SUMMARY: The chapter "Issue of Debentures" in Class 12 Accountancy focuses on the accounting treatment and procedures involved in the issuance of debentures by a company. KEY TOPICS: Types of debentures, issue of debentures at par, premium, and discount, interest on debentures, redemption of debentures, journal entries for issue of debentures, debenture trust deed, debenture holders.

In the case of redeemable debentures, the company is obligated to repay the principal amount at which of the following?

AAt the end of the financial year

BAt a fixed date specified at the time of issue

CWhenever it chooses

DAt the discretion of the debenture holders

Check answerHide answer

Correct answer: Option 2 — At a fixed date specified at the time of issue

Q91 Mark

What is the primary purpose of a debenture trust deed?

ATo outline the terms of the debenture issue

BTo provide a guarantee for the debenture holders

CTo specify the interest rate on debentures

DTo determine the redemption process

Check answerHide answer

Correct answer: Option 1 — To outline the terms of the debenture issue

Q101 Mark

Which type of debenture can be converted into equity shares at the option of the holder?

ANon-Convertible Debenture

BConvertible Debenture

CRedeemable Debenture

DSecured Debenture

Check answerHide answer

Correct answer: Option 2 — Convertible Debenture

Q111 Mark

What is the accounting treatment for interest on debentures?

AIt is recorded as an expense in the Profit and Loss Account

BIt is added to the debenture account

CIt is credited to the Capital Reserve Account

DIt is shown as a liability on the balance sheet

Check answerHide answer

Correct answer: Option 1 — It is recorded as an expense in the Profit and Loss Account

Q121 Mark

If a company issues debentures at a discount, how is the discount treated in the books?

ADebited to the Profit and Loss Account

BCredited to the Debenture Account

CDebited to the Discount on Debentures Account

DIgnored in the accounting records

Check answerHide answer

Correct answer: Option 3 — Debited to the Discount on Debentures Account

Q131 Mark

Which of the following statements is true regarding debenture holders?

AThey are the owners of the company

BThey have voting rights in the company

CThey are creditors of the company

DThey are entitled to dividends

Check answerHide answer

Correct answer: Option 3 — They are creditors of the company

Q141 Mark

What is the maximum period for which a debenture can be issued?

A1 year

B5 years

C10 years

DNo maximum limit defined

Check answerHide answer

Correct answer: Option 4 — No maximum limit defined

Q151 Mark

In the case of a company issuing debentures, which of the following is a legal document that outlines the rights of debenture holders?

AMemorandum of Association

BArticles of Association

CDebenture Trust Deed

DShareholder Agreement

Check answerHide answer

Correct answer: Option 3 — Debenture Trust Deed

Short Answer Questions10 questions

Q163 Marks

Distinguish between shares and debentures.

View sample solutionHide solution

Shares — units of OWNERSHIP; shareholders are owners of the company; receive dividend (variable) only if declared; have voting rights (equity); risk and return higher; rank last in liquidation. Debentures — units of DEBT; debenture holders are creditors of the company; receive fixed interest (paid even if no profit — charged to P&L); no voting rights; rank ahead of shareholders in liquidation; can be secured against company assets. Companies use both: equity for permanent capital, debentures for fixed-cost long-term funds.

Q173 Marks

Explain the various types of debentures.

View sample solutionHide solution

(1) On security: Secured (charged on company assets) vs Unsecured (general claim only). (2) On convertibility: Convertible (can be converted to shares — fully or partially) vs Non-convertible. (3) On registration: Registered (in company books — interest sent to registered holder) vs Bearer (negotiable like cash). (4) On redemption: Redeemable (repaid at maturity) vs Irredeemable (not repaid in normal course — rare in India). (5) On priority: First mortgage debentures (priority on assets) vs Second mortgage. The choice affects interest rate, marketability, and security to investors.

Q183 Marks

How is interest on debentures treated?

View sample solutionHide solution

Interest on debentures is a CHARGE against profit (not an appropriation) — it must be paid even if there is no profit, similar to interest on a loan. Treatment: (1) Debenture Interest A/c Dr (with gross interest); To Bank A/c (after TDS deduction); To TDS A/c (tax deducted at source). (2) Debenture Interest is then transferred to P&L A/c Dr; To Debenture Interest A/c. Tax (TDS) is deposited with government. Interest is calculated on FACE VALUE (not on issue price) at the coupon rate.

Q193 Marks

Explain methods of redemption of debentures.

View sample solutionHide solution

Methods of redemption: (1) Lump sum at maturity — entire debenture amount paid on the maturity date; simple but creates large cash outflow. (2) Annual instalments — fixed annual amount over the life; smoother cash flow. (3) Purchase from open market — company buys back debentures at market price (may be at discount) when funds permit; may save interest. (4) Conversion into shares — convertible debentures are converted as per terms. SEBI rules require Debenture Redemption Reserve (DRR) of 10% of debentures redeemable value created out of profits before redemption.

Q203 Marks

What is Debenture Redemption Reserve (DRR) and why is it required?

View sample solutionHide solution

DRR is a reserve created out of profits available for dividend before debentures are redeemed. As per Companies Act and SEBI guidelines: 10% of the value of debentures to be redeemed must be transferred to DRR. Purpose: protect debenture holders by ensuring funds are set aside for redemption rather than distributed as dividends. Once redemption is complete the DRR balance can be transferred to General Reserve. Some entities (banks, NBFCs, listed companies issuing privately placed debentures) are exempt; the rule applies primarily to publicly issued debentures.

Q213 Marks

What are the key features of convertible debentures?

View sample solutionHide solution

Convertible debentures are debentures that can be converted into equity shares after a specified period. They typically offer lower interest rates compared to non-convertible debentures due to the added benefit of conversion.

Q223 Marks

Define the term 'debenture trust deed'.

View sample solutionHide solution

A debenture trust deed is a legal document that outlines the terms and conditions of the debenture issue. It includes details about the rights of debenture holders, interest payment schedules, and the obligations of the issuing company.

Q233 Marks

What is the accounting treatment for issuing debentures at a premium?

View sample solutionHide solution

When debentures are issued at a premium, the premium amount is credited to a separate account called 'Securities Premium Account'. The journal entry includes debentures being credited at par value and the premium being credited to the securities premium account.

Q243 Marks

Explain the concept of 'interest on debentures'.

View sample solutionHide solution

Interest on debentures is the cost of borrowing that a company pays to debenture holders. It is usually paid at a fixed rate and is a charge against the profits of the company, impacting the net income available to shareholders.

Q253 Marks

What is the significance of a debenture holder in a company?

View sample solutionHide solution

A debenture holder is a creditor of the company who lends money in exchange for debentures. They have a right to receive fixed interest payments and the repayment of principal at maturity, but they do not have voting rights in the company.

Long Answer Questions6 questions

Q266 Marks

M/s Sun Ltd issues 10000 9% Debentures of ₹100 each at par. Pass journal entries for: (i) application 100% received; (ii) allotment; (iii) interest for the year; (iv) interest paid (TDS @10%).

View sample solutionHide solution

(i) Bank A/c Dr 1000000 (10000 × 100); To Debenture Application A/c 1000000. (Being application money received.) (ii) Debenture Application A/c Dr 1000000; To 9% Debentures A/c 1000000. (Being debentures allotted.) (iii) Annual interest = 10000 × 100 × 9% = ₹90000. Debenture Interest A/c Dr 90000; To Debenture Holders A/c 81000 (after TDS); To TDS Payable A/c 9000. (Being interest accrued with TDS.) (iv) Debenture Holders A/c Dr 81000; To Bank A/c 81000. (Being net interest paid.) TDS Payable A/c Dr 9000; To Bank A/c 9000. (Being TDS deposited with government.) Year-end transfer: P&L A/c Dr 90000; To Debenture Interest A/c 90000.

Q276 Marks

M/s Lite Ltd issues 5000 9% debentures of ₹100 each at a discount of 6%. The discount is to be written off over the 6-year life of debentures. Pass journal entries for issue and the first year's writing off.

View sample solutionHide solution

Issue at discount of 6%: issue price = 100 − 6 = ₹94. (i) Bank A/c Dr 470000 (5000 × 94); Discount on Issue of Debentures A/c Dr 30000 (5000 × 6); To 9% Debentures A/c 500000 (face value). (Being debentures issued at 6% discount.) The discount is a deferred charge — written off proportionately over 6 years. Annual write-off = 30000 / 6 = ₹5000. Year 1: P&L A/c Dr 5000; To Discount on Issue of Debentures A/c 5000. (Being discount on issue written off.) After 6 years discount account closes. Issue at premium: opposite — Bank received ₹100 for every ₹100 face value PLUS premium credited to Securities Premium A/c.

Q286 Marks

Discuss the methods of issue of debentures with a numerical example.

View sample solutionHide solution

Methods: (1) For cash — debentures issued in exchange for money. Example: 1000 × ₹100 debentures for cash → Bank A/c Dr 100000; To Debentures A/c 100000. (2) For consideration other than cash — issued to vendors of assets in lieu of payment. Example: machine purchased for ₹500000 paid by 5000 debentures of ₹100. Machinery A/c Dr 500000; To Debentures A/c 500000. (3) As collateral security — debentures issued as additional security to a loan; entries: nominal entry only or No journal entry treating debentures as a contingent issue. The choice depends on the company's funding need and the lender's security requirement.

Q296 Marks

Explain the redemption of debentures by purchase in the open market.

View sample solutionHide solution

Open market purchase: company buys back its own debentures from the market when funds permit and prices are favourable. (1) Purchase: Investment in Own Debentures A/c Dr; To Bank A/c (with purchase price). (2) Cancellation: 9% Debentures A/c Dr (face value); To Investment in Own Debentures A/c (purchase price); difference goes to either Capital Reserve (if purchased at discount — gain) or P&L A/c (if at premium — loss). Example: Buy 100 debentures of ₹100 each at ₹95: cost 9500; cancellation entry — 9% Debentures A/c Dr 10000; To Investment in Own Debentures A/c 9500; To Capital Reserve A/c 500. The company saves 5% per debenture. This method is faster than annual instalments.

Q306 Marks

M/s Sun Ltd issues 1000 9% debentures of ₹100 each redeemable at par after 5 years. The company creates 10% DRR. Pass journal entries for issue and redemption (assume DRR is built up over time before redemption).

View sample solutionHide solution

Issue: Bank A/c Dr 100000; To 9% Debentures A/c 100000. (Being debentures issued at par.) DRR creation: Required DRR = 10% × 100000 = ₹10000. Spread over 5 years or built fully before redemption. Annual transfer: P&L Appropriation A/c Dr 2000 (over 5 years); To DRR A/c 2000. Redemption (year 5): 9% Debentures A/c Dr 100000; To Debenture Holders A/c 100000. Debenture Holders A/c Dr 100000; To Bank A/c 100000. (Being debentures redeemed at par.) Transfer DRR back: DRR A/c Dr 10000; To General Reserve A/c 10000. (Being DRR transferred to General Reserve after redemption.)

Q316 Marks

Compare shares and debentures with the help of a table on at least five features.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): A debenture is a long-term debt instrument.

Reason (R): Debenture holders are creditors of the company and receive a fixed interest.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Interest on debentures is a charge against profit not an appropriation.

Reason (R): Interest must be paid even when the company has no profit; it is similar to interest on a loan.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): A Debenture Redemption Reserve protects debenture holders.

Reason (R): The reserve ensures that funds are set aside for redemption rather than distributed as dividend.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Convertible debentures can be converted into equity shares.

Reason (R): Conversion provides debenture holders with potential capital appreciation in addition to fixed interest.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Discount on issue of debentures is written off over the life of the debentures.

Reason (R): The discount represents an additional cost of borrowing that should be amortised over the period of benefit.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): Debentures can be issued at a premium to attract investors.

Reason (R): Issuing at a premium increases the funds raised for the company.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): Interest on debentures is payable only if the company makes a profit.

Reason (R): Interest on debentures is a fixed charge and must be paid regardless of profit.

Show explanationHide explanation

Correct answer: Option 4 —

A is false, but R is true.

Q391 Mark

Assertion (A): A debenture trust deed outlines the rights of debenture holders.

Reason (R): The trust deed serves as a legal contract between the company and the debenture holders.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: Debentures are debt and shares are ownership.

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Debentures can be secured or unsecured convertible or non-convertible.

Statement 2: The choice affects interest rate and marketability.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Debentures may be issued for cash for non-cash consideration or as collateral security.

Statement 2: Each method has different accounting treatment.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Redemption can be by lump sum instalments open market purchase or conversion.

Statement 2: The method depends on company finances and the terms of issue.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: A Debenture Redemption Reserve must be created before redemption.

Statement 2: DRR is set at 10% of debentures redeemable value.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: Debentures can only be issued at par value.

Statement 2: Debentures can be issued at a premium or discount depending on market conditions.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q461 Mark

Statement 1: Interest on debentures is paid before tax.

Statement 2: Debenture holders are considered part owners of the company.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: A debenture trust deed outlines the rights of debenture holders.

Statement 2: Debenture holders do not have voting rights in a company.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Case Study / Passage Questions4 questions

Q483 Marks

M/s Sun Ltd issues 10000 9% debentures of ₹100 each at par on 1 April 2023 redeemable at par after 5 years. Annual interest is paid half-yearly. The TDS rate on debenture interest is 10%.

Interest on debentures is treated as:

ACharge against profit

BAppropriation of profit

CReserve transfer

DOptional

Total annual interest payable on the debentures is:

A₹45000

B₹90000

C₹50000

D₹100000

Pass journal entries for issue and one year of interest payment.

Show answersHide answers

1. Option 1 — Charge against profit

2. Option 2 — ₹90000

3. Annual interest = Face value × rate = 10000 × 100 × 9% = ₹90000. Half-yearly interest = ₹45000 paid in two instalments. Journal entries (annual): (1) Bank A/c Dr (10000 × 100) 1000000; To Debenture Application 1000000. (2) Debenture Application A/c Dr 1000000; To 9% Debentures A/c 1000000. (3) Annual interest accrual: Debenture Interest A/c Dr 90000; To Debenture Holders A/c 81000 (after TDS); To TDS Payable A/c 9000. (4) Payment: Debenture Holders A/c Dr 81000; To Bank A/c 81000. TDS Payable A/c Dr 9000; To Bank A/c 9000. Year-end: P&L A/c Dr 90000; To Debenture Interest A/c 90000.

Q493 Marks

M/s Lite Ltd issues 5000 9% debentures of ₹100 each at a discount of 6% on 1 April 2023. The debentures are redeemable at par after 6 years. The discount on issue must be written off over the life of the debentures.

The issue price per debenture is:

A₹100

B₹94

C₹106

D₹6

Discount on issue of debentures is treated as:

AAsset

BLiability

CNegative reserve

DDeferred charge written off over life

Pass journal entries for issue and the first year's write-off.

Show answersHide answers

1. Option 2 — ₹94

2. Option 4 — Deferred charge written off over life

3. Issue at 6% discount: Issue price = 100 − 6 = ₹94. Total face value = 5000 × 100 = ₹500000; Total discount = 5000 × 6 = ₹30000. Annual write-off = 30000 / 6 years = ₹5000 per year. Journal entries (issue): Bank A/c Dr 470000; Discount on Issue of Debentures A/c Dr 30000; To 9% Debentures A/c 500000. (Being debentures issued at 6% discount.) Year 1 write-off: P&L A/c Dr 5000; To Discount on Issue of Debentures A/c 5000. (Being discount written off proportionately.) After 6 years discount account closes — total ₹30000 written off. The discount is shown as a reduction from Reserves and Surplus on the balance sheet (or under Other Non-current Assets if amortised).

Q503 Marks

M/s Crown Ltd had issued 1000 8% debentures of ₹100 each redeemable at par after 5 years. As per Companies Act it must create a Debenture Redemption Reserve (DRR) at 10% of debentures redeemable value before redemption. The company decides to redeem all debentures on the maturity date.

The DRR amount required is:

A₹10000

B₹50000

C₹100000

D₹0

DRR is created from:

AOut of capital

BOut of profits available for dividend

CFrom cash balance

DFrom reserves any source

Compute DRR and pass entries for the redemption.

Show answersHide answers

1. Option 1 — ₹10000

2. Option 2 — Out of profits available for dividend

3. Required DRR = 10% × Total face value = 10% × 1000 × 100 = ₹10000. DRR can be built up over time before redemption. Common practice: build over the life of the debentures, transferring part of profit to DRR each year. For 5-year life, DRR transfer = 10000 / 5 = ₹2000 per year. Journal: P&L Appropriation A/c Dr 2000; To DRR A/c 2000. (Being DRR contribution from profit.) Redemption (year 5): 8% Debentures A/c Dr 100000; To Debenture Holders A/c 100000. Debenture Holders A/c Dr 100000; To Bank A/c 100000. (Being debentures redeemed.) After redemption: DRR A/c Dr 10000; To General Reserve A/c 10000. (Being DRR transferred to General Reserve since redemption is complete.) The purpose of DRR is to ensure funds are set aside for redemption rather than distributed as dividends.

Q514 Marks

Debentures are a popular means of raising funds for companies. They are essentially a type of debt instrument that companies issue to borrow money from the public. When a company issues debentures, it promises to pay a fixed rate of interest to the debenture holders at specified intervals. The principal amount is usually repaid at the end of the debenture's term. Debentures can be issued at par, at a premium, or at a discount. The terms of the debenture issue, including the interest rate and redemption conditions, are specified in a document known as the debenture trust deed. This document outlines the rights of debenture holders and the obligations of the company. Understanding the accounting treatment for debentures is crucial for accurate financial reporting and compliance with legal requirements.

What is a debenture?

Which document outlines the rights of debenture holders?

ADebenture Trust Deed

BShareholder Agreement

CCompany Bylaws

DFinancial Statement

What are the three ways debentures can be issued?

AAt par, at a premium, or at a discount

BAt face value, at market value, or at book value

CAs secured, unsecured, or convertible

DAs equity, debt, or hybrid

Why is understanding the accounting treatment for debentures important?

Show answersHide answers

1. A debenture is a type of debt instrument that companies issue to borrow money from the public.

2. Option 1 — Debenture Trust Deed

3. Option 1 — At par, at a premium, or at a discount

4. It is crucial for accurate financial reporting and compliance with legal requirements.

Table-Based Questions4 questions

Q523 Marks

Compare types of debentures:

Type

Distinction

Example

Secured vs Unsecured

Charged on assets vs general claim

Mortgage debentures vs simple debentures

Convertible vs Non-convertible

Can be converted to shares vs cannot

FCD/PCD vs NCD

Registered vs Bearer

Registered in books vs negotiable

Indian companies issue registered

Redeemable vs Irredeemable

Repaid at maturity vs not repaid normally

Most are redeemable

First mortgage vs Second mortgage

Priority on assets

First has higher security

A debenture that can be converted into equity shares is:

AConvertible

BNon-convertible

CBoth

DNeither

A debenture backed by mortgage on assets is:

ASecured

BUnsecured

CConvertible

DBearer

Why does the choice of debenture type affect the interest rate?

Show answersHide answers

1. Option 1 — Convertible

2. Option 1 — Secured

3. Debentures can be classified by various features. Secured debentures are charged on specific assets and have priority on those assets in liquidation; unsecured (also called naked) debentures have a general claim only. Convertible debentures (FCD/PCD — Fully/Partly Convertible) can be converted to shares per agreed terms, giving holders potential capital appreciation. Non-Convertible Debentures (NCDs) stay as debt. Registered debentures are registered in company books — interest sent to registered holder. Bearer debentures are negotiable — whoever holds them gets the interest. Most Indian companies issue registered debentures. The choice of type affects the interest rate (more secure types have lower rates) and marketability.

Q533 Marks

Methods of issue of debentures and their accounting:

Method

Description

Accounting

For cash

Issued for cash payment

Bank A/c Dr; To Debentures A/c

For non-cash consideration

Issued to vendor in lieu of payment for asset

Asset A/c Dr; To Debentures A/c

As collateral security

Issued as additional security to a loan

Nominal entry only; no real exchange

At par

Face value = issue price

Bank = Debentures

At premium

Issue price > face value

Bank = Debentures + Premium

At discount

Issue price < face value

Bank + Discount = Debentures

For non-cash consideration the entry is:

ABank A/c Dr To Debentures A/c

BAsset A/c Dr To Debentures A/c

CLoan A/c Dr To Debentures A/c

DNo entry

Issue at premium credits the Securities Premium A/c.

AYes

BNo

CSometimes

DOptional

Compare the three methods of issue and their accounting impact.

Show answersHide answers

1. Option 2 — Asset A/c Dr To Debentures A/c

2. Option 1 — Yes

3. Debentures can be issued for cash for non-cash consideration (e.g. to vendors of assets) or as collateral security. The accounting depends on the method: cash issue is a simple Bank-to-Debenture transfer; non-cash uses the Asset acquired as the debit; collateral often involves only a nominal entry since no real exchange of value happens. Premium and discount affect the bank receipt vs face value: premium is credited to Securities Premium A/c (under Section 52); discount is a deferred charge written off over the life of the debentures. The choice depends on the company's circumstances and the market's perception of its credit worthiness.

Q546 Marks

M/s Sun Ltd issues 10000 9% debentures of ₹100 each at par on 1 April 2023 redeemable after 5 years. Compute annual interest and pass entries (TDS @10%).

Quantity

Value

Debentures issued

10000

Face value per debenture

₹100

Coupon rate

9%

Issue price

at par

Redemption period

5 years

TDS rate

10%

Q556 Marks

M/s Lite Ltd issues 5000 9% debentures of ₹100 each at a discount of 6% redeemable after 6 years. Pass journal entries for issue and the first year's writing off.

Quantity

Value

Debentures issued

5000

Face value

₹100

Discount

6%

Issue price

₹94

Life

6 years

Annual write-off

? ₹5000

Picture-Based Questions3 questions

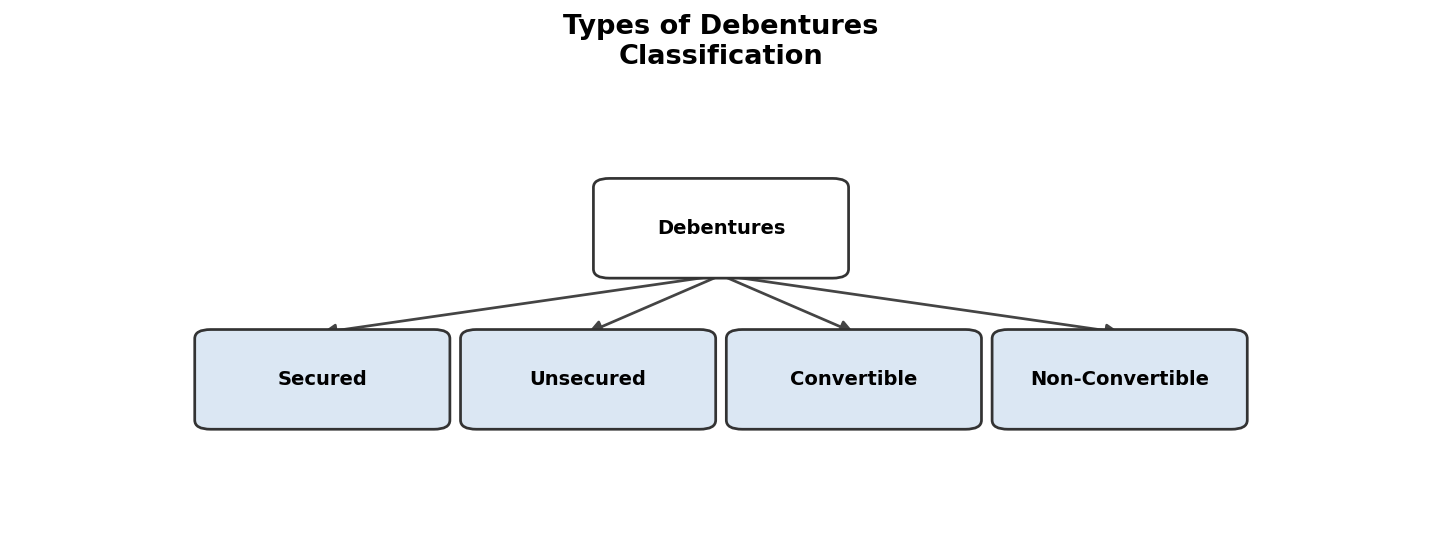

Q562 Marks

Based on the given flowchart, answer the following:

What type of debenture is not backed by any collateral?

ASecured

BUnsecured

CConvertible

DNon-Convertible

Name one type of secured debenture.

What is one method of redeeming debentures before maturity?

AAt Maturity

BBy Purchase

CBy Conversion

DNone of the above

Explain the term 'redemption at maturity'.

Show answersHide answers

1. Option 2 — Unsecured

2. Mortgage Debenture

3. Option 2 — By Purchase

4. Repayment of the principal amount on the due date.

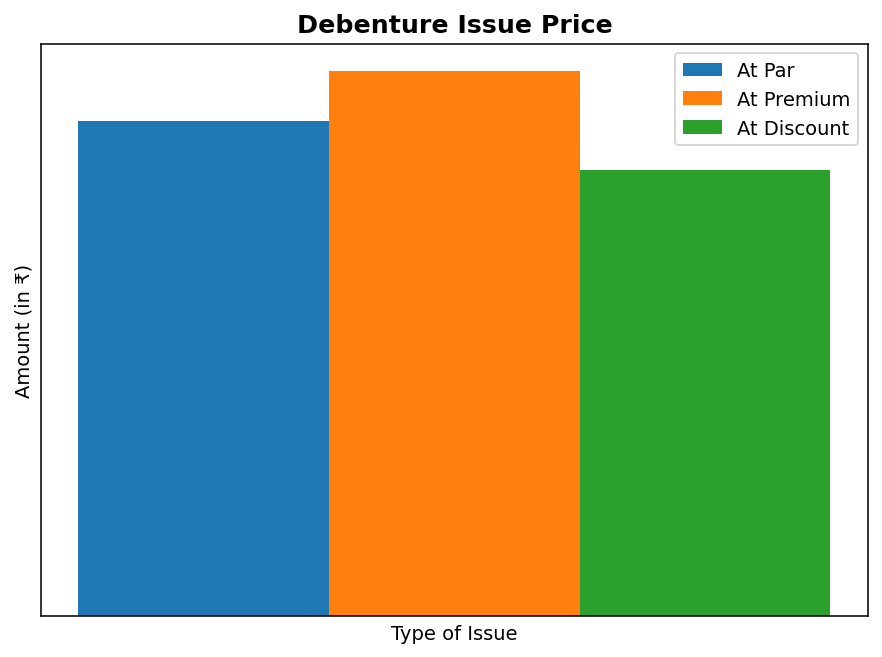

Q572 Marks

Based on the given chart, answer the following:

Which type of debenture is issued at ₹110?

AAt Par

BAt Premium

CAt Discount

DNone of the above

What is the issue price of debentures at discount?

Which type of debenture has the highest interest payment?

ASecured Debentures

BUnsecured Debentures

CConvertible Debentures

DNon-Convertible Debentures

What percentage of interest is paid on Non-Convertible Debentures?

Show answersHide answers

1. Option 2 — At Premium

2. ₹90

3. Option 1 — Secured Debentures

4. 10%

Q582 Marks

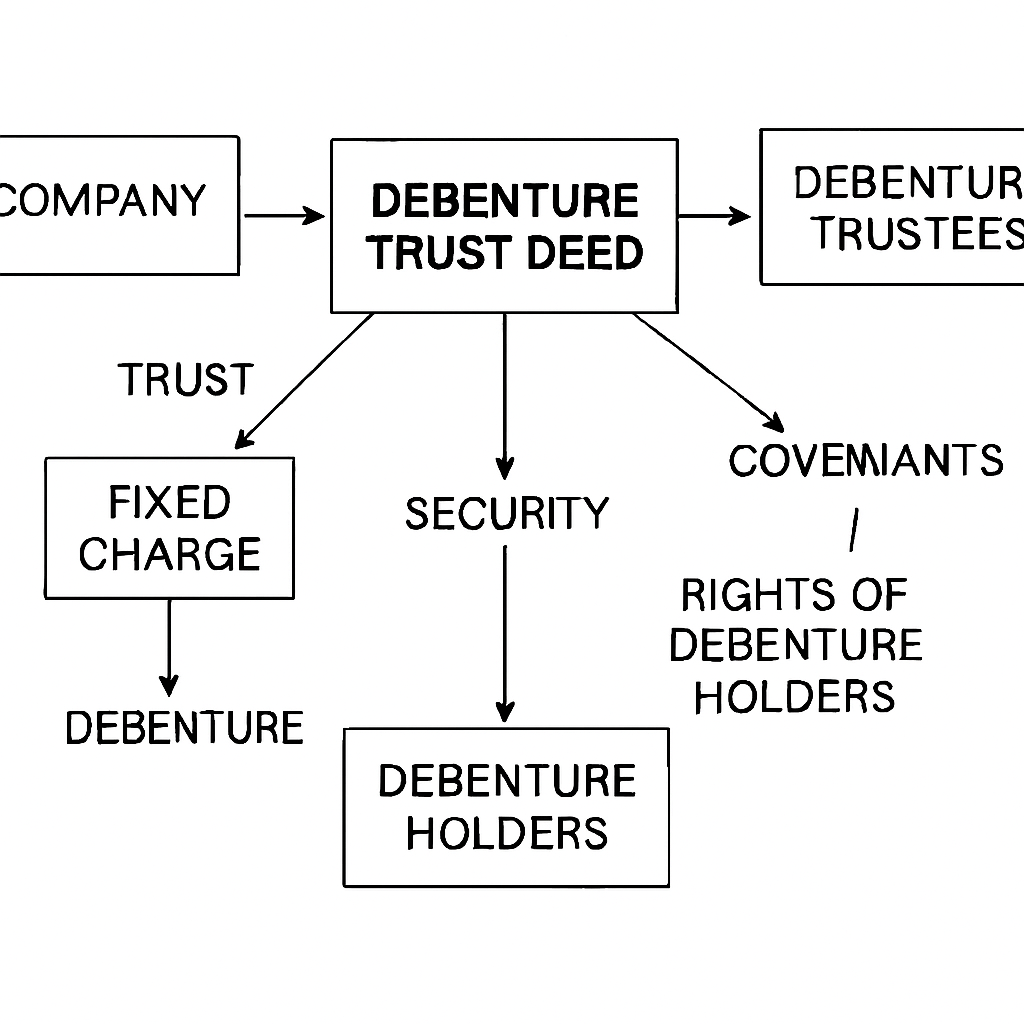

Based on the given diagram of a debenture trust deed, answer the following:

What is the primary purpose of a debenture trust deed?

Which party is typically responsible for managing the trust deed?