150000 (+50000 +50%); Long-term Borrowings 200000→180000 (−20000 −10%); Current Liab 50000→60000 (+10000 +20%); Total Liab/Equity 750000→890000 (+140000 +18.7%). Fixed Assets 500000→650000 (+150000 +30%); Current Assets 250000→240000 (−10000 −4%); Total Assets 750000→890000 (+140000 +18.7%). Insights: Capital grew strongly (+25%); Reserves grew faster (+50%) suggesting profit retention; Long-term borrowings reduced (−10%); Fixed Assets grew significantly (+30%) — indicates capital investment. Comparative analysis is best paired with common-size and trend analysis for a complete picture.

Q493 Marks

M/s Reema Ltd has these P&L figures. Revenue ₹500000; Cost of Materials ₹200000; Employee Benefits ₹100000; Other Expenses ₹50000; Finance Costs ₹20000; Depreciation ₹30000; Tax @25% on profit before tax.

The technique that expresses items as percentage of base is:

AComparative

BCommon-size

CTrend

DCash flow

Cost of Materials as % of Revenue =

A40% of Revenue

B80% of Revenue

C20% of Revenue

D15% of Revenue

Prepare a common-size P&L and explain insights.

Show answersHide answers

1. Option 2 — Common-size

2. Option 1 — 40% of Revenue

3. Common-size P&L (% of Revenue from Operations): Revenue 500000 (100%); Cost of Materials 200000 (40%); Employee Benefits 100000 (20%); Other Expenses 50000 (10%); Finance Costs 20000 (4%); Depreciation 30000 (6%); Total Expenses 400000 (80%); Profit Before Tax 100000 (20%); Tax @25% × 100000 = 25000 (5%); Profit After Tax 75000 (15%). The percentages reveal cost structure: 40% of revenue goes to materials (the largest cost), 20% to employees. Compare with industry benchmarks or different firms — those with materials costs higher than 40% may have pricing or supply-chain issues. Common-size statements enable fair comparison across firms of different sizes.

Q503 Marks

M/s Verma Stores has these annual revenues: 2020 ₹500000; 2021 ₹600000; 2022 ₹720000; 2023 ₹800000; 2024 ₹900000. The company wants to understand its growth pattern.

The technique using a base year and percentages is:

AComparative

BCommon-size

CTrend analysis

DRatio

2024 trend % (base 2020 = 100) =

A144%

B160%

C180%

D100%

Compute trend percentages and discuss the insight.

Show answersHide answers

1. Option 3 — Trend analysis

2. Option 3 — 180%

3. Trend analysis with 2020 as base year (= 100%). 2021: 600000/500000 × 100 = 120%. 2022: 720000/500000 × 100 = 144%. 2023: 800000/500000 × 100 = 160%. 2024: 900000/500000 × 100 = 180%. Insight: Revenue has grown 80% over 4 years (CAGR ≈ 16% per year). The trend is upward and consistent — indicates strong business growth. Trend analysis is most useful when applied to multiple line items (revenue costs profit) and over 5+ years. It reveals long-term direction but should be combined with other techniques (common-size ratio analysis) for a complete picture. A consistently rising trend in costs while revenue plateaus would signal margin pressure.

Q513 Marks

The analysis of financial statements is crucial for stakeholders to evaluate a company's performance and financial health. Financial statements include the balance sheet, income statement, and cash flow statement. Comparative statements allow for the analysis of financial data over different periods, highlighting trends and changes in financial performance. Common size statements express each line item as a percentage of a base figure, facilitating comparison across companies of different sizes. Ratio analysis is a key tool in this process, where various ratios such as liquidity ratios, profitability ratios, and solvency ratios are calculated to assess different aspects of a company's financial condition. For instance, liquidity ratios measure a company's ability to meet short-term obligations, while profitability ratios evaluate its ability to generate profit relative to sales, assets, or equity. Understanding these concepts helps stakeholders make informed decisions regarding investments, credit, and management strategies.

What is the primary purpose of analyzing financial statements?

ATo prepare tax returns

BTo evaluate company performance

CTo determine employee salaries

DTo create marketing strategies

Define common size statements and their significance.

Which type of ratio assesses a company's ability to meet short-term obligations?

AProfitability ratios

BLiquidity ratios

CSolvency ratios

DEfficiency ratios

Show answersHide answers

1. Option 2 — To evaluate company performance

2. Common size statements express each line item as a percentage of a base figure, allowing for easier comparison across companies and periods.

3. Option 2 — Liquidity ratios

Table-Based Questions4 questions

Q523 Marks

Compare tools of financial statement analysis:

Tool

What it shows

Best for

Comparative

Year-on-year changes

Identifying trends

Common-size

Items as % of base

Inter-firm comparison

Trend analysis

% over 5+ years from base

Long-term direction

Ratio analysis

Single-figure indicators

Comparing performance

Cash flow

Cash inflows/outflows

Liquidity assessment

Common-size analysis is best for:

ATrend

BCommon-size

CComparative

DRatio

Trend analysis is best done over:

A5+ years

B1 year

C1 month

DRandom

Why are multiple tools used together rather than relying on one?

Show answersHide answers

1. Option 2 — Common-size

2. Option 1 — 5+ years

3. Each tool of financial analysis has distinct strengths. Comparative statements show year-on-year movement and reveal direction of change. Common-size statements normalise figures by expressing items as percentages of a common base — perfect for comparing firms of different sizes. Trend analysis tracks long-term movement of selected items over 5+ years using a base year. Ratio analysis provides single-figure indicators of liquidity profitability solvency and activity. Cash flow analysis reveals how cash has been generated and used. Best practice: use multiple tools together. Comparative + common-size shows both absolute and relative changes; trend reveals long-term direction; ratios benchmark performance.

Q533 Marks

Users of financial statement analysis and their information needs:

User

Information needed

Decision

Investors

Profitability, EPS, dividend

Buy/hold/sell

Lenders

Solvency, debt-equity

Lend/at what rate

Management

All metrics

Plan/control

Government

Tax compliance

Tax assessment

Employees

Profitability, growth

Job security/bonus

Customers

Continuity

Continued supply

Suppliers

Creditworthiness

Extend credit

Who is most interested in debt-equity ratio?

AInvestors

BLenders

CGovernment

DCustomers

Who looks at creditworthiness for extending trade credit?

ASuppliers

BInvestors

CEmployees

DGovernment

Why does each user focus on different parts of the analysis?

Show answersHide answers

1. Option 2 — Lenders

2. Option 1 — Suppliers

3. Different users have different information needs. Investors focus on profitability and return — they decide whether to invest more or exit. Lenders focus on solvency (debt-equity interest coverage) — to lend or not, at what rate. Management uses comprehensive analysis for planning control and strategic decisions. Government cares about tax compliance and revenue. Employees look for stability and growth — for job security and bonus negotiations. Customers want continuity of supply and warranty coverage. Suppliers assess creditworthiness for extending trade credit. The same financial statements serve all users but each focuses on different parts of the analysis.

Q546 Marks

Prepare a comparative balance sheet for M/s Kapur Industries showing absolute and percentage changes.

Item

31 Mar 2023

31 Mar 2024

Equity Capital

₹400000

₹500000

Reserves

₹100000

₹150000

Long-term Borrowings

₹200000

₹180000

Current Liabilities

₹50000

₹60000

Fixed Assets

₹500000

₹650000

Current Assets

₹250000

₹240000

Q556 Marks

Prepare a common-size P&L statement for M/s Reema Ltd showing each item as a percentage of revenue.

Item

Amount

Revenue

₹500000

Cost of Materials

₹200000

Employee Benefits

₹100000

Other Expenses

₹50000

Finance Costs

₹20000

Depreciation

₹30000

Tax rate

25%

Picture-Based Questions3 questions

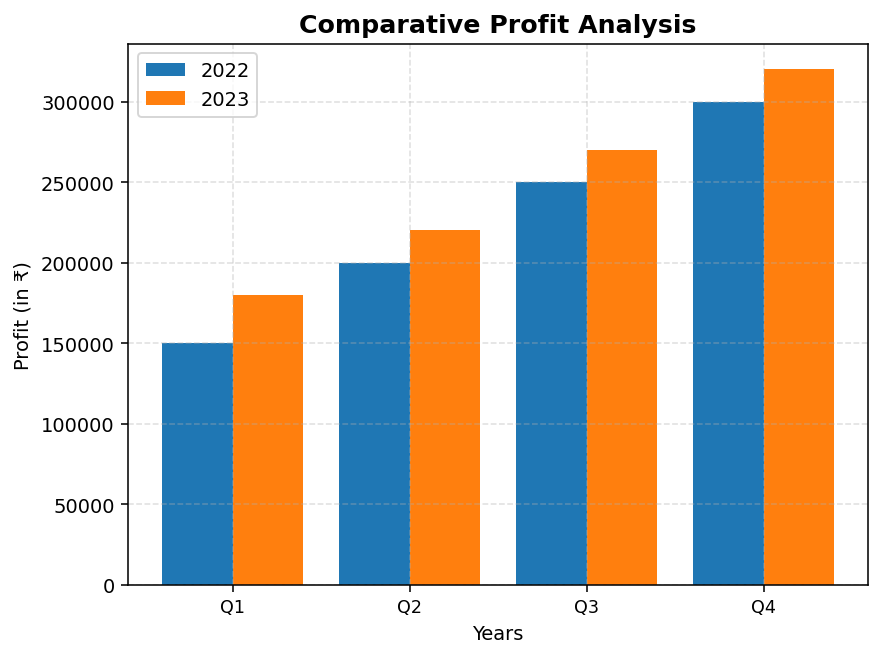

Q562 Marks

Based on the given chart, answer the following:

Which quarter showed the highest profit in 2023?

AQ1

BQ2

CQ3

DQ4

What is the total profit for 2022?

What percentage of total expenses is allocated to Marketing?

A10%

B15%

C20%

D25%

Calculate the total percentage of expenses for Salaries and Rent combined.

Show answersHide answers

1. Option 4 — Q4

2. 900000

3. Option 3 — 20%

4. 55%

Q572 Marks

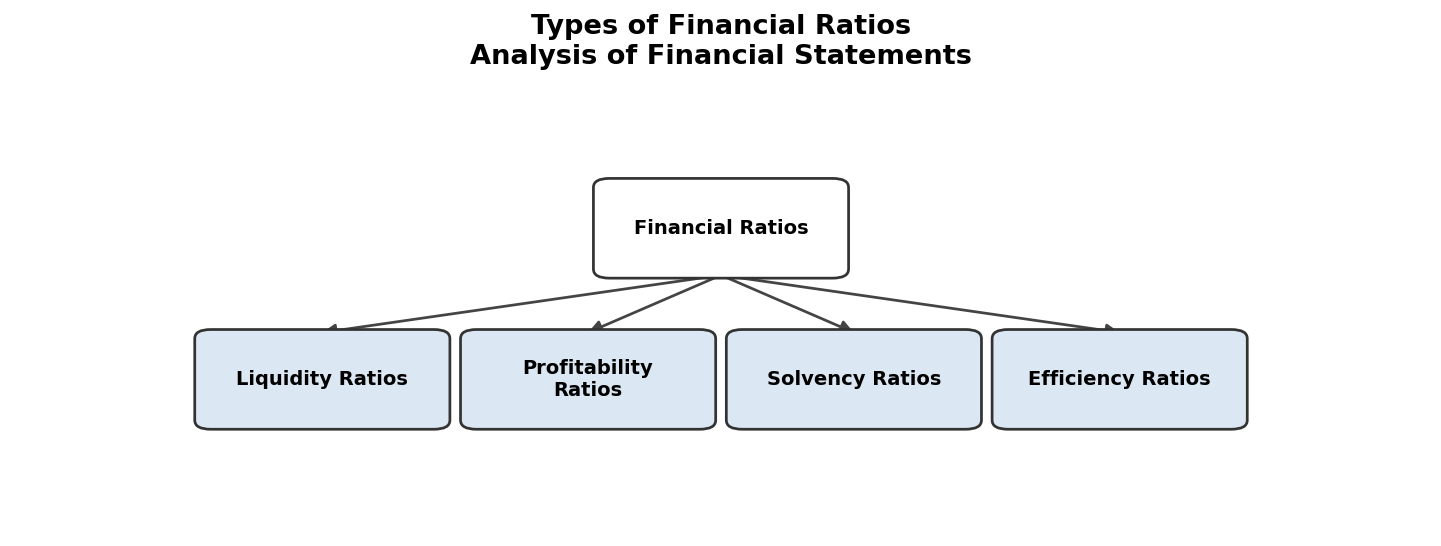

Based on the given flowchart, answer the following:

Which type of ratio assesses a company's ability to meet short-term obligations?

ALiquidity Ratios

BProfitability Ratios

CSolvency Ratios

DEfficiency Ratios

List one example of a profitability ratio.

Which limitation refers to the reliance on past performance?

AHistorical Data

BSubjectivity

CNon-Financial Factors

DWindow Dressing

Explain what is meant by 'Window Dressing' in financial statements.

Show answersHide answers

1. Option 1 — Liquidity Ratios

2. Net Profit Margin

3. Option 1 — Historical Data

4. Manipulating financial statements to present a more favorable picture.

Q582 Marks

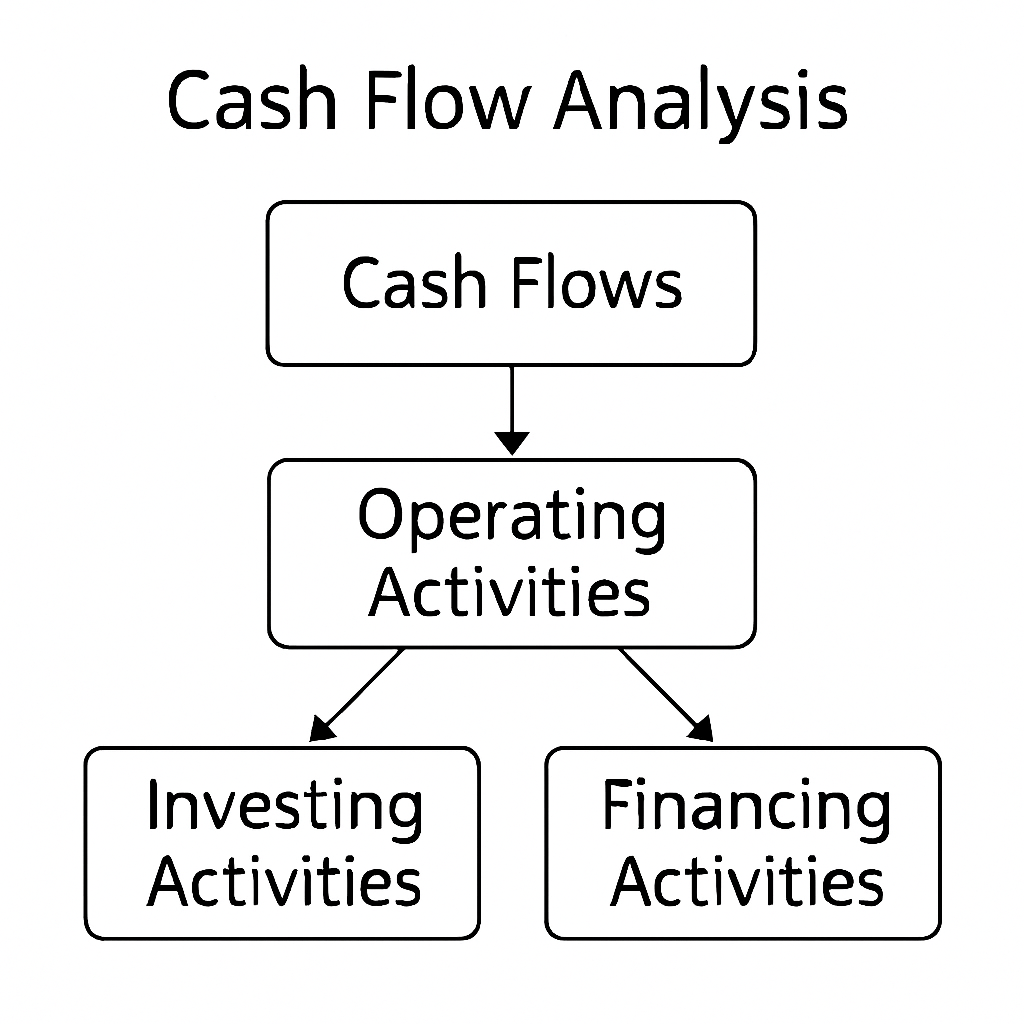

Based on the given diagram of cash flow analysis, answer the following:

What are the three main activities involved in cash flow analysis?

AOperating, Investing, Financing

BRevenue, Expense, Profit

CAssets, Liabilities, Equity

DSales, Purchases, Returns

Explain the importance of cash flow analysis in financial statements.

Show answersHide answers

1. Option 1 — Operating, Investing, Financing

2. It helps assess the liquidity and financial health of a business.