Accounting for Share Capital — Important Questions

58 questions

With answersCBSE format

SUMMARY: This chapter focuses on the accounting treatment and procedures related to the issue and management of share capital in a company. KEY TOPICS: types of share capital, issue of shares, over-subscription and under-subscription, calls in arrears and calls in advance, forfeiture of shares, reissue of forfeited shares, accounting treatment of share capital, disclosure of share capital in financial statements, pro-rata allotment.

What is the maximum amount of share capital that a company can issue as per its memorandum of association?

AIssued Capital

BPaid-up Capital

CAuthorized Capital

DSubscribed Capital

Check answerHide answer

Correct answer: Option 3 — Authorized Capital

Q71 Mark

When a company issues shares for cash, how is the amount received in excess of the face value treated?

AAs a liability

BAs a revenue

CAs a securities premium

DAs an expense

Check answerHide answer

Correct answer: Option 3 — As a securities premium

Q81 Mark

In the case of over-subscription of shares, what is the process followed for allotment?

AAllotment on a first-come, first-served basis

BPro-rata allotment

CRandom selection

DFull allotment to all applicants

Check answerHide answer

Correct answer: Option 2 — Pro-rata allotment

Q91 Mark

Which of the following is NOT a type of share capital?

AEquity Share Capital

BPreference Share Capital

CDebenture Capital

DAuthorized Share Capital

Check answerHide answer

Correct answer: Option 3 — Debenture Capital

Q101 Mark

What does 'calls in arrears' refer to in share capital accounting?

AAdvance payment of calls

BUnpaid calls on shares

CCalls that are fully paid

DCalls that are forfeited

Check answerHide answer

Correct answer: Option 2 — Unpaid calls on shares

Q111 Mark

If a company forfeits shares, what is the accounting treatment for the forfeited shares?

AThey are treated as an asset

BThey are shown as a liability

CThey are transferred to a forfeited shares account

DThey are written off completely

Check answerHide answer

Correct answer: Option 3 — They are transferred to a forfeited shares account

Q121 Mark

What is the term for shares that have been issued but not yet fully paid for by shareholders?

APaid-up Shares

BIssued Shares

CCalls in Advance

DCalls in Arrears

Check answerHide answer

Correct answer: Option 4 — Calls in Arrears

Q131 Mark

Which financial statement must disclose the share capital of a company?

AIncome Statement

BBalance Sheet

CCash Flow Statement

DStatement of Changes in Equity

Check answerHide answer

Correct answer: Option 2 — Balance Sheet

Q141 Mark

What is the primary reason for a company to reissue forfeited shares?

ATo increase liabilities

BTo recover unpaid amounts

CTo raise additional capital

DTo reduce authorized capital

Check answerHide answer

Correct answer: Option 3 — To raise additional capital

Q151 Mark

In the context of share capital, what does 'pro-rata allotment' mean?

AAllotting shares equally to all applicants

BAllotting shares based on the amount applied

CAllotting shares based on seniority

DAllotting shares randomly

Check answerHide answer

Correct answer: Option 2 — Allotting shares based on the amount applied

Short Answer Questions10 questions

Q163 Marks

Distinguish between authorised issued and paid-up capital.

View sample solutionHide solution

Authorised (or Nominal/Registered) capital — the maximum amount of capital a company is authorised to raise per its memorandum of association. Issued capital — the portion of authorised capital actually offered to the public for subscription. Subscribed capital — the part of issued capital that the public has agreed to subscribe. Called-up capital — the part of subscribed capital that the company has called from shareholders. Paid-up capital — the part of called-up capital that shareholders have actually paid. Authorised ≥ Issued ≥ Subscribed ≥ Called-up ≥ Paid-up.

Q173 Marks

Distinguish between equity shares and preference shares.

View sample solutionHide solution

Equity shares — owners of the company; voting rights; dividend after preference shareholders; residual claim on assets at liquidation; risk and reward proportional. Preference shares — preferred over equity for dividend (fixed rate) and capital repayment; usually NO voting rights (except on matters affecting their interests); the dividend is fixed and may be cumulative or non-cumulative; participating or non-participating in surplus profits. Companies issue preference for steady-yield investors; equity for risk-takers seeking growth.

Q183 Marks

Explain over-subscription and the methods of dealing with it.

View sample solutionHide solution

Over-subscription occurs when applications received exceed shares offered. SEBI guidelines provide methods: (1) Reject excess applications — refund excess money to applicants who get nothing. (2) Pro-rata allotment — every applicant gets proportionately fewer shares; excess money used to adjust against allotment/calls. (3) Combined — some applicants rejected, others get pro-rata. The chosen method must be disclosed in the prospectus. Refund or adjustment must be made within the prescribed time to avoid SEBI penalties.

Q193 Marks

What is forfeiture of shares and what is its effect?

View sample solutionHide solution

Forfeiture is the cancellation of shares by the company because the shareholder failed to pay any call (allotment or call money) within the stipulated time. Effect: (1) The defaulter loses his rights and the share is cancelled; (2) The amount already paid is forfeited (NOT refunded) and credited to Forfeited Shares A/c; (3) The forfeited shares can be re-issued by the company at any price not less than the unpaid amount; (4) Any profit on re-issue is transferred to Capital Reserve.

Q203 Marks

Explain calls in arrears and calls in advance.

View sample solutionHide solution

Calls in arrears: amount called by the company but not yet paid by shareholders. Treated as a deduction from called-up capital on balance sheet; interest may be charged on calls in arrears (typically 5% p.a. unless otherwise specified). Calls in advance: amount paid by shareholders before the company has called for it. Treated as a current liability (amount payable when call is made); interest may be paid on calls in advance (typically 6% p.a. as per Articles). Both arise from timing differences between calls and payments.

Q213 Marks

What are the different types of share capital?

View sample solutionHide solution

The different types of share capital include authorized capital, issued capital, subscribed capital, and paid-up capital. Authorized capital is the maximum amount of share capital that a company can issue, while issued capital is the portion that has actually been offered to shareholders.

Q223 Marks

Define pro-rata allotment of shares.

View sample solutionHide solution

Pro-rata allotment refers to the allocation of shares to applicants in proportion to the number of shares they applied for when the demand exceeds the number of shares available. This method ensures that all applicants receive a fair share based on their application.

Q233 Marks

What is the accounting treatment for calls in arrears?

View sample solutionHide solution

Calls in arrears are amounts due from shareholders who have not paid their calls on shares. In accounting, they are shown as a deduction from the total amount of share capital in the balance sheet until paid.

Q243 Marks

Explain the process of reissue of forfeited shares.

View sample solutionHide solution

Reissue of forfeited shares involves selling shares that were previously forfeited due to non-payment of calls. The company can reissue these shares at a price that may be lower than the original issue price, and the proceeds are credited to the share capital account.

Q253 Marks

What is the significance of disclosing share capital in financial statements?

View sample solutionHide solution

Disclosing share capital in financial statements is crucial as it provides stakeholders with information about the company's equity structure, financial health, and the amount of funds raised through equity financing. It enhances transparency and informs investors about their ownership stake.

Long Answer Questions6 questions

Q266 Marks

M/s Solar Ltd issues 10000 equity shares of ₹10 each at a premium of ₹2. Pass journal entries for: (i) application 100% received; (ii) allotment 5000 received; (iii) first call 2500 received with one shareholder owning 100 shares not paying; (iv) final call 2500 received with the same shareholder still not paying; (v) forfeiture of 100 shares.

View sample solutionHide solution

(i) Bank A/c Dr 100000 (10000 × 10); To Application A/c 100000. (Being application money received.) Application A/c Dr 100000; To Share Capital A/c 50000 (10000 × 5 — face value portion); To Securities Premium A/c 20000 (10000 × 2 — premium portion); To Allotment A/c 30000 (10000 × 3 — adjusted to allotment). (ii) Bank A/c Dr 50000 (5000 × 10000 / 10); To Allotment A/c 50000. (iii) Bank A/c Dr 24500 (after deducting 100 × 5 = 500 unpaid); To First Call A/c 24500. (iv) Bank A/c Dr 24500 (similarly); To Final Call A/c 24500. (v) Forfeiture: Share Capital A/c Dr 1000 (100 × 10); To First Call A/c 500; To Final Call A/c 500; To Forfeited Shares A/c (already paid amount). The numerical assumptions illustrate the methodology — the actual amounts depend on specific values per share (face value premium application allotment first/final call breakdown).

Q276 Marks

Discuss the issue of shares at premium and at discount.

View sample solutionHide solution

Issue at premium — share issued at price higher than face value (e.g. ₹100 face value at ₹120). The premium ₹20 is credited to Securities Premium A/c (a reserve). Securities premium can be used only for specified purposes under Section 52 of Companies Act 2013: issue of bonus shares writing off preliminary expenses writing off issue expenses providing premium on redemption of preference shares/debentures or buyback. Cannot be distributed as dividend. Issue at discount — share issued below face value (e.g. ₹100 at ₹95). Section 53 of Companies Act 2013 PROHIBITS issue of shares at discount (except sweat equity shares to employees). Hence issue at discount is NOT permitted in normal course.

Q286 Marks

Solar Ltd forfeited 200 shares of ₹10 each fully called up for non-payment of final call of ₹3 per share. Of the forfeited shares 150 were re-issued at ₹8 per share fully paid. Pass journal entries.

View sample solutionHide solution

Forfeiture: Share Capital A/c Dr 2000 (200 × 10); To Forfeited Shares A/c 1400 (200 × 7 — already paid); To Final Call A/c 600 (200 × 3). Re-issue of 150 shares at ₹8: Bank A/c Dr 1200 (150 × 8); Forfeited Shares A/c Dr 300 (loss on re-issue 150 × 2); To Share Capital A/c 1500 (150 × 10). Transfer to Capital Reserve: balance in Forfeited Shares A/c after re-issue = 1400 × (150/200) − 300 = 1050 − 300 = ₹750. Forfeited Shares A/c Dr 750; To Capital Reserve A/c 750. The remaining 50 forfeited shares' forfeited amount stays in Forfeited Shares A/c until they are re-issued.

Q296 Marks

M/s Bharat Ltd issues 5000 equity shares of ₹10 each. Applications received for 8000 shares. Pro-rata allotment is made. Pass journal entries (assume application ₹3, allotment ₹4, first and final call ₹3 each).

View sample solutionHide solution

Pro-rata: 5000 / 8000 = 5/8 of applied. Each applicant for 8 gets 5; excess application money 3 × 3 (per applicant) = ₹9 adjusted to allotment per applicant. (i) Bank A/c Dr 24000 (8000 × 3); To Application A/c 24000. (ii) Application A/c Dr 24000; To Share Capital A/c 15000 (5000 × 3); To Allotment A/c 9000 (excess application adjusted to allotment). (iii) Allotment due 5000 × 4 = 20000; less excess from application 9000 = 11000 to be received. Bank A/c Dr 11000; To Allotment A/c 11000. (iv) First call: Bank A/c Dr 15000 (5000 × 3); To First Call A/c 15000. (v) Final call: Bank A/c Dr 15000 (5000 × 3); To Final Call A/c 15000. Total capital raised = 50000.

Q306 Marks

Discuss the various reserves arising from share capital transactions and their use.

View sample solutionHide solution

Reserves from share capital transactions: (1) Securities Premium A/c — premium on issue of shares; can be used for bonus issue writing off preliminary or issue expenses providing premium on redemption of debentures/preference shares or buyback (Section 52 Companies Act 2013). (2) Capital Reserve — premium on forfeiture (after re-issue) profit on sale of fixed assets pre-incorporation profits; not available for cash dividend; used for writing off capital losses or issue of bonus shares. (3) General Reserve — appropriation of revenue profits; available for dividend equalisation business expansion. (4) Forfeited Shares A/c — temporary reserve holding amounts forfeited; transferred to Capital Reserve on re-issue. (5) Capital Redemption Reserve — created on redemption of preference shares out of profits; cannot be used for dividend.

Q316 Marks

Differentiate between equity shares and preference shares in tabular form on five features.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): A share is a unit of ownership in a company.

Reason (R): A shareholder is part-owner of the company and shares its profits and losses.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Equity shareholders bear the maximum risk in a company.

Reason (R): They are entitled to the residual profits and assets after preference shareholders are paid.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): Forfeited shares can be re-issued at a discount.

Reason (R): The discount must not exceed the amount already forfeited on those shares.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Securities premium cannot be used for cash dividend.

Reason (R): Section 52 of the Companies Act 2013 specifies the limited uses of securities premium.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Calls in advance is a current liability.

Reason (R): The amount represents money owed by the company to be applied against future calls.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): Equity shares provide voting rights to shareholders.

Reason (R): Preference shares do not carry voting rights.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): Over-subscription occurs when the number of shares applied for exceeds the number of shares issued.

Reason (R): Under-subscription means fewer shares are applied for than are available.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q391 Mark

Assertion (A): Calls in arrears represent amounts due from shareholders on shares issued.

Reason (R): Calls in advance are amounts paid by shareholders before they are due.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: Equity shares carry voting rights.

Statement 2: Preference shares usually do not carry voting rights except on matters affecting them.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Authorised capital is the upper limit set in the memorandum.

Statement 2: Subscribed capital is the part actually agreed to be taken up by the public.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Over-subscription is dealt with by rejection or pro-rata allotment.

Statement 2: SEBI rules require disclosure of the chosen method in the prospectus.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Securities premium is part of reserves and surplus.

Statement 2: It is shown separately on the balance sheet and used only as per Section 52.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Profit on forfeiture and re-issue is transferred to Capital Reserve.

Statement 2: Capital Reserve is generally not used for cash dividends.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: Calls in arrears must be paid before a shareholder can sell their shares.

Statement 2: Calls in advance can be refunded to shareholders at any time.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q461 Mark

Statement 1: The reissue of forfeited shares can be done at a price lower than the original issue price.

Statement 2: Forfeited shares cannot be reissued under any circumstances.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: Under-subscription means that the number of shares applied for is less than the number of shares issued.

Statement 2: In case of under-subscription, the company must refund the excess application money immediately.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Case Study / Passage Questions4 questions

Q483 Marks

M/s Solar Ltd is incorporated and issues 10000 equity shares of ₹10 each at par. The amounts payable: ₹3 on application ₹3 on allotment ₹2 on first call ₹2 on final call. Applications received are 12000 shares. M/s Solar Ltd decides to do a pro-rata allotment.

Total applications received are:

A12000

B10000

C2000

DEither

Pro-rata allotment means:

ARefund excess money

BPro-rata allotment with adjustment to allotment

CReject some applicants

DBoth 1 and 2

Pass the journal entries through the issue cycle.

Show answersHide answers

1. Option 1 — 12000

2. Option 2 — Pro-rata allotment with adjustment to allotment

3. Total applications = 12000; Available = 10000; Ratio = 5/6 of applied. Each applicant for 6 gets 5 shares. Excess application money per applicant = (1 share × ₹3) = ₹3 adjusted to allotment. Journal entries: (1) Bank A/c Dr 36000 (12000 × 3); To Application A/c 36000. (2) Application A/c Dr 36000; To Share Capital A/c 30000 (10000 × 3); To Allotment A/c 6000 (excess application money adjusted). (3) Bank A/c Dr 24000 (10000 × 3 − 6000 already adjusted); To Allotment A/c 24000. (4) Bank A/c Dr 20000 (10000 × 2); To First Call A/c 20000. (5) Bank A/c Dr 20000; To Final Call A/c 20000. Total capital raised = 10000 × 10 = ₹100000.

Q493 Marks

M/s Lite Ltd has 10000 equity shares of ₹10 each fully called up. Mohan held 200 shares but failed to pay the final call of ₹3 per share. Lite Ltd forfeits these shares. Later it re-issues 150 of these shares at ₹8 per share (fully paid) to a new shareholder.

Forfeiture is done:

ATo penalise default

BTo raise capital again

CBoth

DNeither

On re-issue at ₹8:

AProfit ₹750

BLoss ₹300

CProfit on re-issue transferred to Capital Reserve

DBoth 1 and 3

Pass entries for forfeiture and re-issue. Show transfer to Capital Reserve.

Show answersHide answers

1. Option 3 — Both

2. Option 4 — Both 1 and 3

3. Forfeiture: Share Capital A/c Dr 2000 (200 × 10); To Forfeited Shares A/c 1400 (200 × 7 already paid); To Final Call A/c 600 (200 × 3 unpaid). Re-issue of 150 at ₹8 fully paid: Bank A/c Dr 1200 (150 × 8); Forfeited Shares A/c Dr 300 (loss on re-issue 150 × 2); To Share Capital A/c 1500 (150 × 10). Profit on re-issue = balance in Forfeited Shares A/c after re-issue. Original forfeited per share = 7. After re-issue 150 shares of forfeited reduced by ₹2 each = 5 per share. So 150 × 5 = ₹750 still in Forfeited Shares A/c. Transfer to Capital Reserve: Forfeited Shares A/c Dr 750; To Capital Reserve A/c 750. The remaining 50 shares' forfeited amount stays until they are re-issued.

Q503 Marks

M/s Bharat Ltd issues 20000 equity shares of ₹10 each at a premium of ₹5. Application ₹4 (incl. premium ₹2); allotment ₹4 (incl. premium ₹3); first call ₹4; final call ₹3.

Securities premium account is shown under:

AReserve

BLiability

CAsset

DCapital reserve

Securities premium can NOT be used for:

ABonus issue

BCash dividend

CBuyback

DWriting off issue expenses

Explain how Securities Premium is treated and its permitted uses.

Show answersHide answers

1. Option 1 — Reserve

2. Option 2 — Cash dividend

3. Premium is the excess of issue price over face value: (15 − 10) = ₹5 per share. Total premium = 20000 × 5 = ₹100000. Allocation: Premium of ₹2 per share is collected with application (40000 total) and ₹3 per share with allotment (60000 total). Both go to Securities Premium A/c (a reserve under Schedule III). Section 52 of Companies Act 2013 specifies the limited uses of Securities Premium: (1) issue of bonus shares (fully paid); (2) writing off preliminary expenses; (3) writing off the expenses of issue of shares/debentures; (4) providing premium on redemption of preference shares/debentures; (5) buyback of shares. Cannot be used for cash dividend. Securities Premium A/c is shown under Reserves and Surplus on the balance sheet.

Q513 Marks

In the context of share capital, companies can issue different types of shares, including equity shares and preference shares. Equity shares represent ownership in the company and come with voting rights, while preference shares typically do not carry voting rights but have a fixed dividend. When a company issues shares, it must follow specific procedures, including the collection of application money, allotment money, and calls on shares. If a company receives more applications than the number of shares available, it may face over-subscription, leading to a pro-rata allotment where shares are distributed proportionately among applicants. Conversely, under-subscription occurs when fewer applications are received than the shares available, which can affect the company's capital structure and funding plans.

What are the two main types of shares mentioned in the passage?

AEquity shares and preference shares

BDebentures and bonds

CCommon shares and preferred shares

DConvertible shares and non-convertible shares

Explain the term 'pro-rata allotment' as used in the passage.

What happens during under-subscription according to the passage?

AMore applications than shares available

BFewer applications than shares available

CAll shares are fully subscribed

DShares are issued at a premium

Show answersHide answers

1. Option 1 — Equity shares and preference shares

2. Pro-rata allotment refers to the distribution of shares among applicants in proportion to the number of shares they applied for when there is over-subscription.

3. Option 2 — Fewer applications than shares available

Table-Based Questions4 questions

Q523 Marks

Types of share capital (Authorised → Paid-up):

Type

Definition

Source

Authorised

Maximum amount per memorandum

Specified in MOA

Issued

Offered to the public

Per prospectus

Subscribed

Subscribed by public

Per applications received

Called-up

Amount called from shareholders so far

Per resolutions

Paid-up

Amount actually received by company

Per receipts

Relationship of authorised and paid-up:

AAuthorised ≤ Paid-up

BAuthorised ≥ Paid-up

CPaid-up = Authorised

DRandom

Can paid-up exceed authorised capital?

AYes

BNo

CSometimes

DOnly on dividend

Why does authorised capital represent a ceiling and not actual amount raised?

Show answersHide answers

1. Option 2 — Authorised ≥ Paid-up

2. Option 2 — No

3. The hierarchy: Authorised ≥ Issued ≥ Subscribed ≥ Called-up ≥ Paid-up. Authorised capital is the maximum amount a company can raise per its memorandum. Issued capital is the part offered to the public. Subscribed capital is what the public agreed to subscribe (could be less if under-subscribed or more if over-subscribed before any pro-rata). Called-up capital is what the company has called from shareholders so far (full amount or only part if it's a partly-paid issue). Paid-up capital is what shareholders have actually paid. The difference between called-up and paid-up is 'Calls in Arrears' (a deduction from called-up on balance sheet). Calls in Advance is the OPPOSITE (paid before call) — shown as a current liability.

Q533 Marks

Treatment of premium and discount on share issue:

Item

Treatment

Section

Issue at premium

Premium credited to Securities Premium A/c

Sec 52

Use of premium

Bonus issue, writing off, premium on redemption, buyback

Sec 52(2)

Issue at discount

Generally PROHIBITED for shares

Sec 53

Sweat equity at discount

Allowed to employees/directors

Sec 54

Discount on debentures

Allowed; written off over life

—

Issue of shares at discount is generally:

AYes

BNo

CSometimes

DOnly with court approval

Securities Premium can be used for:

ABonus shares

BWorking capital

CCash dividend

DOffice expenses

Why is issue of shares at discount prohibited but discount on debentures allowed?

Show answersHide answers

1. Option 2 — No

2. Option 1 — Bonus shares

3. Section 52 of Companies Act 2013 governs Securities Premium. Premium received on issue of shares (and debentures) is credited to Securities Premium A/c. Limited uses: bonus issue of fully-paid shares, writing off preliminary expenses, writing off issue expenses, premium on redemption of preference shares/debentures, and buyback. Cannot be used for cash dividend. Section 53 generally PROHIBITS issue of shares at discount with one exception — Section 54 allows sweat equity shares at discount to employees/directors as compensation. Discount on issue of debentures is permissible (unlike shares) and is written off over the life of the debentures. The differential treatment reflects the different nature of equity (ownership) vs debt (debentures).

Q546 Marks

M/s Solar Ltd issues 10000 equity shares of ₹10 each at par. Applications received for 12000 shares; pro-rata allotment is made. Pass journal entries (assume application ₹3 allotment ₹3 first call ₹2 final call ₹2).

Quantity

Value

Shares issued

10000

Applications received

12000

Face value per share

₹10

Application money

₹3

Allotment money

₹3

First call

₹2

Final call

₹2

Q556 Marks

M/s Lite Ltd forfeits 200 shares of ₹10 each on which Mohan failed to pay final call of ₹3. Later 150 of these shares are re-issued at ₹8 fully paid. Pass journal entries.

Quantity

Value

Shares forfeited

200

Face value

₹10

Already paid (3 calls)

₹7

Unpaid final call

₹3

Re-issued

150 shares

Re-issue price (fully paid)

₹8

Picture-Based Questions3 questions

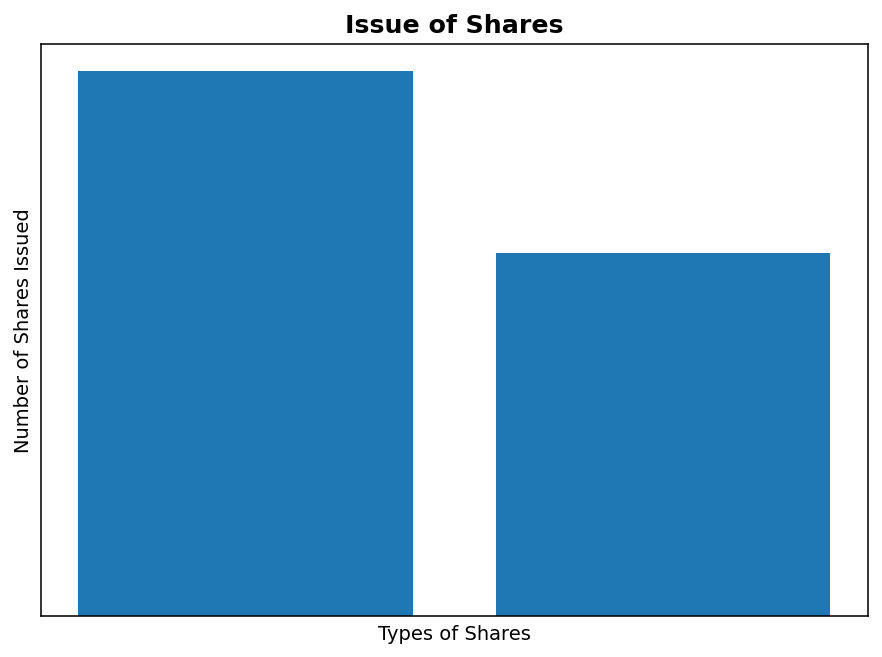

Q567 Marks

Based on the given chart, answer the following:

What is the total number of shares issued?

Which type of share has a higher issuance?

AEquity Shares

BPreference Shares

CBoth are equal

DNone of the above

What percentage of the total equity is made up of Equity Shares?

A60%

B30%

C10%

D50%

If the total equity is ₹1,000,000, how much is attributed to Preference Shares?

Which type of share had the highest issuance in category C?

AEquity Shares

BPreference Shares

CBoth are equal

DNone of the above

What is the total number of Equity Shares issued across all categories?

In which category did Preference Shares see the least issuance?

AA

BB

CC

DAll categories are equal

Which type of share capital has the highest amount?

AEquity Shares

BPreference Shares

CDebentures

DNone of the above

What is the total amount of share capital represented in the chart?

If the company decides to issue more Preference Shares, how would it affect the total capital?

Show answersHide answers

1. 500

2. Option 1 — Equity Shares

3. Option 1 — 60%

4. ₹300,000

5. Option 1 — Equity Shares

6. 600

7. Option 1 — A

8. Option 1 — Equity Shares

9. 1000000

10. The total capital would increase.

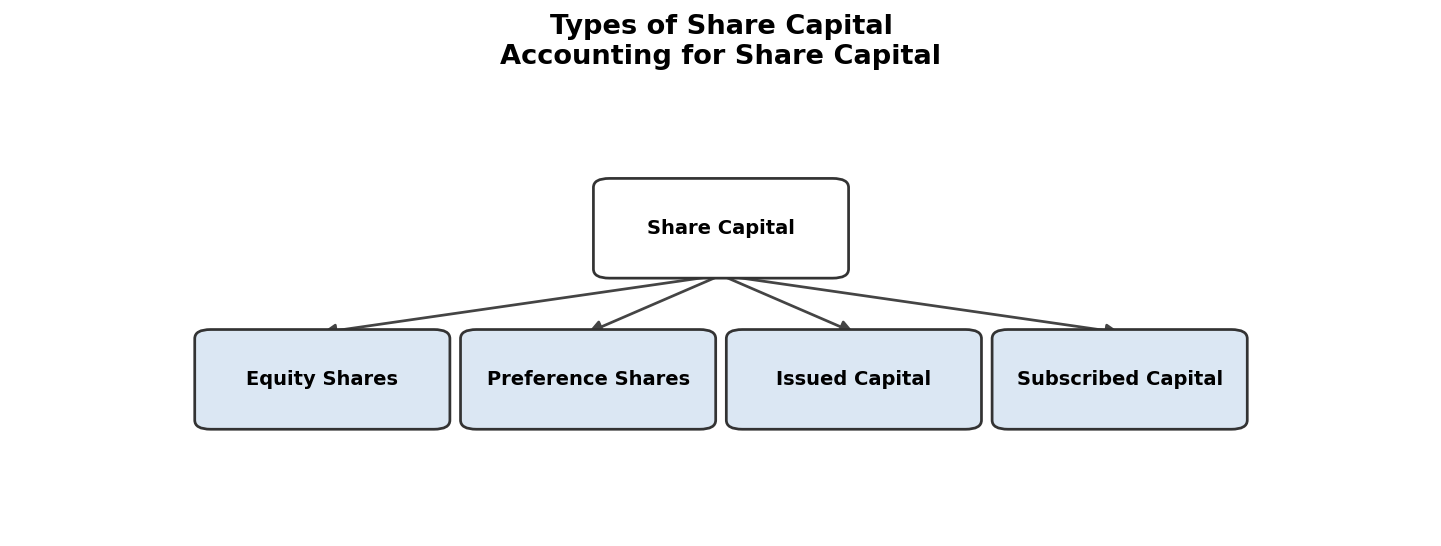

Q577 Marks

Based on the given flowchart, answer the following:

How many types of share capital are shown in the flowchart?

ATwo

BThree

CFour

DFive

What is the main category represented in the flowchart?

What initiates the forfeiture process?

ADefault on Payment

BReissue of Shares

CNotice Issued

DShares Forfeited

What is the final step in the forfeiture process?

What is the first step in the process of share forfeiture?

AIssue Notice

BForfeiture of Shares

CReissue of Shares

DTransfer to Forfeited Shares Account

What happens after the forfeiture of shares?

Which step directly follows issuing a notice to the shareholder?

AForfeiture of Shares

BReissue of Shares

CTransfer to Forfeited Shares Account

DNone of the above

What type of share capital is represented by 'Equity Shares'?

APreference Shares

BOrdinary Shares

CDebentures

DConvertible Shares

What does 'Calls in Arrears' signify in share capital?

Which type of share capital is not guaranteed a fixed dividend?

AEquity Shares

BPreference Shares

CIssued Capital

DPaid-up Capital

Show answersHide answers

1. Option 3 — Four

2. Share Capital

3. Option 1 — Default on Payment

4. Reissue of Shares

5. Option 1 — Issue Notice

6. Shares are either reissued or transferred to the forfeited shares account.

7. Option 1 — Forfeiture of Shares

8. Option 2 — Ordinary Shares

9. It signifies the amount due from shareholders that has not been paid.

10. Option 1 — Equity Shares

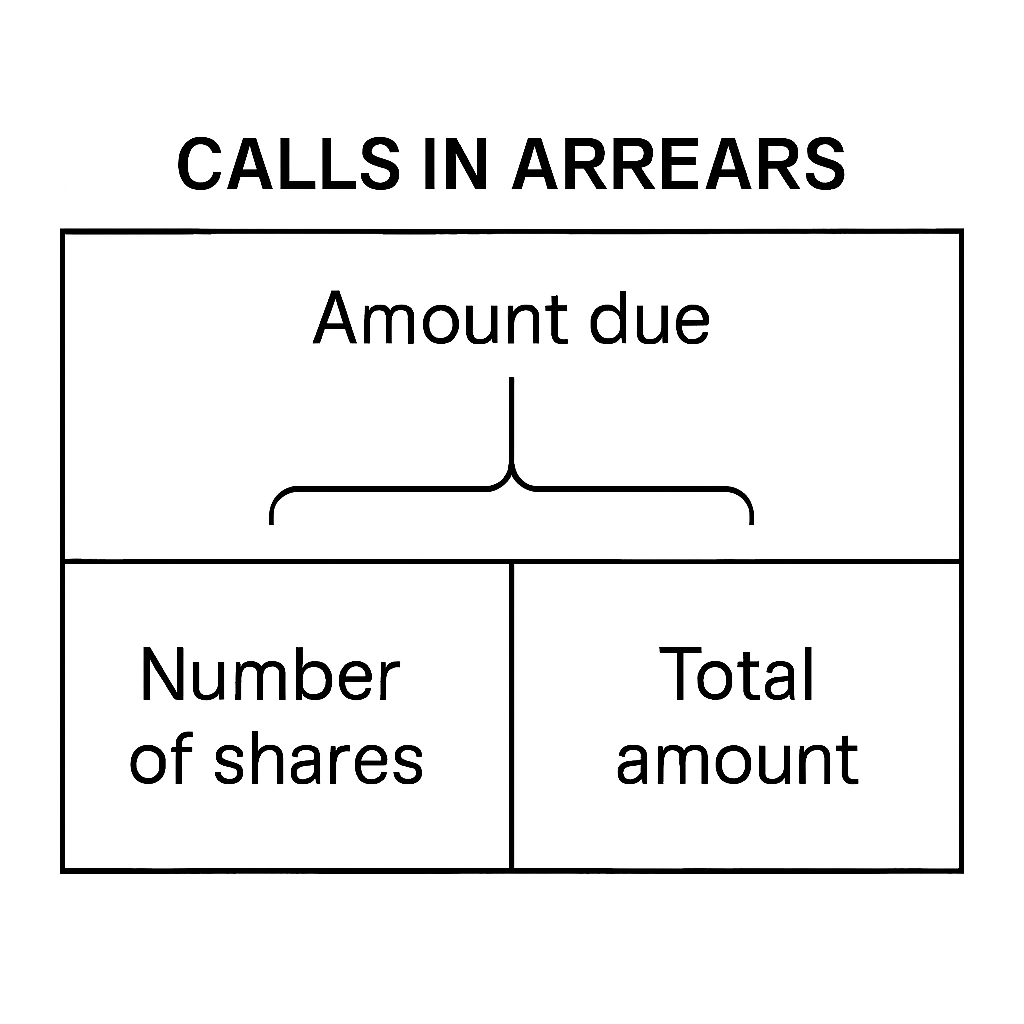

Q582 Marks

Based on the given diagram of Calls in Arrears, answer the following:

What does the diagram represent?

ACalls in Advance

BCalls in Arrears

CForfeiture of Shares

DReissue of Shares

If the amount due is ₹10,000 and the number of shares is 1000, what is the amount per share?