SUMMARY: The chapter on Cash Flow Statement in Class 12 Accountancy focuses on understanding the preparation and analysis of cash flow statements as per the accounting standards. KEY TOPICS: Cash flow from operating activities, cash flow from investing activities, cash flow from financing activities, direct method, indirect method, cash and cash equivalents, non-cash transactions, significance of cash flow statement, preparation of cash flow statement, limitations of cash flow statement.

Which of the following is NOT a component of cash flow from operating activities?

ACash receipts from customers

BCash payments to suppliers

CSale of equipment

DCash payments for operating expenses

Check answerHide answer

Correct answer: Option 3 — Sale of equipment

Q71 Mark

In the cash flow statement, which method involves adjusting net income for changes in working capital?

ADirect method

BIndirect method

CHybrid method

DStandard method

Check answerHide answer

Correct answer: Option 2 — Indirect method

Q81 Mark

Which of the following is considered a cash equivalent?

AShort-term investments

BAccounts receivable

CInventory

DLong-term bonds

Check answerHide answer

Correct answer: Option 1 — Short-term investments

Q91 Mark

Which activity would be classified under cash flow from investing activities?

APayment of wages

BPurchase of machinery

CIssuance of debentures

DPayment of dividends

Check answerHide answer

Correct answer: Option 2 — Purchase of machinery

Q101 Mark

What is the significance of the cash flow statement?

AIt shows the profitability of a company

BIt provides information about cash inflows and outflows

CIt reflects the company's market value

DIt summarizes the equity of the company

Check answerHide answer

Correct answer: Option 2 — It provides information about cash inflows and outflows

Q111 Mark

Which of the following transactions is classified as a non-cash transaction?

AIssuing shares for cash

BAcquisition of assets through a loan

CCash sales to customers

DPayment of cash for expenses

Check answerHide answer

Correct answer: Option 2 — Acquisition of assets through a loan

Q121 Mark

When preparing a cash flow statement using the direct method, which of the following is included?

ANet income

BCash received from customers

CDepreciation expense

DChanges in accounts payable

Check answerHide answer

Correct answer: Option 2 — Cash received from customers

Q131 Mark

Which of the following is NOT a limitation of the cash flow statement?

ADoes not provide information about profitability

BIgnores non-cash transactions

CDoes not reflect future cash flows

DShows only cash transactions

Check answerHide answer

Correct answer: Option 4 — Shows only cash transactions

Q141 Mark

What type of cash flow is generated from the sale of a long-term asset?

AOperating cash flow

BInvesting cash flow

CFinancing cash flow

DNon-operating cash flow

Check answerHide answer

Correct answer: Option 2 — Investing cash flow

Q151 Mark

Which of the following is an example of cash flow from financing activities?

APayment of interest

BSale of investments

CIssuance of shares

DPurchase of inventory

Check answerHide answer

Correct answer: Option 3 — Issuance of shares

Short Answer Questions10 questions

Q163 Marks

Define cash flow statement and state its objectives.

View sample solutionHide solution

Cash Flow Statement is a financial statement that shows the inflow and outflow of cash and cash equivalents during a period classified into three activities — operating investing and financing. Objectives: (1) Provide information about cash receipts and payments; (2) Show how the company has generated and used cash; (3) Help assess liquidity and solvency; (4) Help users predict future cash flows; (5) Show the relationship between profit and cash flow (net profit ≠ cash). Mandatory under AS-3 and Companies Act 2013 for companies above specified threshold.

Q173 Marks

Explain the three activities under which cash flows are classified.

View sample solutionHide solution

OPERATING activities: cash flows from primary revenue-generating activities — receipts from sales of goods/services; payments to suppliers; payments to and on behalf of employees; tax payments. INVESTING activities: cash flows from acquisition and disposal of non-current assets — purchase/sale of fixed assets investments and intangibles; loans given. FINANCING activities: cash flows that result in changes in size and composition of equity and borrowings — issue of shares debentures or borrowings; repayment of debt; payment of dividend interest. The three-way split reveals how the company is funded and where its money is going.

Q183 Marks

Distinguish between direct and indirect methods of preparing cash flow from operating activities.

View sample solutionHide solution

DIRECT METHOD: directly lists major classes of cash receipts and payments (cash from sales cash to suppliers cash to employees etc.). Provides clearer information but requires extensive cash book analysis. Less commonly used. INDIRECT METHOD: starts with net profit before tax and adjusts for: (a) non-cash items (depreciation amortisation); (b) operating items not affecting cash this period (changes in receivables payables inventories); (c) items shown elsewhere (interest dividend gain/loss on sale of fixed assets). More commonly used because it reconciles profit and cash flow. Indian companies typically use indirect method.

Q193 Marks

How is depreciation treated in the cash flow statement under indirect method?

View sample solutionHide solution

Depreciation is a NON-CASH expense — it reduces profit but does not involve cash outflow. Under the indirect method (which starts with net profit before tax) depreciation is ADDED BACK to profit to arrive at cash flow from operating activities. Treatment: Net Profit Before Tax + Depreciation + Amortisation + Loss on sale of fixed assets − Gain on sale of fixed assets ± changes in working capital items = Cash from Operating Activities. The same logic applies to other non-cash items.

Q203 Marks

Explain the treatment of interest paid and dividend paid in cash flow statement.

View sample solutionHide solution

Interest PAID: in case of NON-FINANCIAL companies — treated as FINANCING activity (cash outflow). For financial companies (banks NBFCs) — operating activity. Dividend PAID: always FINANCING activity (cash outflow to equity holders). Interest RECEIVED: NON-FINANCIAL — INVESTING activity; FINANCIAL — operating. Dividend RECEIVED: NON-FINANCIAL — INVESTING activity; FINANCIAL — operating. The rationale: interest and dividends are returns from/on capital — for non-financial companies these are not part of the main business. Indian standard AS-3 specifies these treatments.

Q213 Marks

What are cash and cash equivalents, and why are they important in a cash flow statement?

View sample solutionHide solution

Cash and cash equivalents include cash on hand, demand deposits, and short-term investments that are easily convertible to cash. They are important in a cash flow statement as they represent the liquidity of a company and its ability to meet short-term obligations.

Q223 Marks

Describe the significance of a cash flow statement for stakeholders in a business.

View sample solutionHide solution

A cash flow statement provides stakeholders, such as investors and creditors, with insights into a company's cash generation and usage. It helps assess the company's liquidity, financial health, and ability to generate cash for future growth.

Q233 Marks

What is the difference between cash flow from operating activities and cash flow from investing activities?

View sample solutionHide solution

Cash flow from operating activities refers to cash generated or used in the core business operations, while cash flow from investing activities involves cash transactions for the purchase or sale of long-term assets. Both are essential for understanding a company's overall cash position.

Q243 Marks

Explain how non-cash transactions are reported in a cash flow statement.

View sample solutionHide solution

Non-cash transactions, such as barter exchanges or depreciation, are not included in the cash flow statement as they do not affect cash. However, they may be disclosed in the notes to the financial statements to provide additional context to stakeholders.

Q253 Marks

How do changes in working capital affect the cash flow from operating activities?

View sample solutionHide solution

Changes in working capital, such as increases in accounts receivable or inventory, can decrease cash flow from operating activities, while decreases in these accounts can increase cash flow. This reflects the cash impact of operational efficiency and management of current assets and liabilities.

Long Answer Questions6 questions

Q266 Marks

Calculate Cash from Operating Activities (indirect method) from the following: Net Profit Before Tax ₹100000; Depreciation ₹20000; Loss on Sale of Asset ₹5000; Increase in Trade Receivables ₹15000; Decrease in Inventories ₹10000; Increase in Trade Payables ₹8000; Income Tax Paid ₹25000.

View sample solutionHide solution

Cash from Operating Activities (Indirect Method): Net Profit Before Tax 100000. ADD non-cash items: Depreciation 20000; Loss on sale of asset 5000. = 125000. Adjust for changes in working capital: Less Increase in Trade Receivables 15000; Add Decrease in Inventories 10000; Add Increase in Trade Payables 8000. = 125000 − 15000 + 10000 + 8000 = 128000. Less Income Tax Paid 25000. CASH FROM OPERATING ACTIVITIES = 128000 − 25000 = ₹103000. The adjustments convert accrual-based net profit to cash basis.

Q276 Marks

Compute Cash from Investing Activities from: Purchase of fixed assets ₹120000; Sale of investments ₹30000; Sale of fixed asset for ₹15000 (book value ₹20000); Interest received on investments ₹5000; Purchase of investments ₹40000.

View sample solutionHide solution

Cash from Investing Activities: Outflows — Purchase of fixed assets (120000); Purchase of investments (40000) = (160000). Inflows — Sale of investments 30000; Sale of fixed assets 15000; Interest received 5000 = 50000. NET CASH USED IN INVESTING = 50000 − 160000 = (110000). The loss on sale of fixed asset (book value 20000 − sale 15000 = ₹5000) does NOT enter investing activities directly — it was already added back to profit in operating activities (since it is a non-cash loss). Only the actual cash inflow ₹15000 from the sale enters investing.

Q286 Marks

Compute Cash from Financing Activities from: Proceeds from issue of equity shares ₹200000; Proceeds from debentures issue ₹100000; Repayment of long-term loan ₹50000; Dividend paid ₹40000; Interest paid ₹15000.

View sample solutionHide solution

Cash from Financing Activities: Inflows — Proceeds from issue of shares 200000; Proceeds from debentures 100000 = 300000. Outflows — Repayment of long-term loan (50000); Dividend paid (40000); Interest paid (15000) = (105000). NET CASH FROM FINANCING = 300000 − 105000 = ₹195000. Financing activities reflect changes in equity and long-term borrowings; the firm has raised ₹300000 in capital and used ₹105000 for repayments and distributions netting +₹195000 inflow.

Q296 Marks

Prepare a complete cash flow statement from the following: Operating activities — Net Profit Before Tax ₹150000, Depreciation ₹30000, Increase in receivables ₹25000, Decrease in inventories ₹15000, Tax paid ₹35000. Investing activities — Purchase of fixed assets ₹120000, Sale of investments ₹20000. Financing activities — Issue of shares ₹100000, Repayment of debentures ₹50000, Dividend paid ₹20000.

View sample solutionHide solution

CASH FLOW STATEMENT for the year ended 31 March 2024. (A) Operating: NP Before Tax 150000 + Depreciation 30000 = 180000; Less Increase in Receivables (25000); Add Decrease in Inventories 15000; = 170000. Less Tax paid (35000). Cash from Operating = 135000. (B) Investing: Purchase of fixed assets (120000) + Sale of investments 20000 = (100000). Cash used in Investing = (100000). (C) Financing: Issue of shares 100000 + Repayment of debentures (50000) + Dividend paid (20000) = 30000. Cash from Financing = 30000. Net increase in cash = 135000 − 100000 + 30000 = 65000. Add Opening cash balance + Net increase = Closing cash balance.

Q306 Marks

Explain the format of cash flow statement under indirect method and the treatment of various items.

View sample solutionHide solution

Format under indirect method (AS-3): I. CASH FROM OPERATING ACTIVITIES — start with NP Before Tax; ADD non-cash items (depreciation amortisation goodwill written off loss on sale of fixed asset); SUBTRACT non-operating items already included (gain on sale interest received dividend received); adjust for working capital changes (increase in current assets or decrease in current liabilities = subtract; opposite = add); subtract income tax paid. II. CASH FROM INVESTING — purchases and sales of fixed assets/investments; interest/dividend received (for non-financial companies). III. CASH FROM FINANCING — issue of shares debentures borrowings (inflows); repayment dividend interest paid (outflows). Net change = I + II + III; opening + net change = closing cash and cash equivalents.

Q316 Marks

Differentiate between cash flow statement and fund flow statement in tabular form.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): Cash flows are classified into operating investing and financing activities.

Reason (R): Each category captures cash flows from a different aspect of business operations.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Depreciation is added back to net profit in the indirect method.

Reason (R): Depreciation is a non-cash expense that does not involve outflow of cash.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): Interest paid by a non-financial company is shown under financing activities.

Reason (R): Interest paid represents the cost of borrowing — directly related to financing decisions.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Dividend paid is shown under financing activities.

Reason (R): Dividend paid is a return to shareholders related to the financing of the company.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): The indirect method reconciles net profit with cash flow.

Reason (R): The indirect method starts with profit and adjusts for non-cash and non-operating items.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): Cash flow from operating activities includes cash receipts from customers.

Reason (R): Cash flow from operating activities is derived from the core business operations of a company.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): The direct method of preparing a cash flow statement is more commonly used than the indirect method.

Reason (R): The direct method provides a clearer view of cash inflows and outflows.

Show explanationHide explanation

Correct answer: Option 4 —

A is false, but R is true.

Q391 Mark

Assertion (A): Cash equivalents are short-term investments that are easily convertible to cash.

Reason (R): Cash equivalents include items like treasury bills and commercial paper.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: The cash flow statement shows how the firm has generated and used cash.

Statement 2: It complements the P&L Account and Balance Sheet.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Cash from operating activities is the primary source of long-term funding.

Statement 2: Insufficient cash from operations indicates underlying business problems.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Investing activities reflect long-term capital deployment.

Statement 2: Net negative investing cash flow often indicates capital expansion.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Financing activities reflect changes in equity and borrowings.

Statement 2: Net positive financing cash flow indicates the firm has raised more capital than it has returned.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Cash equivalents are short-term highly liquid investments.

Statement 2: They include money in bank fixed deposits with maturity less than 3 months.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: Cash flow from operating activities includes cash received from customers and cash paid to suppliers.

Statement 2: Cash flow from investing activities includes cash transactions for the purchase and sale of fixed assets.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q461 Mark

Statement 1: The direct method of preparing the cash flow statement is more commonly used than the indirect method.

Statement 2: The indirect method adjusts net income for changes in non-cash items and working capital.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: Cash equivalents can include stocks and bonds that are easily convertible to cash.

Statement 2: Cash equivalents must have a maturity of three months or less from the date of acquisition.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Case Study / Passage Questions4 questions

Q483 Marks

M/s Sundar Stores has these data for FY 2023-24: Net Profit Before Tax ₹100000; Depreciation ₹20000; Loss on Sale of Asset ₹5000; Increase in Trade Receivables ₹15000; Decrease in Inventories ₹10000; Increase in Trade Payables ₹8000; Income Tax Paid ₹25000.

The method described is:

ADirect

BIndirect

CEither

DBoth

Depreciation in indirect method is:

AAdd to net profit

BSubtract from net profit

CNo effect

DGoes to investing

Compute cash from operating activities and explain the adjustments.

Show answersHide answers

1. Option 2 — Indirect

2. Option 1 — Add to net profit

3. Cash from Operating Activities (Indirect Method): Net Profit Before Tax 100000. ADD non-cash items: Depreciation 20000; Loss on sale of asset 5000. = 125000. Adjust for changes in working capital: Less Increase in Trade Receivables 15000; Add Decrease in Inventories 10000; Add Increase in Trade Payables 8000. = 125000 − 15000 + 10000 + 8000 = 128000. Less Income Tax Paid 25000. CASH FROM OPERATING ACTIVITIES = 128000 − 25000 = ₹103000. The adjustments convert accrual-based net profit to cash basis. Logic: depreciation is non-cash (added back); changes in working capital reflect timing differences between earning revenue and receiving cash.

Q493 Marks

M/s Verma Ltd has these investing activities for FY 2023-24: Purchase of Fixed Assets ₹120000; Sale of Investments ₹30000; Sale of Fixed Asset for ₹15000 (book value ₹20000); Interest received on investments ₹5000; Purchase of Investments ₹40000.

Sale of investments is shown under:

AOperating

BInvesting

CFinancing

DOperating + Investing

Purchase of fixed assets represents:

ACash inflow

BCash outflow

CBoth

DNo effect

Compute cash from investing activities and explain treatment of loss on sale.

Show answersHide answers

1. Option 2 — Investing

2. Option 2 — Cash outflow

3. Cash from Investing Activities: Outflows — Purchase of fixed assets (120000); Purchase of investments (40000) = (160000). Inflows — Sale of investments 30000; Sale of fixed assets 15000; Interest received 5000 = 50000. NET CASH USED IN INVESTING = 50000 − 160000 = (110000). Note: The loss on sale of fixed asset (book value 20000 − sale 15000 = ₹5000) does NOT enter investing activities directly — it was already added back to profit in operating activities (since it is a non-cash loss). Only the actual cash inflow ₹15000 from the sale enters investing. Same principle for gain/loss treatment. Investing activities reflect long-term capital deployment — a net negative often indicates capital expansion which is healthy if returns justify it.

Q503 Marks

M/s Pooja Industries has these financing activities for FY 2023-24: Proceeds from issue of equity shares ₹200000; Proceeds from debentures issue ₹100000; Repayment of long-term loan ₹50000; Dividend paid ₹40000; Interest paid ₹15000.

Issue of shares is shown under:

AOperating

BInvesting

CFinancing

DAll

Dividend paid is treated as:

AOutflow

BInflow

CBoth

DNo effect

Compute cash from financing activities and explain treatment of interest and dividend.

Show answersHide answers

1. Option 3 — Financing

2. Option 1 — Outflow

3. Cash from Financing Activities: Inflows — Proceeds from issue of shares 200000; Proceeds from debentures 100000 = 300000. Outflows — Repayment of long-term loan (50000); Dividend paid (40000); Interest paid (15000) = (105000). NET CASH FROM FINANCING = 300000 − 105000 = ₹195000. Financing activities reflect changes in equity and long-term borrowings: the firm has raised ₹300000 in capital and used ₹105000 for repayments and distributions netting +₹195000 inflow. Note: Interest paid is treated as financing (for non-financial companies) per AS-3 — it represents the cost of borrowing directly related to financing decisions. Dividend paid is always financing — it is a return to shareholders related to the financing of the company.

Q513 Marks

The Cash Flow Statement is a financial report that provides a detailed analysis of what happened to a business's cash during a specific period. It breaks down cash flows into three main categories: operating activities, investing activities, and financing activities. Cash flow from operating activities includes cash generated from the core business operations, while cash flow from investing activities reflects cash used for investments in assets and securities. Financing activities show the cash inflows and outflows related to borrowing and equity financing. The statement is crucial for assessing the liquidity and financial health of a business, as it highlights the cash available for operations and investments. Understanding cash flow is essential for stakeholders to make informed decisions regarding the company's financial performance and sustainability.

Which of the following is NOT a category of cash flow activities?

AOperating Activities

BInvesting Activities

CFinancing Activities

DTax Activities

What is the primary purpose of a Cash Flow Statement?

Cash flow from operating activities primarily includes cash generated from which of the following?

AInvestments

BCore business operations

CBorrowing

DEquity financing

Show answersHide answers

1. Option 4 — Tax Activities

2. To provide a detailed analysis of cash inflows and outflows during a specific period.

3. Option 2 — Core business operations

Table-Based Questions4 questions

Q523 Marks

Three activities classification under Cash Flow Statement (AS-3):

Activity

Description

Examples

Operating

Primary revenue-generating

Cash from sales, payments to suppliers/employees, tax paid

Investing

Acquisition/disposal of long-term assets

Purchase/sale of fixed assets/investments

Financing

Changes in equity and borrowings

Issue of shares/debentures, repayment of loans, dividend paid

Issue of debentures is classified as:

AOperating

BInvesting

CFinancing

DOperating + Financing

Purchase of investments is classified as:

AOperating

BInvesting

CFinancing

DOperating + Investing

Why are cash flows classified into three categories?

Show answersHide answers

1. Option 3 — Financing

2. Option 2 — Investing

3. Cash flows are classified into three categories per AS-3 to provide users with useful information about cash generation and use. Operating activities are the main revenue-generating activities — typically the largest source of cash for a healthy business. Investing activities reflect long-term capital deployment — purchases of fixed assets and investments are outflows; sales are inflows. Financing activities reflect changes in equity and long-term debt — raising capital is an inflow; repayment dividend interest are outflows. Net change in cash = Operating + Investing + Financing. The classification reveals how the firm has generated cash (operations vs financing) and what it has done with it (investments vs distributions).

Q533 Marks

Treatment of common items in Cash Flow Statement (Indirect Method):

Item

Treatment

Where shown

Depreciation

Add back to profit

Operating

Loss on sale of asset

Add back

Operating

Gain on sale of asset

Subtract

Operating

Increase in receivables

Subtract

Operating (working capital)

Increase in payables

Add

Operating (working capital)

Interest paid (non-financial co.)

Outflow

Financing

Dividend paid

Outflow

Financing

Interest received

Inflow

Investing

Loss on sale of asset is treated in indirect method by:

AAdd to profit

BSubtract from profit

CNo effect

DGoes to investing

Interest paid by non-financial company is shown under:

AOperating

BInvesting

CFinancing

DEither

Why is loss on sale of asset added back in operating activities?

Show answersHide answers

1. Option 1 — Add to profit

2. Option 3 — Financing

3. Each item has specific treatment in the Cash Flow Statement. Non-cash items (depreciation amortisation goodwill written off) are added back to profit. Gain/loss on sale of fixed assets is non-operating — added back (loss) or subtracted (gain) from profit and the actual cash inflow goes to investing. Working capital changes: increase in current assets or decrease in current liabilities = subtracted (cash used); opposite = added. Interest received is investing; interest paid by non-financial co. is financing; for financial cos. (banks) interest is operating. Dividend paid is always financing. Following these rules ensures the Operating + Investing + Financing = Net change in cash = Closing − Opening cash.

Q546 Marks

Compute Cash from Operating Activities (Indirect Method) from the data of M/s Sundar Stores.

Item

Amount

Net Profit Before Tax

₹100000

Depreciation

₹20000

Loss on Sale of Asset

₹5000

Increase in Trade Receivables

₹15000

Decrease in Inventories

₹10000

Increase in Trade Payables

₹8000

Income Tax Paid

₹25000

Q556 Marks

Compute Cash from Investing Activities and Financing Activities from the data below.

Item

Amount

Purchase of Fixed Assets

₹120000

Sale of Investments

₹30000

Sale of Fixed Asset

₹15000

Interest received

₹5000

Purchase of Investments

₹40000

Issue of equity shares

₹200000

Issue of debentures

₹100000

Repayment of long-term loan

₹50000

Dividend paid

₹40000

Interest paid

₹15000

Picture-Based Questions3 questions

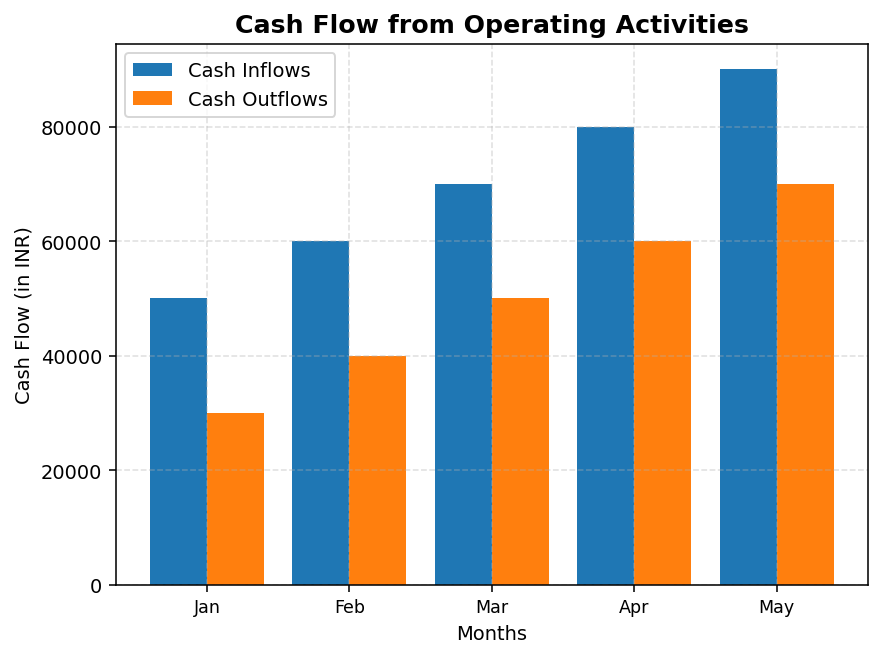

Q562 Marks

Based on the given chart, answer the following:

What is the cash flow from operating activities in March?

AINR 20000

BINR 30000

CINR 40000

DINR 50000

Calculate the total cash inflow for the given months.

Which activity has the highest cash flow in investing activities?

APurchase of Assets

BSale of Assets

CInvestments

DDividends Received

What percentage of cash flow is attributed to 'Sale of Assets'?

Show answersHide answers

1. Option 3 — INR 40000

2. INR 400000

3. Option 1 — Purchase of Assets

4. 30%

Q572 Marks

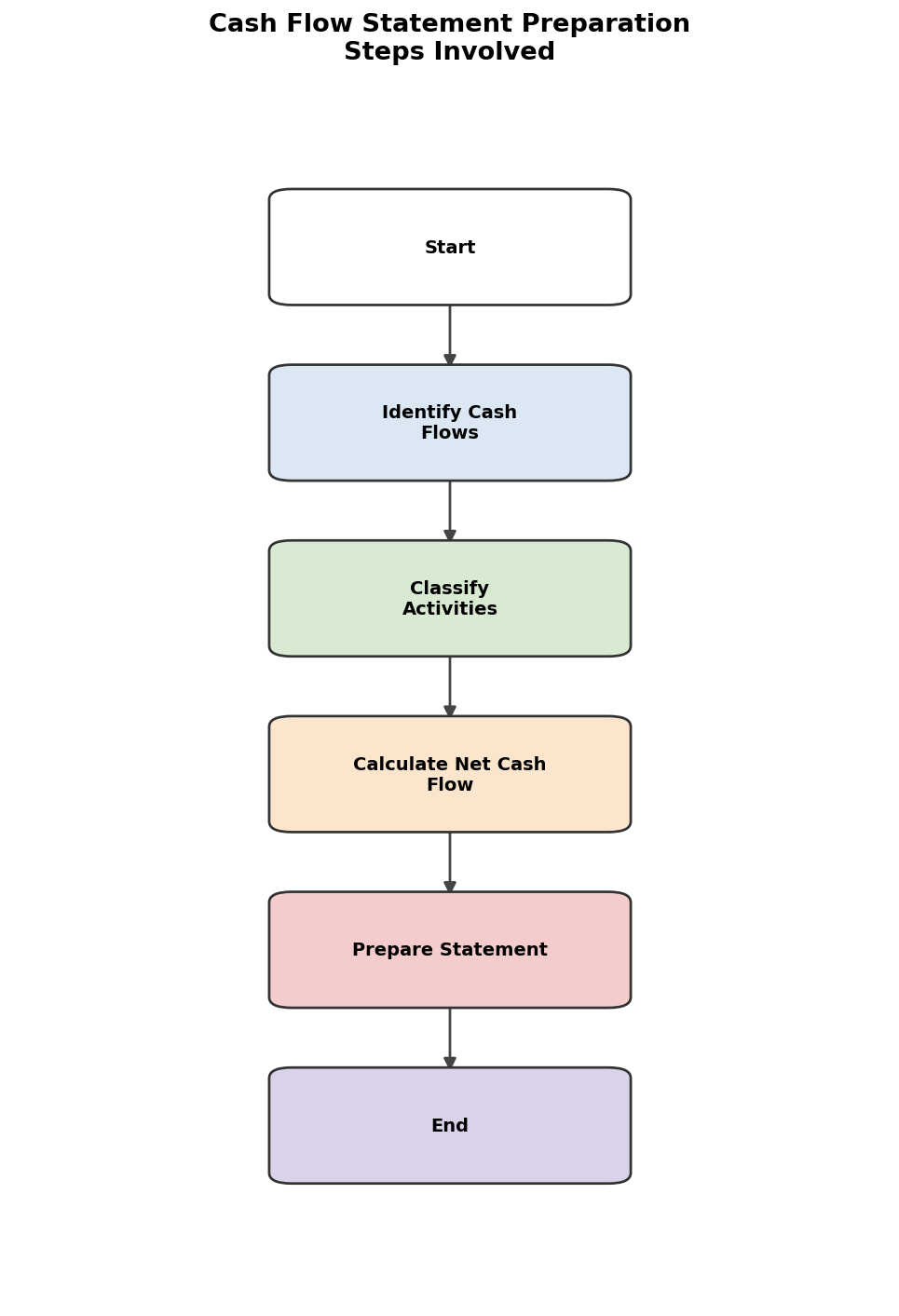

Based on the given flowchart, answer the following:

What is the first step in preparing a cash flow statement?

AIdentify Cash Flows

BClassify Activities

CCalculate Net Cash Flow

DPrepare Statement

What is the final step in the preparation of the cash flow statement?

What are the three classifications of cash flows?

AOperating, Investing, Financing

BRevenue, Expense, Profit

CCurrent, Non-current, Equity

DAssets, Liabilities, Equity

Explain the significance of cash flow from financing activities.

Show answersHide answers

1. Option 1 — Identify Cash Flows

2. End

3. Option 1 — Operating, Investing, Financing

4. It shows the cash inflows and outflows related to borrowing and equity financing.

Q582 Marks

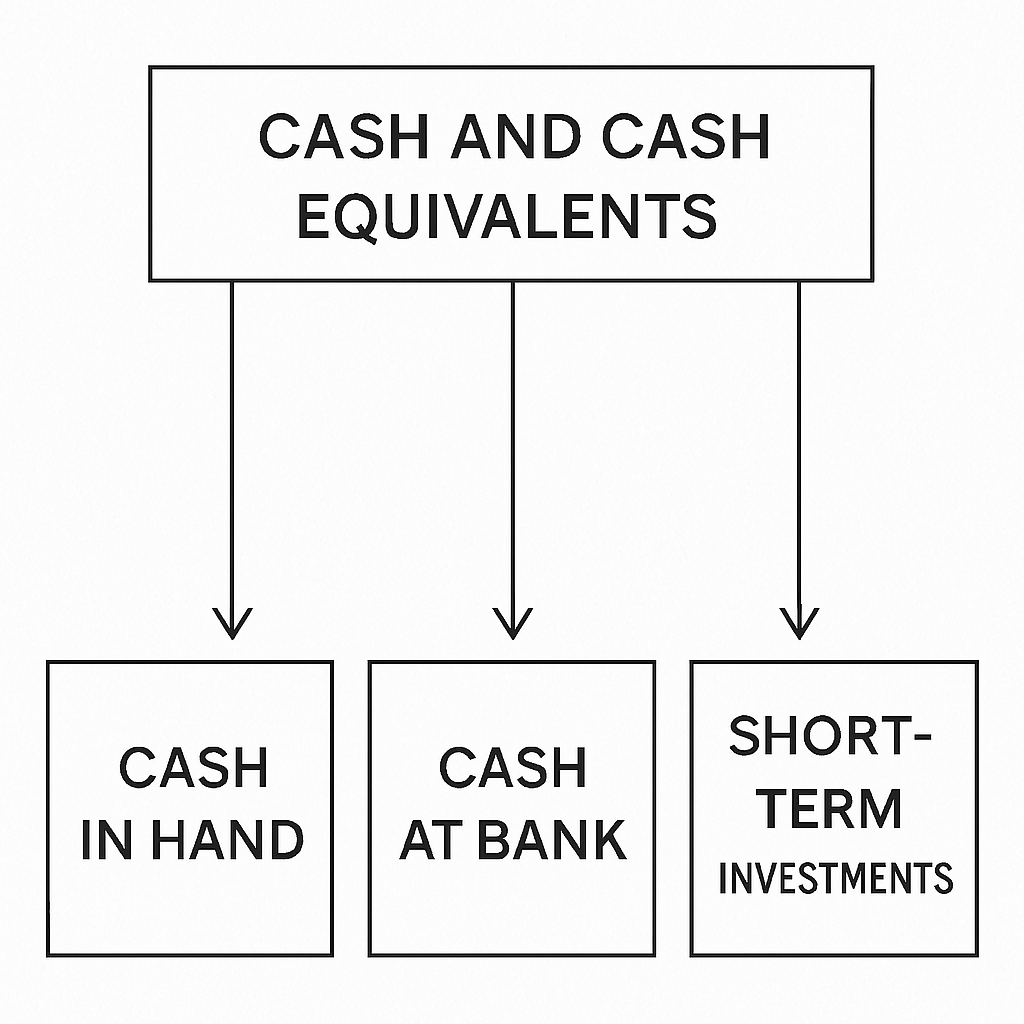

Based on the given diagram of cash and cash equivalents, answer the following:

What does cash in hand represent in the cash flow statement?