SUMMARY: The chapter on Accounting Ratios in Class 12 Accountancy focuses on the analysis and interpretation of financial statements using various ratios to assess the financial health and performance of a business. KEY TOPICS: Liquidity ratios, Solvency ratios, Activity ratios, Profitability ratios, Current ratio, Quick ratio, Debt to equity ratio, Inventory turnover ratio, Return on investment, Earnings per share.

Correct answer: Option 2 — Current Assets / Current Liabilities

Q21 Mark

Quick ratio excludes:

ACash

BInventories and prepaid expenses

CTrade receivables

DBank

Check answerHide answer

Correct answer: Option 2 — Inventories and prepaid expenses

Q31 Mark

Debt-equity ratio measures:

ALiquidity

BProfitability

CSolvency

DActivity

Check answerHide answer

Correct answer: Option 3 — Solvency

Q41 Mark

Inventory turnover ratio measures:

AProfitability

BLiquidity

CActivity (efficiency)

DSolvency

Check answerHide answer

Correct answer: Option 3 — Activity (efficiency)

Q51 Mark

Return on Equity is calculated as:

ANet Profit / Total Sales

BNet Profit / Average Equity

CNet Profit / Total Assets

DOperating Profit / Sales

Check answerHide answer

Correct answer: Option 2 — Net Profit / Average Equity

Q61 Mark

Which of the following ratios is primarily used to assess a company's ability to meet its short-term obligations?

ADebt to Equity Ratio

BCurrent Ratio

CReturn on Investment

DInventory Turnover Ratio

Check answerHide answer

Correct answer: Option 2 — Current Ratio

Q71 Mark

What does a high Quick Ratio indicate about a company's liquidity position?

AThe company has a high level of inventory

BThe company can cover its current liabilities without relying on inventory

CThe company is highly leveraged

DThe company has low profitability

Check answerHide answer

Correct answer: Option 2 — The company can cover its current liabilities without relying on inventory

Q81 Mark

The formula for calculating the Debt to Equity Ratio is:

ATotal Assets / Total Liabilities

BTotal Liabilities / Shareholders' Equity

CShareholders' Equity / Total Assets

DTotal Equity / Total Liabilities

Check answerHide answer

Correct answer: Option 2 — Total Liabilities / Shareholders' Equity

Q91 Mark

Which of the following is NOT a liquidity ratio?

ACurrent Ratio

BQuick Ratio

CDebt to Equity Ratio

DCash Ratio

Check answerHide answer

Correct answer: Option 3 — Debt to Equity Ratio

Q101 Mark

The Inventory Turnover Ratio is calculated to determine:

AHow quickly a company can sell its inventory

BThe profitability of a company

CThe company's debt levels

DThe efficiency of asset utilization

Check answerHide answer

Correct answer: Option 1 — How quickly a company can sell its inventory

Q111 Mark

If a company has a Current Ratio of 1.5, what does this indicate?

AThe company has more current liabilities than current assets

BThe company has equal current assets and current liabilities

CThe company has 1.5 times more current assets than current liabilities

DThe company is in financial distress

Check answerHide answer

Correct answer: Option 3 — The company has 1.5 times more current assets than current liabilities

Q121 Mark

Which of the following ratios is used to measure profitability?

ACurrent Ratio

BReturn on Investment

CDebt to Equity Ratio

DQuick Ratio

Check answerHide answer

Correct answer: Option 2 — Return on Investment

Q131 Mark

A company with a low Debt to Equity Ratio is generally considered:

AHigh risk

BLow risk

CHighly profitable

DIlliquid

Check answerHide answer

Correct answer: Option 2 — Low risk

Q141 Mark

The formula for calculating Earnings per Share (EPS) is:

ANet Income / Total Shares Outstanding

BTotal Revenue / Total Assets

CNet Profit / Total Equity

DNet Income / Total Liabilities

Check answerHide answer

Correct answer: Option 1 — Net Income / Total Shares Outstanding

Q151 Mark

Which of the following statements is true about the Quick Ratio?

AIt includes all current assets

BIt excludes cash and cash equivalents

CIt provides a more stringent measure of liquidity than the Current Ratio

DIt is not a measure of liquidity

Check answerHide answer

Correct answer: Option 3 — It provides a more stringent measure of liquidity than the Current Ratio

Short Answer Questions10 questions

Q163 Marks

List the major categories of accounting ratios with one example each.

View sample solutionHide solution

(1) LIQUIDITY ratios — current ratio, quick (acid-test) ratio. Measure short-term solvency. (2) SOLVENCY ratios — debt-equity ratio, interest coverage ratio. Measure long-term financial stability. (3) PROFITABILITY ratios — gross profit ratio, net profit ratio, return on equity, return on capital employed. Measure earning capacity. (4) ACTIVITY (turnover) ratios — inventory turnover, debtors turnover, asset turnover. Measure efficiency in use of assets. Each category provides different insights into the financial health of the firm.

Q173 Marks

Distinguish between current ratio and quick ratio.

View sample solutionHide solution

Current Ratio = Current Assets / Current Liabilities. Includes ALL current assets (inventories prepaid expenses also). Standard: 2:1 (means current assets twice the current liabilities). Quick Ratio (acid-test ratio) = (Current Assets − Inventories − Prepaid expenses) / Current Liabilities. Excludes inventories (slow to liquidate) and prepaid (not realisable in cash). Standard: 1:1 — quick assets equal current liabilities. Quick ratio is a stricter test of immediate liquidity; current ratio is a broader test. Both are computed from the balance sheet.

Q183 Marks

Explain debt-equity ratio and its significance.

View sample solutionHide solution

Debt-Equity Ratio = Long-term Debt / Shareholders' Funds. (Some authors use Total Debt / Equity.) Measures the LEVERAGE of the firm — proportion of debt to equity in capital structure. Standard: 2:1 (debt twice equity is acceptable for many industries; varies by sector). Significance: (1) High ratio means high financial risk — large interest commitment must be served even in bad years; (2) Low ratio means lower risk but possibly under-utilising leverage; (3) Lenders use it to assess credit risk; (4) Equity investors check whether the firm is over-leveraged. The ideal ratio depends on industry, business cycle, and management's risk appetite.

Q193 Marks

Define inventory turnover ratio. State its formula and standard.

View sample solutionHide solution

Inventory Turnover Ratio = Cost of Goods Sold (COGS) / Average Inventory. (Some authors use Net Sales as numerator if COGS unavailable.) Average Inventory = (Opening + Closing Stock) / 2. Measures how many times the inventory has been sold and replaced during the period. A high ratio indicates: (a) efficient inventory management; (b) good demand for products; (c) less risk of obsolescence. A low ratio indicates: (a) over-stocking; (b) slow-moving items; (c) potential write-downs. Standard varies by industry — supermarkets ~10-15, jewellers ~3-5. Days inventory = 365 / Inventory Turnover gives the average days inventory is held.

Q203 Marks

Explain return on capital employed (ROCE) and its computation.

View sample solutionHide solution

ROCE = (Earnings Before Interest and Tax / Capital Employed) × 100. Capital Employed = Shareholders' Funds + Long-term Debt (or Total Assets − Current Liabilities). Measures the overall profitability of the firm in relation to its long-term financing. Comparison with cost of capital tells whether the firm is creating or destroying value. Higher ROCE is better. Use cases: (a) inter-firm comparison — firms in same industry; (b) intra-firm — track over years; (c) comparison with cost of capital — must exceed it. Limitations: based on book values not market values; sensitive to depreciation methods; doesn't account for risk.

Q213 Marks

What is the current ratio, and how is it calculated?

View sample solutionHide solution

The current ratio measures a company's ability to pay its short-term liabilities with its short-term assets. It is calculated by dividing current assets by current liabilities. A ratio above 1 indicates good short-term financial health.

Q223 Marks

Define quick ratio and explain its importance in financial analysis.

View sample solutionHide solution

The quick ratio, also known as the acid-test ratio, measures a company's ability to meet its short-term obligations without relying on the sale of inventory. It is calculated by subtracting inventory from current assets and dividing by current liabilities. This ratio provides a more stringent assessment of liquidity than the current ratio.

Q233 Marks

What does the debt to equity ratio indicate about a company?

View sample solutionHide solution

The debt to equity ratio indicates the relative proportion of shareholders' equity and debt used to finance a company's assets. A higher ratio suggests greater financial risk, as it indicates that a company is more leveraged and relies more on borrowed funds.

Q243 Marks

Explain the significance of the inventory turnover ratio in business operations.

View sample solutionHide solution

The inventory turnover ratio indicates how efficiently a company manages its inventory by showing how many times inventory is sold and replaced over a period. A higher ratio suggests efficient inventory management, while a lower ratio may indicate overstocking or weak sales.

Q253 Marks

What is return on investment (ROI), and how is it calculated?

View sample solutionHide solution

Return on investment (ROI) measures the profitability of an investment relative to its cost. It is calculated by dividing the net profit from the investment by the initial cost of the investment and multiplying by 100 to get a percentage. A higher ROI indicates a more profitable investment.

Long Answer Questions6 questions

Q266 Marks

Compute the following ratios from this data: Current Assets ₹150000 (incl. inventory ₹40000 and prepaid ₹5000); Current Liabilities ₹75000; Net Sales ₹500000; Gross Profit ₹150000; Net Profit ₹50000; Total Equity ₹400000; Long-term Debt ₹200000; Average Inventory ₹35000; COGS ₹350000.

View sample solutionHide solution

(1) Current Ratio = 150000 / 75000 = 2:1. Liquidity is healthy. (2) Quick Ratio = (150000 − 40000 − 5000) / 75000 = 105000 / 75000 = 1.4:1. Above standard 1:1. (3) Debt-Equity Ratio = 200000 / 400000 = 0.5:1. Conservative leverage. (4) Gross Profit Ratio = (150000 / 500000) × 100 = 30%. (5) Net Profit Ratio = (50000 / 500000) × 100 = 10%. (6) Inventory Turnover = COGS / Avg Inventory = 350000 / 35000 = 10 times. Inventory replaced 10 times in the year. (7) Return on Equity = (50000 / 400000) × 100 = 12.5%. The firm is liquid solvent moderately profitable and efficient in inventory management.

Q276 Marks

Discuss the importance and limitations of ratio analysis.

View sample solutionHide solution

Importance: (1) Quick assessment of financial position — ratios summarise large amounts of data into single figures; (2) Aid in decision-making for investors lenders managers; (3) Trend identification — comparing ratios over years reveals patterns; (4) Inter-firm comparison — common ratios apply across firms of different sizes; (5) Performance benchmarking — comparing with industry standards. Limitations: (1) Based on historical figures — does not predict future; (2) Window dressing of accounts can manipulate ratios; (3) Different accounting policies make inter-firm comparison difficult; (4) Inflation distorts ratios over time; (5) No single ratio is enough — must use a balanced set; (6) Qualitative factors (brand quality reputation) are not captured. Despite limitations ratio analysis is one of the most widely used analytical tools.

Q286 Marks

Discuss the relationship between gross profit ratio, net profit ratio, and operating profit ratio.

View sample solutionHide solution

Gross Profit Ratio = (Gross Profit / Net Sales) × 100 = (Net Sales − COGS) / Net Sales × 100. Reflects the efficiency of trading or production activities — how much margin is left after direct costs. Operating Profit Ratio = (Operating Profit / Net Sales) × 100. Operating Profit = Gross Profit − Operating Expenses (excludes interest tax extraordinary items). Measures core operating efficiency. Net Profit Ratio = (Net Profit / Net Sales) × 100. After ALL expenses including interest tax. Final indicator of overall profitability. Relationship: GP Ratio ≥ Operating Profit Ratio ≥ Net Profit Ratio. The gap between GP and operating profit reveals indirect/operating expenses; the gap between operating profit and net profit reveals interest tax and exceptional items. Together they provide a layered view of profitability.

Q296 Marks

Compute the various activity ratios: Net Sales ₹600000; Average Trade Receivables ₹50000; Cost of Goods Sold ₹400000; Average Inventory ₹40000; Total Assets ₹500000; Average Working Capital ₹100000.

View sample solutionHide solution

(1) Debtors Turnover Ratio = Net Credit Sales / Avg Trade Receivables = 600000 / 50000 = 12 times. Average collection period = 365 / 12 = 30 days. (2) Inventory Turnover Ratio = COGS / Avg Inventory = 400000 / 40000 = 10 times. Days inventory = 365 / 10 = 36.5 days. (3) Total Asset Turnover Ratio = Net Sales / Total Assets = 600000 / 500000 = 1.2 times. Each ₹1 of assets generates ₹1.20 of sales. (4) Working Capital Turnover Ratio = Net Sales / Working Capital = 600000 / 100000 = 6 times. Working capital is rotated 6 times in the year. Activity ratios reveal how efficiently resources are being used to generate sales — higher is generally better.

Q306 Marks

Discuss the importance of liquidity and solvency ratios separately and explain how they relate.

View sample solutionHide solution

Liquidity ratios (current quick) measure SHORT-TERM solvency — ability to meet obligations falling due within 12 months. A low liquidity ratio means the firm may default on supplier payments salaries short-term loans. A very high ratio may indicate idle current assets. Solvency ratios (debt-equity interest coverage) measure LONG-TERM solvency — ability to honour long-term debt obligations. A high debt-equity ratio means the firm carries significant fixed financial commitments (interest); a low interest coverage means earnings are barely sufficient to pay interest. Relationship: a firm can be liquid but insolvent (e.g., enough cash now but heavy LT debt) or solvent but illiquid (good capital structure but cash crunch). Both must be monitored. Crisis arises when both deteriorate simultaneously.

Q316 Marks

Differentiate between liquidity ratios and solvency ratios in tabular form on five features.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): Current ratio measures short-term liquidity.

Reason (R): Current ratio compares current assets to current liabilities to assess ability to meet near-term obligations.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Quick ratio is a stricter test of liquidity than current ratio.

Reason (R): Quick ratio excludes inventories and prepaid expenses which are not immediately realisable in cash.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): A high debt-equity ratio indicates greater financial risk.

Reason (R): High debt means higher interest commitments that must be met regardless of profit.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): A higher inventory turnover ratio is generally better.

Reason (R): High turnover indicates efficient inventory management and good demand for products.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Return on Capital Employed measures the overall profitability of a firm.

Reason (R): ROCE relates earnings before interest and tax to total long-term capital employed.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): The liquidity ratios help assess a company's ability to meet its short-term obligations.

Reason (R): Liquidity ratios include the current ratio and quick ratio, which provide insights into financial health.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): A higher current ratio indicates better liquidity.

Reason (R): The current ratio is calculated by dividing current assets by current liabilities.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q391 Mark

Assertion (A): The debt to equity ratio is used to measure a company's profitability.

Reason (R): The debt to equity ratio primarily assesses financial leverage and risk, not profitability.

Show explanationHide explanation

Correct answer: Option 3 —

A is true, but R is false.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: The standard current ratio is 2:1.

Statement 2: A ratio below 1:1 indicates liquidity stress.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Gross profit ratio measures trading efficiency.

Statement 2: Net profit ratio measures overall profitability after all expenses.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Inventory turnover ratio reflects efficiency in inventory management.

Statement 2: High turnover indicates fast-moving stock and lower obsolescence risk.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Interest coverage ratio = EBIT / Interest expense.

Statement 2: A higher ratio indicates greater ability to meet interest obligations.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Ratios should be interpreted with industry context.

Statement 2: Comparison with industry averages is more meaningful than absolute thresholds.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: The quick ratio is a measure of a company's short-term liquidity, excluding inventory from current assets.

Statement 2: A current ratio of 1:1 indicates that a company has sufficient assets to cover its liabilities.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q461 Mark

Statement 1: A higher debt to equity ratio indicates a higher level of financial risk.

Statement 2: Profitability ratios are used to assess a company's ability to generate earnings relative to sales, assets, or equity.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q471 Mark

Statement 1: The inventory turnover ratio is calculated by dividing cost of goods sold by average inventory.

Statement 2: A low inventory turnover ratio may indicate overstocking or weak sales.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Case Study / Passage Questions4 questions

Q483 Marks

M/s Sangam Stores has Current Assets ₹150000 (incl. inventory ₹40000 and prepaid ₹5000); Current Liabilities ₹75000. The bank wants liquidity ratios before lending.

Current Ratio =

ACurrent Ratio = 2:1

BCurrent Ratio = 1.5:1

CCurrent Ratio = 3:1

DCurrent Ratio = 1:1

Quick Ratio =

A1.4:1

B1:1

C2:1

D1.5:1

Compute current and quick ratios and interpret for the bank.

Show answersHide answers

1. Option 1 — Current Ratio = 2:1

2. Option 1 — 1.4:1

3. Current Ratio = Current Assets / Current Liabilities = 150000 / 75000 = 2:1. Quick Ratio = (Current Assets − Inventory − Prepaid) / Current Liabilities = (150000 − 40000 − 5000) / 75000 = 105000 / 75000 = 1.4:1. Both above the standard (current 2:1, quick 1:1). Healthy liquidity. Interpretation: M/s Sangam can comfortably meet short-term obligations. Even excluding the slow-to-convert inventory and prepaid, ₹1.40 of quick assets are available for every ₹1 of current liability. The bank would view this favourably for short-term lending. Caveat: too high a ratio (e.g., 5:1) might indicate idle current assets — over-stocking or excess cash not deployed productively.

Q493 Marks

M/s Suri Ltd has Long-term Debt ₹400000; Shareholders' Funds (Equity + Reserves) ₹500000; EBIT ₹120000; Annual Interest expense ₹40000.

Debt-Equity Ratio =

A1.25:1

B0.8:1

C2:1

D1:2

Interest Coverage Ratio =

A3 times

B2 times

C4 times

D5 times

Compute D/E and interest coverage ratios and interpret.

Show answersHide answers

1. Option 2 — 0.8:1

2. Option 1 — 3 times

3. Debt-Equity Ratio = Long-term Debt / Shareholders' Funds = 400000 / 500000 = 0.8:1. Below the standard of 2:1 — moderate leverage with conservative capital structure. Interest Coverage Ratio = EBIT / Interest = 120000 / 40000 = 3 times. The firm earns 3 times its interest commitment. Standard: at least 1.5x, comfortably 3x+. Interpretation: M/s Suri Ltd has comfortable solvency — debt is moderate and earnings cover interest 3 times over. The firm has capacity to take on more debt if needed (without becoming risky). Lenders would view this positively. Risk: sharp drop in EBIT could erode this comfort — interest commitment is rigid while EBIT is variable.

Q503 Marks

M/s Dhruv Industries has Net Sales ₹600000; Cost of Goods Sold ₹400000; Net Profit ₹50000; Average Inventory ₹40000; Average Trade Receivables ₹50000; Total Equity ₹400000.

Gross Profit Ratio =

A33%

B50%

C8.3%

D15%

Inventory Turnover Ratio =

A10 times

B12 times

C15 times

D5 times

Compute the various ratios and interpret each.

Show answersHide answers

1. Option 1 — 33%

2. Option 1 — 10 times

3. Gross Profit Ratio = (Gross Profit / Net Sales) × 100 = (200000 / 600000) × 100 = 33.33%. Net Profit Ratio = (50000 / 600000) × 100 = 8.33%. Inventory Turnover Ratio = COGS / Avg Inventory = 400000 / 40000 = 10 times. Days inventory = 365 / 10 = 36.5 days. Debtors Turnover Ratio = Net Sales / Avg Trade Receivables = 600000 / 50000 = 12 times. Days collection = 365 / 12 = 30 days. Return on Equity = (Net Profit / Equity) × 100 = (50000 / 400000) × 100 = 12.5%. Interpretation: GP ratio 33% is healthy; NP ratio 8% is moderate (gap shows operating expenses); inventory turns 10x and collection in 30 days indicate efficient operations; ROE of 12.5% is acceptable. The firm is profitable, operationally efficient, and provides reasonable return to equity holders.

Q513 Marks

Accounting ratios are essential tools for analyzing the financial health of a business. They provide insights into various aspects such as liquidity, profitability, and solvency. Liquidity ratios, like the current ratio and quick ratio, help assess a company's ability to meet short-term obligations. Solvency ratios, including the debt to equity ratio, evaluate long-term financial stability. Activity ratios, such as inventory turnover, measure how efficiently a company utilizes its assets. Profitability ratios, including return on investment and earnings per share, indicate how well a company generates profit relative to its sales or equity. By interpreting these ratios, stakeholders can make informed decisions regarding investments, credit, and management strategies.

What do liquidity ratios primarily assess?

ALong-term financial stability

BAbility to meet short-term obligations

CEfficiency in asset utilization

DOverall profitability

Define the term 'debt to equity ratio'.

Which of the following is a profitability ratio?

ACurrent ratio

BQuick ratio

CReturn on investment

DInventory turnover ratio

Show answersHide answers

1. Option 2 — Ability to meet short-term obligations

2. The debt to equity ratio is a financial ratio that compares a company's total liabilities to its shareholder equity, indicating the relative proportion of debt and equity used to finance the company's assets.

3. Option 3 — Return on investment

Table-Based Questions4 questions

Q523 Marks

Categories of accounting ratios:

Category

What it measures

Examples

Liquidity

Short-term solvency

Current ratio, Quick ratio

Solvency

Long-term financial stability

Debt-equity ratio, Interest coverage

Profitability

Earning capacity

GP ratio, NP ratio, ROCE

Activity (Turnover)

Efficiency in asset use

Inventory turnover, Debtors turnover

Quick ratio falls under which category?

ALiquidity

BSolvency

CProfitability

DActivity

Profitability ratios include:

AGP Ratio

BNP Ratio

CROCE

DAll

Why is a balanced analysis using ratios from all four categories preferred?

Show answersHide answers

1. Option 1 — Liquidity

2. Option 4 — All

3. Ratios are categorised by purpose. Liquidity ratios measure ability to meet short-term obligations (within 12 months) — current ratio quick ratio. Solvency ratios measure long-term financial stability — debt-equity ratio interest coverage capital gearing. Profitability ratios measure earning capacity — gross profit ratio net profit ratio operating profit ratio return on capital employed return on equity. Activity (turnover) ratios measure efficiency in use of assets — inventory turnover debtors turnover total asset turnover working capital turnover. A complete analysis uses ratios from all four categories to give a balanced view.

Q533 Marks

Common ratios and their formulas:

Ratio

Formula

Standard

Current Ratio

Current Assets / Current Liabilities

2:1

Quick Ratio

(CA - Inventory - Prepaid) / CL

1:1

Debt-Equity

LT Debt / Shareholders' Funds

2:1 (varies)

GP Ratio

(Gross Profit / Net Sales) × 100

Industry-specific

NP Ratio

(Net Profit / Net Sales) × 100

Industry-specific

Inventory Turnover

COGS / Avg Inventory

Industry-specific

ROE

(Net Profit / Avg Equity) × 100

15% or higher

Inventory Turnover Ratio formula:

AEBIT / Sales

BCOGS / Avg Inventory

CNet Profit / Sales

DSales / COGS

Standard Current Ratio is:

A1:1

B2:1

C3:1

D4:1

Why are ratio standards industry-specific?

Show answersHide answers

1. Option 2 — COGS / Avg Inventory

2. Option 2 — 2:1

3. Each ratio uses specific data from financial statements: balance sheet (current ratio quick ratio debt-equity); P&L (GP NP ROE); both (inventory turnover debtors turnover). Standards vary by industry — supermarkets have low GP ratio (~10%) but high turnover; jewellers have high GP ratio (~30%) but low turnover. Always benchmark against industry peers. Ratios are most meaningful when (a) compared with prior years (trend); (b) compared with industry averages (benchmark); (c) used together rather than in isolation. A single ratio out of context can mislead — a high current ratio could indicate good liquidity OR idle current assets.

Q546 Marks

Compute the various accounting ratios of M/s Sangam Stores from the given data.

Item

Amount

Current Assets

₹150000

Inventory

₹40000

Prepaid expenses

₹5000

Current Liabilities

₹75000

Net Sales

₹500000

Gross Profit

₹150000

Net Profit

₹50000

Total Equity

₹400000

Long-term Debt

₹200000

Average Inventory

₹35000

COGS

₹350000

Q556 Marks

Classify these ratios into liquidity solvency profitability and activity categories.

Ratio

Category

Current Ratio

? Liquidity

Quick Ratio

? Liquidity

Debt-Equity Ratio

? Solvency

Interest Coverage Ratio

? Solvency

Gross Profit Ratio

? Profitability

Net Profit Ratio

? Profitability

Inventory Turnover

? Activity

Debtors Turnover

? Activity

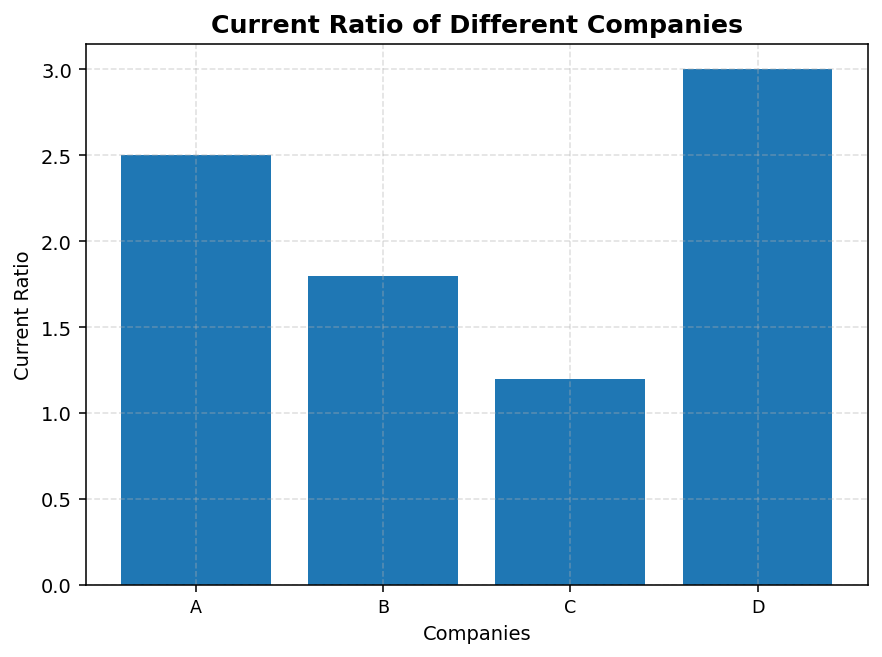

Picture-Based Questions3 questions

Q562 Marks

Based on the given chart, answer the following:

Which company has the highest current ratio?

ACompany A

BCompany B

CCompany C

DCompany D

What does a current ratio above 2 indicate?

Which profitability ratio has the highest percentage?

AReturn on Investment

BEarnings per Share

CNet Profit Margin

DGross Profit Margin

What does a higher return on investment indicate?

Show answersHide answers

1. Option 4 — Company D

2. The company has good liquidity.

3. Option 2 — Earnings per Share

4. Better profitability and efficiency in generating returns.

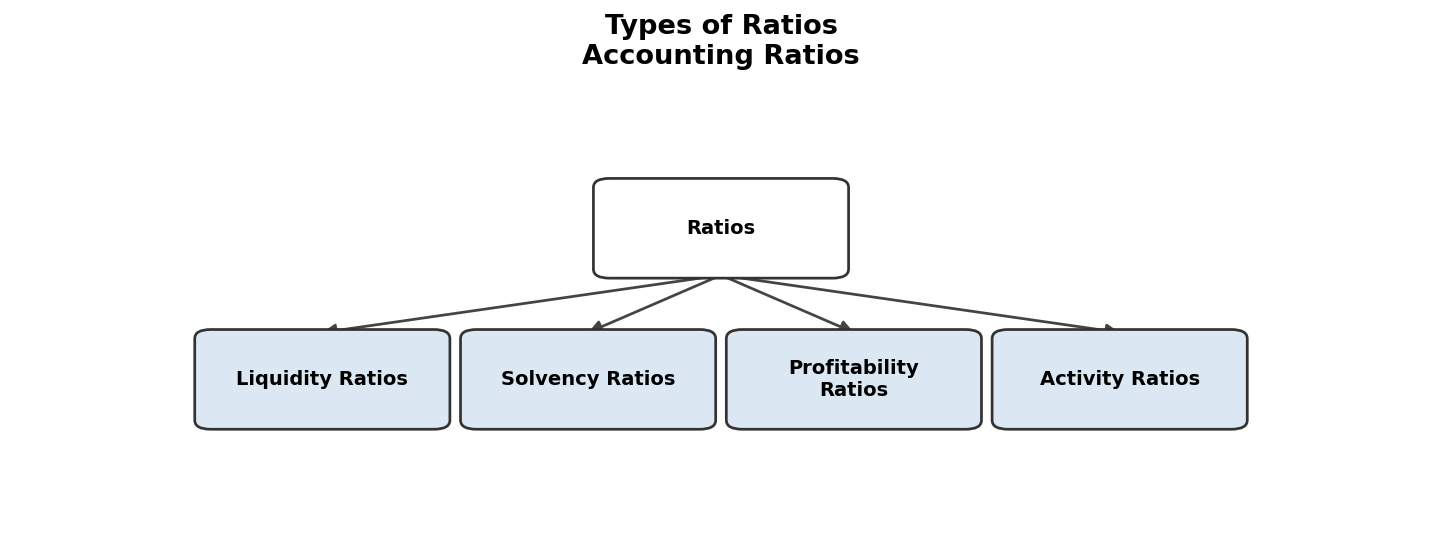

Q572 Marks

Based on the given flowchart, answer the following:

How many types of ratios are shown in the flowchart?

A2

B3

C4

D5

What type of ratio assesses a company's ability to meet short-term obligations?

What does the Debt to Equity Ratio measure?

ALiquidity

BProfitability

CSolvency

DActivity

What is the significance of a high Debt to Equity Ratio?

Show answersHide answers

1. Option 3 — 4

2. Liquidity Ratios

3. Option 3 — Solvency

4. It indicates higher financial risk.

Q582 Marks

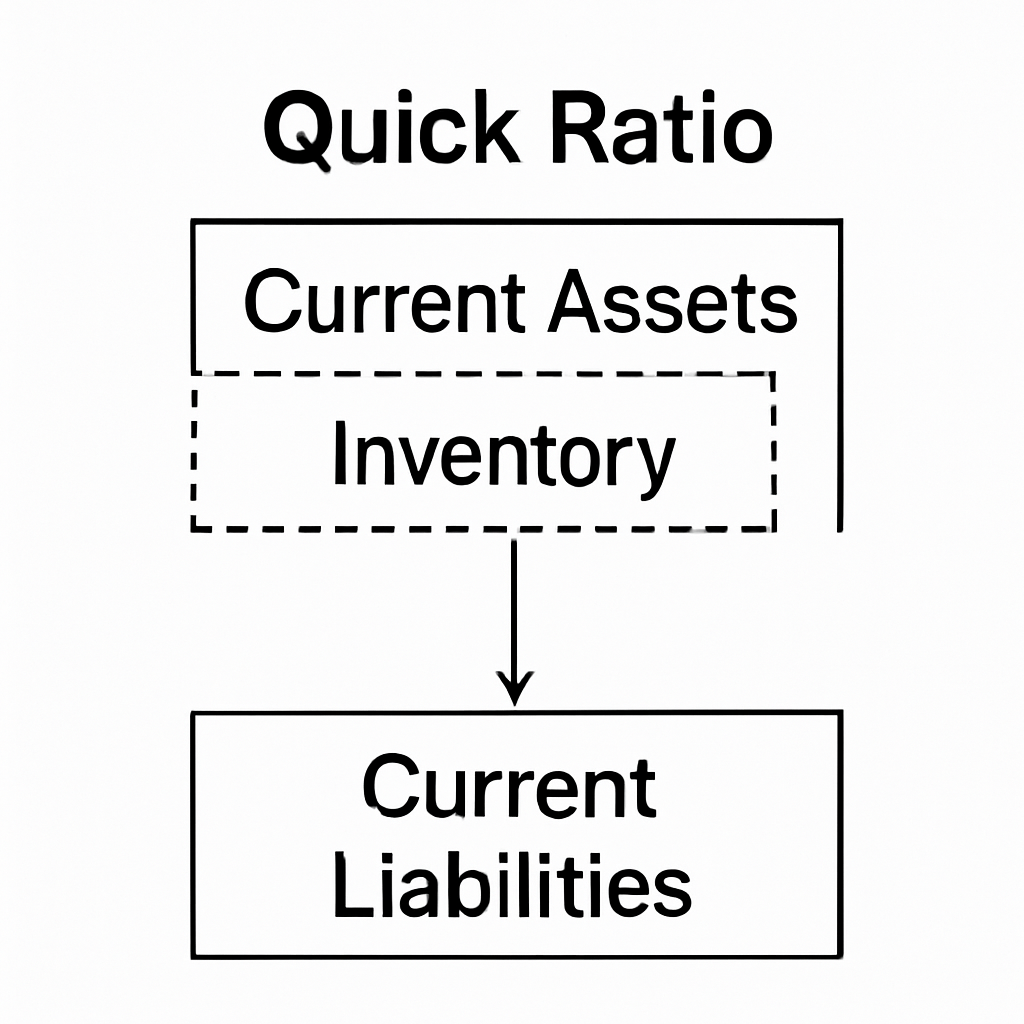

Based on the given diagram, answer the following:

What is the formula for calculating the Quick Ratio?

Why is inventory excluded in the Quick Ratio calculation?

Show answersHide answers

1. Quick Ratio = (Current Assets - Inventory) / Current Liabilities

2. Because inventory may not be easily liquidated.