Financial Statements of a Company — Important Questions

58 questions

With answersCBSE format

SUMMARY: This chapter focuses on the preparation and presentation of financial statements of a company as per the prescribed format in the Companies Act, 2013. KEY TOPICS: Balance Sheet, Statement of Profit and Loss, Notes to Accounts, Schedule III of Companies Act 2013, Financial Statement Analysis, Share Capital, Reserves and Surplus, Non-current Liabilities, Current Liabilities, Assets.

Schedule III of the Companies Act 2013 prescribes the format for:

AIncome Tax Return

BBalance Sheet and P&L

CGST Returns

DAudit Report

Check answerHide answer

Correct answer: Option 2 — Balance Sheet and P&L

Q21 Mark

The Balance Sheet of a company is prepared in:

AHorizontal form only

BVertical form

CT-form

DBoth horizontal and vertical

Check answerHide answer

Correct answer: Option 2 — Vertical form

Q31 Mark

Provision for tax in the P&L is shown:

ABefore profit before tax

BAfter profit before tax

CAbove sales

DNot shown

Check answerHide answer

Correct answer: Option 2 — After profit before tax

Q41 Mark

Reserves and Surplus is shown under:

AEquity and Liabilities

BAssets

CBoth

DNeither

Check answerHide answer

Correct answer: Option 1 — Equity and Liabilities

Q51 Mark

Notes to accounts are prepared:

AOptional

BMandatory under Companies Act 2013

COnly for foreign companies

DRandom

Check answerHide answer

Correct answer: Option 2 — Mandatory under Companies Act 2013

Q61 Mark

What is the primary purpose of the Statement of Profit and Loss?

ATo show the financial position of a company

BTo summarize revenue and expenses over a period

CTo detail the cash flows of a company

DTo present the company's assets and liabilities

Check answerHide answer

Correct answer: Option 2 — To summarize revenue and expenses over a period

Q71 Mark

Which of the following is classified as a non-current liability?

AAccounts Payable

BBank Overdraft

CLong-term Borrowings

DAccrued Expenses

Check answerHide answer

Correct answer: Option 3 — Long-term Borrowings

Q81 Mark

In which section of the Balance Sheet would you find 'Share Capital'?

AAssets

BEquity

CLiabilities

DExpenses

Check answerHide answer

Correct answer: Option 2 — Equity

Q91 Mark

The total of current liabilities is found in which part of the Balance Sheet?

AEquity and Liabilities

BNon-current Assets

CCurrent Assets

DShareholder's Equity

Check answerHide answer

Correct answer: Option 1 — Equity and Liabilities

Q101 Mark

Which of the following is NOT included in the Notes to Accounts?

AAccounting Policies

BContingent Liabilities

CShareholder's Equity

DRelated Party Transactions

Check answerHide answer

Correct answer: Option 3 — Shareholder's Equity

Q111 Mark

What does 'Reserves and Surplus' represent in the Balance Sheet?

ATotal liabilities of the company

BAccumulated profits not distributed as dividends

CCurrent assets available for use

DInvestments made by shareholders

Check answerHide answer

Correct answer: Option 2 — Accumulated profits not distributed as dividends

Q121 Mark

Which of the following is true regarding the format of financial statements as per Schedule III?

AIt allows for flexibility in presentation

BIt is mandatory for all companies to follow

CIt is optional for listed companies

DIt is only applicable to private companies

Check answerHide answer

Correct answer: Option 2 — It is mandatory for all companies to follow

Q131 Mark

How are 'Current Assets' defined in the context of financial statements?

AAssets that are expected to be converted into cash within one year

BAssets that are held for more than one year

CAssets that are not easily liquidated

DAssets that are used in the production process

Check answerHide answer

Correct answer: Option 1 — Assets that are expected to be converted into cash within one year

Q141 Mark

Which of the following is an example of a current liability?

ABonds Payable

BDeferred Tax Liabilities

CShort-term Loans

DLong-term Debt

Check answerHide answer

Correct answer: Option 3 — Short-term Loans

Q151 Mark

The 'Statement of Profit and Loss' includes which of the following components?

AAssets and Liabilities

BRevenue and Expenses

CCash Flow and Equity

DCurrent and Non-current Assets

Check answerHide answer

Correct answer: Option 2 — Revenue and Expenses

Short Answer Questions10 questions

Q163 Marks

Explain the components of financial statements as per Companies Act 2013.

View sample solutionHide solution

As per Section 129 and Schedule III of Companies Act 2013 the financial statements of a company comprise: (1) Balance Sheet — financial position as at year-end; (2) Statement of P&L — financial performance for the year; (3) Cash Flow Statement — cash inflows and outflows; (4) Statement of Changes in Equity — for Ind AS-compliant entities; (5) Notes to Accounts — disclosures supporting the figures; (6) Auditor's Report — opinion on the truth and fairness of statements; (7) Director's Report — narrative of operations and management commentary. Together they give a comprehensive view of the company's financial health.

Q173 Marks

List the major heads on the Equity and Liabilities side of a company's balance sheet.

View sample solutionHide solution

Per Schedule III: (1) SHAREHOLDERS' FUNDS — Share Capital and Reserves & Surplus; (2) Share Application Money Pending Allotment; (3) NON-CURRENT LIABILITIES — Long-term Borrowings Deferred Tax Liabilities Long-term Provisions Other Long-term Liabilities; (4) CURRENT LIABILITIES — Short-term Borrowings Trade Payables Other Current Liabilities Short-term Provisions. Total Equity and Liabilities equals Total Assets. Each main head has supporting notes giving sub-classifications and details.

Q183 Marks

List the major heads on the Assets side of a company's balance sheet.

View sample solutionHide solution

(1) NON-CURRENT ASSETS — Property Plant and Equipment (PPE) and Intangible Assets; Capital Work-in-Progress; Intangible Assets under development; Investments; Long-term Loans and Advances; Other Non-current Assets. (2) CURRENT ASSETS — Inventories; Trade Receivables; Cash and Cash Equivalents; Short-term Loans and Advances; Other Current Assets. Each is supported by notes. Total Assets = Total Equity and Liabilities maintains the accounting equation.

Q193 Marks

Distinguish between current and non-current assets.

View sample solutionHide solution

Non-current assets: held for use over multiple operating cycles; expected benefit period > 12 months; valued at cost less accumulated depreciation. Examples: land, buildings, plant, machinery, long-term investments, goodwill. Current assets: held for short-term use; expected to be realised in cash within 12 months or one operating cycle whichever is longer. Examples: inventories, trade receivables (debtors), cash, short-term investments, prepaid expenses. The split helps users assess solvency (long-term) vs liquidity (short-term).

Q203 Marks

Explain the format of the Statement of Profit and Loss.

View sample solutionHide solution

As per Schedule III the P&L is presented vertically: I. Revenue from Operations + II. Other Income = Total Revenue. III. Less: Cost of Materials Consumed; Purchases; Changes in Inventories; Employee Benefit Expenses; Finance Costs; Depreciation and Amortisation; Other Expenses = Total Expenses. IV. Profit before Exceptional & Extraordinary Items and Tax (I+II)−III. V. Less: Exceptional Items. VI. Less: Extraordinary Items. VII. Less: Tax. VIII. Profit/(Loss) for the year. IX. Earnings per share (basic and diluted). The format separates operating from non-operating and recurring from non-recurring items for clearer analysis.

Q213 Marks

What is the purpose of the Notes to Accounts in financial statements?

View sample solutionHide solution

The Notes to Accounts provide additional information and explanations regarding the items in the financial statements, enhancing clarity and understanding for users. They include accounting policies, details of significant estimates, and breakdowns of specific line items.

Q223 Marks

Define 'Reserves and Surplus' as it appears in the balance sheet of a company.

View sample solutionHide solution

Reserves and Surplus refer to the portion of profits that are retained in the company rather than distributed as dividends. This includes retained earnings and various reserves created for specific purposes, reflecting the company's financial health.

Q233 Marks

What is Schedule III of the Companies Act 2013?

View sample solutionHide solution

Schedule III of the Companies Act 2013 provides the format for the preparation of financial statements, including the balance sheet and statement of profit and loss, ensuring consistency and transparency in reporting by companies in India.

Q243 Marks

How are 'Share Capital' and 'Reserves and Surplus' different in the context of a balance sheet?

View sample solutionHide solution

Share Capital represents the funds raised by a company through the issuance of shares, while Reserves and Surplus are profits retained in the business after dividends are paid. Share Capital is a liability to shareholders, whereas Reserves and Surplus reflect accumulated profits.

Q253 Marks

What are non-current liabilities, and can you give two examples?

View sample solutionHide solution

Non-current liabilities are obligations that a company expects to settle beyond one year. Examples include long-term loans and bonds payable, which are crucial for understanding a company's long-term financial commitments.

Long Answer Questions6 questions

Q266 Marks

Prepare the balance sheet of M/s Solar Ltd as at 31 March 2024 from the following information using Schedule III format: Equity Share Capital ₹500000; Reserves and Surplus ₹150000; Long-term Borrowings ₹200000; Trade Payables ₹50000; Property Plant and Equipment (net) ₹600000; Inventories ₹100000; Trade Receivables ₹120000; Cash ₹80000.

View sample solutionHide solution

Balance Sheet of M/s Solar Ltd as at 31 March 2024 (Schedule III). I. EQUITY AND LIABILITIES — (1) Shareholders' Funds: Share Capital 500000 + Reserves & Surplus 150000 = 650000; (2) Non-current Liabilities: Long-term Borrowings 200000; (3) Current Liabilities: Trade Payables 50000. Total = ₹900000. II. ASSETS — (1) Non-current Assets: PPE (net) 600000; (2) Current Assets: Inventories 100000 + Trade Receivables 120000 + Cash 80000 = 300000. Total = ₹900000. Both sides equal ₹900000 — balance sheet balances. Notes to accounts would detail share capital break-up, types of reserves, nature of long-term borrowings, etc.

Q276 Marks

Discuss the importance of Notes to Accounts and major disclosures.

View sample solutionHide solution

Notes to Accounts are integral to financial statements. They provide: (1) Significant accounting policies — methods of depreciation, inventory valuation, revenue recognition, foreign currency. (2) Detailed break-up of figures shown only as totals on the face of the statements (e.g., share capital break-up, types of reserves, classes of inventories). (3) Contingent liabilities — pending litigation, guarantees, claims not yet provided for. (4) Commitments — capital expenditure commitments, operating lease commitments. (5) Related party transactions — with directors, key management, subsidiaries. (6) Earnings per share computation. (7) Segment reporting (if applicable). Without notes the financial statements would be unintelligible — they are mandatory under Section 129 of Companies Act 2013.

Q286 Marks

Prepare the Statement of P&L of M/s Lite Ltd for the year ended 31 March 2024: Revenue from Operations ₹800000; Other Income ₹20000; Cost of Materials ₹350000; Employee Benefits ₹150000; Finance Costs ₹30000; Depreciation ₹50000; Other Expenses ₹80000; Tax @25%.

View sample solutionHide solution

Statement of P&L for the year ended 31 March 2024 (Schedule III): I. Revenue from Operations 800000; II. Other Income 20000; Total Revenue 820000. III. Total Expenses: Cost of Materials 350000 + Employee Benefits 150000 + Finance Costs 30000 + Depreciation 50000 + Other Expenses 80000 = 660000. IV. Profit before Tax 820000 − 660000 = 160000. V. Tax @25% × 160000 = 40000. VI. Profit for the year = 160000 − 40000 = ₹120000. EPS (assuming 10000 shares of ₹10 each) = 120000 / 10000 = ₹12. The vertical format clearly separates revenues from expenses and shows profit at each stage.

Q296 Marks

Explain the difference between trial balance and balance sheet.

View sample solutionHide solution

Trial Balance — list of all ledger account balances at a date showing debit and credit columns; checks ARITHMETICAL accuracy; not part of financial statements; preliminary working tool. Includes nominal accounts (revenues and expenses). Balance Sheet — formal statement of FINANCIAL POSITION as at a date; lists assets liabilities and equity; final output of accounting cycle; shared with stakeholders. Excludes nominal accounts (those are in P&L). Trial balance is internal; balance sheet is external. Balance sheet must follow Schedule III format; trial balance has no prescribed format. Both verify the dual aspect (debits = credits in TB; assets = liabilities + equity in BS) but serve different purposes.

Q306 Marks

Discuss the various methods of presentation of financial statements and their requirements.

View sample solutionHide solution

Companies Act 2013 prescribes Schedule III as the format. Two methods: (1) Vertical format — modern, used by all companies; equity & liabilities on top, assets below; subtotals at each level. Better for analysis. (2) Horizontal format — older T-format with assets on right and liabilities/capital on left; rarely used now. Indian companies must use vertical format. Ind AS-compliant entities (large companies) use Statement of Financial Position (Ind AS 1) similar to vertical format with additional disclosures. Other requirements: comparative figures of previous year on the face of every statement; notes referenced from the face; rounding off to nearest thousand or lakh as per company size.

Q316 Marks

What are the key components of a Balance Sheet as per Schedule III of the Companies Act, 2013, and how do they reflect the financial position of a company?

View sample solutionHide solution

The key components of a Balance Sheet as per Schedule III include Assets, Liabilities, and Equity. Assets are divided into non-current and current assets, while liabilities are categorized into non-current and current liabilities. Equity includes share capital and reserves. These components collectively provide a snapshot of a company's financial position at a specific point in time, indicating what the company owns and owes, and the residual interest of the shareholders.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): Schedule III prescribes the format of company balance sheet and P&L.

Reason (R): Schedule III is part of the Companies Act 2013 and ensures uniformity in presentation.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Notes to Accounts are integral to financial statements.

Reason (R): Without notes the financial statements would lack the detail needed to understand the figures.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): Trade payables of less than 12 months are classified as current liabilities.

Reason (R): Current assets and liabilities relate to the operating cycle of the business or 12 months whichever is longer.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Equity Share Capital is part of Shareholders' Funds.

Reason (R): It represents owners' contribution that ranks last in liquidation but earns the residual profits.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): EPS is required to be disclosed on the face of the Statement of P&L.

Reason (R): EPS helps shareholders assess earnings per equity share basic and diluted.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): The Balance Sheet of a company provides information about its financial position at a specific point in time.

Reason (R): The Balance Sheet includes assets, liabilities, and shareholders' equity as per the Companies Act, 2013.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): Reserves and Surplus are shown under the head 'Shareholders' Funds' in the Balance Sheet.

Reason (R): Reserves and Surplus represent retained earnings and other reserves available for distribution to shareholders.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q391 Mark

Assertion (A): Current Liabilities are obligations that a company expects to settle within one year.

Reason (R): Current Liabilities include trade payables, short-term loans, and other liabilities due within the operating cycle.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: Financial statements include Balance Sheet and P&L.

Statement 2: They also include Cash Flow Statement and Notes to Accounts.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: The Balance Sheet has two sides: Equity and Liabilities and Assets.

Statement 2: The two sides must always be equal.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Revenue from Operations is the main source of company income.

Statement 2: Other Income includes interest dividend and gain on sale of investments.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Long-term borrowings appear under Non-current Liabilities.

Statement 2: Short-term borrowings due within 12 months appear under Current Liabilities.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: PPE is classified as a non-current asset.

Statement 2: Inventories trade receivables and cash are current assets.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: The Statement of Profit and Loss includes both revenue and expenses.

Statement 2: Notes to Accounts provide additional information that is not included in the main financial statements.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q461 Mark

Statement 1: Reserves and Surplus are classified under Current Liabilities in the Balance Sheet.

Statement 2: Share Capital represents the funds raised by issuing shares to the public.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: The Balance Sheet is prepared as per Schedule III of the Companies Act, 2013.

Statement 2: Current Liabilities include long-term borrowings.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Case Study / Passage Questions4 questions

Q483 Marks

M/s Solar Ltd has the following balances at 31 March 2024: Equity Share Capital ₹500000; Reserves and Surplus ₹150000; Long-term Borrowings ₹200000; Trade Payables ₹50000; Property Plant and Equipment (net) ₹600000; Inventories ₹100000; Trade Receivables ₹120000; Cash ₹80000.

Schedule III prescribes which format for the balance sheet?

AVertical

BHorizontal

CT-form

DRandom

Total Shareholders' Funds is:

A₹650000

B₹500000

C₹150000

D₹900000

Prepare the balance sheet in Schedule III format.

Show answersHide answers

1. Option 1 — Vertical

2. Option 1 — ₹650000

3. Schedule III (Companies Act 2013) prescribes the vertical format. Balance Sheet of M/s Solar Ltd as at 31 March 2024: I. EQUITY AND LIABILITIES — (1) Shareholders' Funds: Share Capital 500000 + Reserves & Surplus 150000 = ₹650000. (2) Non-current Liabilities: Long-term Borrowings 200000. (3) Current Liabilities: Trade Payables 50000. Total Equity & Liabilities = ₹900000. II. ASSETS — (1) Non-current Assets: PPE 600000. (2) Current Assets: Inventories 100000 + Trade Receivables 120000 + Cash 80000 = 300000. Total Assets = ₹900000. Both sides match — balance sheet balances. Notes to Accounts would detail the share capital break-up types of reserves and nature of long-term borrowings.

Q493 Marks

M/s Lite Ltd has the following data for the year ended 31 March 2024: Revenue from Operations ₹800000; Other Income ₹20000; Cost of Materials ₹350000; Employee Benefits ₹150000; Finance Costs ₹30000; Depreciation ₹50000; Other Expenses ₹80000; Tax @25%.

The first line item in the Statement of P&L is:

ATotal Revenue

BProfit before Tax

CTax

DProfit for the year

Profit for the year is:

A₹160000

B₹120000

C₹40000

D₹820000

Prepare the Statement of P&L for the year.

Show answersHide answers

1. Option 1 — Total Revenue

2. Option 2 — ₹120000

3. Statement of P&L for the year ended 31 March 2024 (Schedule III): I. Revenue from Operations 800000. II. Other Income 20000. Total Revenue (I+II) = 820000. III. Total Expenses: Cost of Materials 350000 + Employee Benefits 150000 + Finance Costs 30000 + Depreciation 50000 + Other Expenses 80000 = 660000. IV. Profit before Tax = 820000 − 660000 = ₹160000. V. Tax @25% × 160000 = ₹40000. VI. Profit for the year = 160000 − 40000 = ₹120000. The vertical format separates revenues from expenses and shows profit at each stage. EPS would be disclosed below if share information is available.

Q502 Marks

M/s Bharat Ltd publishes its annual report. The MD asks the CFO why so much detail is given in 'Notes to Accounts' which seem to repeat figures already in the financial statements.

Notes to Accounts are:

AJust supplementary

BIntegral part of financial statements

COptional disclosures

DInternal documents

Explain why Notes to Accounts are integral to financial statements.

Show answersHide answers

1. Option 2 — Integral part of financial statements

2. Notes to Accounts are integral to financial statements per Section 129 of Companies Act 2013. They provide: (1) Significant accounting policies — depreciation method inventory valuation revenue recognition foreign currency. (2) Detailed break-up of figures shown only as totals on the face of the statements (share capital break-up types of reserves classes of inventories). (3) Contingent liabilities — pending litigation guarantees claims not yet provided for. (4) Commitments — capital expenditure commitments operating lease commitments. (5) Related party transactions — with directors key management subsidiaries. (6) Earnings per share computation. (7) Segment reporting (if applicable). Without notes the financial statements would be unintelligible — they explain the figures and reveal the context. They are MANDATORY under Section 129.

Q514 Marks

The financial statements of a company are crucial for providing a clear picture of its financial health. According to the Companies Act, 2013, these statements typically include the Balance Sheet, Statement of Profit and Loss, and Notes to Accounts. The Balance Sheet presents a snapshot of the company's assets, liabilities, and equity at a specific point in time, while the Statement of Profit and Loss summarizes the company's revenues and expenses over a period, showing the net profit or loss. The Notes to Accounts provide additional details and explanations regarding the figures presented in the financial statements, enhancing transparency and aiding stakeholders in making informed decisions.

What are the main components of a company's financial statements as per the Companies Act, 2013?

Which financial statement provides a snapshot of a company's financial position at a specific point in time?

AStatement of Profit and Loss

BBalance Sheet

CCash Flow Statement

DIncome Statement

Why are the Notes to Accounts important in financial statements?

What does the Statement of Profit and Loss summarize?

AAssets and Liabilities

BRevenues and Expenses

CShareholder Equity

DCash Flows

Show answersHide answers

1. Balance Sheet, Statement of Profit and Loss, Notes to Accounts

2. Option 2 — Balance Sheet

3. They provide additional details and explanations regarding the figures presented.

4. Option 2 — Revenues and Expenses

Table-Based Questions4 questions

Q523 Marks

Equity and Liabilities heads on a company's balance sheet (Schedule III):

Head

Sub-head

Examples

Shareholders' Funds

Share Capital + Reserves & Surplus

Equity capital, general reserve, share premium

Share Application Money Pending Allotment

—

Application money in transit

Non-current Liabilities

Long-term Borrowings, Deferred Tax, Long-term Provisions, Other LT Liabilities

Bank loans, debentures, deferred tax

Current Liabilities

Short-term Borrowings, Trade Payables, Other CL, Short-term Provisions

Bank overdraft, creditors, taxes payable

The major heads of Equity and Liabilities side are:

AShareholders' Funds

BNon-current Liabilities

CCurrent Liabilities

DAll of these

Trade payables are classified as Current Liabilities.

AYes

BNo

CSometimes

DOnly with court order

Explain why liabilities are classified into shareholders' funds non-current and current.

Show answersHide answers

1. Option 4 — All of these

2. Option 1 — Yes

3. Schedule III categorises liabilities by nature and timing. Shareholders' Funds represents the owners' stake — share capital plus accumulated reserves. Non-current Liabilities have repayment obligations beyond 12 months — long-term loans debentures bonds and deferred tax. Current Liabilities have repayment within 12 months or one operating cycle — trade payables short-term borrowings other current liabilities and short-term provisions. The classification helps users assess solvency (long-term capital structure) and liquidity (short-term obligations).

Q533 Marks

Assets heads on a company's balance sheet (Schedule III):

Inventories, Trade Receivables, Cash & Cash Equivalents, ST Loans, Other

Stock, debtors, cash, prepaid

Capital Work-in-Progress

—

Building under construction

Intangible Assets under development

—

Software being developed

Land and Building is classified as:

ANon-current

BCurrent

CBoth

DNeither

A building under construction is shown as:

AInventories

BPPE

CCapital WIP

DTrade Receivables

Why are Capital Work-in-Progress and Intangible Assets under Development shown separately?

Show answersHide answers

1. Option 1 — Non-current

2. Option 3 — Capital WIP

3. Schedule III divides assets into non-current and current based on the operating cycle and 12-month criteria. Non-current Assets have benefit period > 12 months: Property Plant and Equipment (tangible long-term physical assets); Intangible Assets (goodwill software patents); Long-term Investments; Long-term Loans and Advances; Other non-current assets. Current Assets have benefit/realisation within 12 months: Inventories; Trade Receivables; Cash and Cash Equivalents; Short-term Loans and Advances; Other Current Assets. Capital Work-in-Progress (CWIP) and Intangible Assets under Development are special categories — assets being constructed/developed but not yet ready for use; shown separately to highlight ongoing investment.

Q546 Marks

Prepare a balance sheet of M/s Solar Ltd as at 31 March 2024 in Schedule III format.

Item

Amount

Equity Share Capital

₹500000

Reserves and Surplus

₹150000

Long-term Borrowings

₹200000

Trade Payables

₹50000

Property Plant and Equipment (net)

₹600000

Inventories

₹100000

Trade Receivables

₹120000

Cash

₹80000

Q556 Marks

Prepare the Statement of P&L of M/s Lite Ltd for the year ended 31 March 2024 in Schedule III format.

Item

Amount

Revenue from Operations

₹800000

Other Income

₹20000

Cost of Materials Consumed

₹350000

Employee Benefits Expense

₹150000

Finance Costs

₹30000

Depreciation

₹50000

Other Expenses

₹80000

Tax rate

25%

Picture-Based Questions3 questions

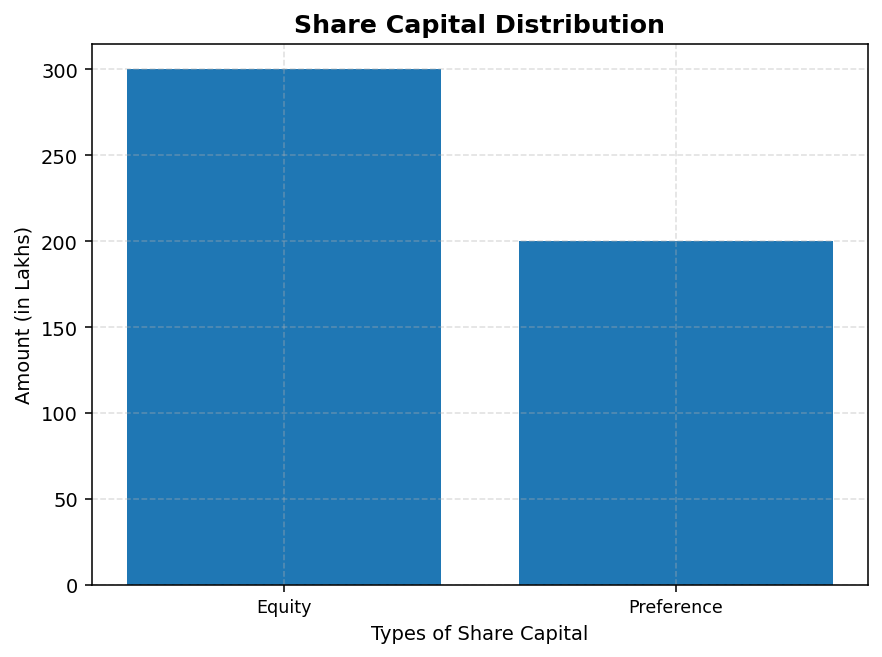

Q563 Marks

Based on the given chart, answer the following:

What is the total amount of share capital represented in the chart?

Which type of share capital has a higher amount?

AEquity Shares

BPreference Shares

CBoth are equal

DNone of the above

What percentage of the total share capital is made up of Equity Shares?

What percentage of the reserves is made up of General Reserve?

A40%

B30%

C20%

D50%

Which reserve has the least proportion in the composition?

AGeneral Reserve

BCapital Reserve

CSurplus

DNone of the above

What is the total percentage represented in the chart?

Show answersHide answers

1. 500 Lakhs

2. Option 1 — Equity Shares

3. 60%

4. Option 1 — 40%

5. Option 3 — Surplus

6. 100%

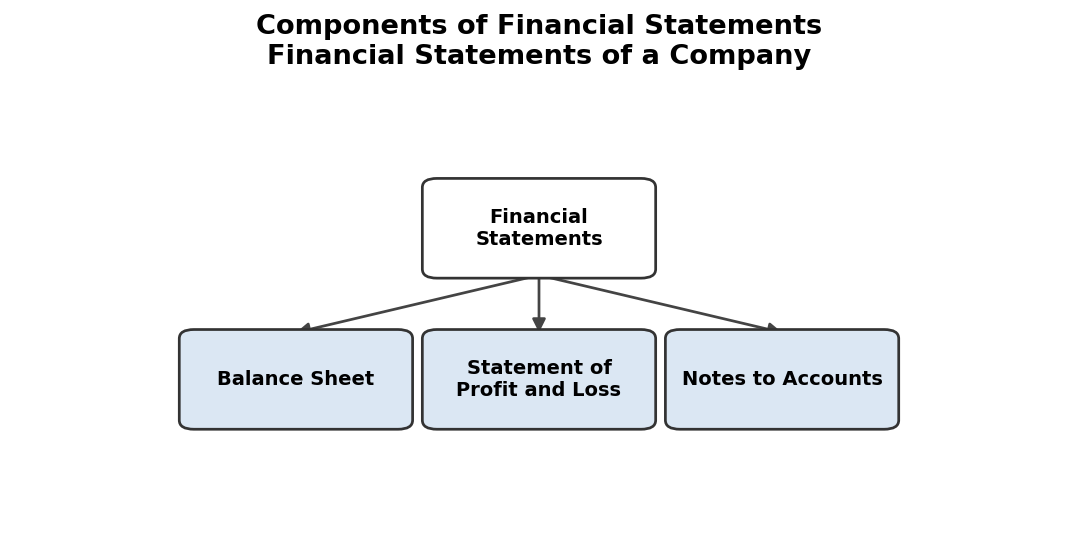

Q573 Marks

Based on the given flowchart, answer the following:

How many main components are identified in the flowchart?

ATwo

BThree

CFour

DFive

What is the primary focus of the flowchart?

Which component is NOT included in the flowchart?

ABalance Sheet

BCash Flow Statement

CStatement of Profit and Loss

DNotes to Accounts

How many types of liabilities are shown in the flowchart?

ATwo

BThree

CFour

DFive

What is an example of Current Liabilities?

Which type of liability is associated with long-term obligations?

ACurrent Liabilities

BNon-current Liabilities

CBoth

DNeither

Show answersHide answers

1. Option 2 — Three

2. Components of Financial Statements

3. Option 2 — Cash Flow Statement

4. Option 3 — Four

5. Short-term Debt

6. Option 2 — Non-current Liabilities

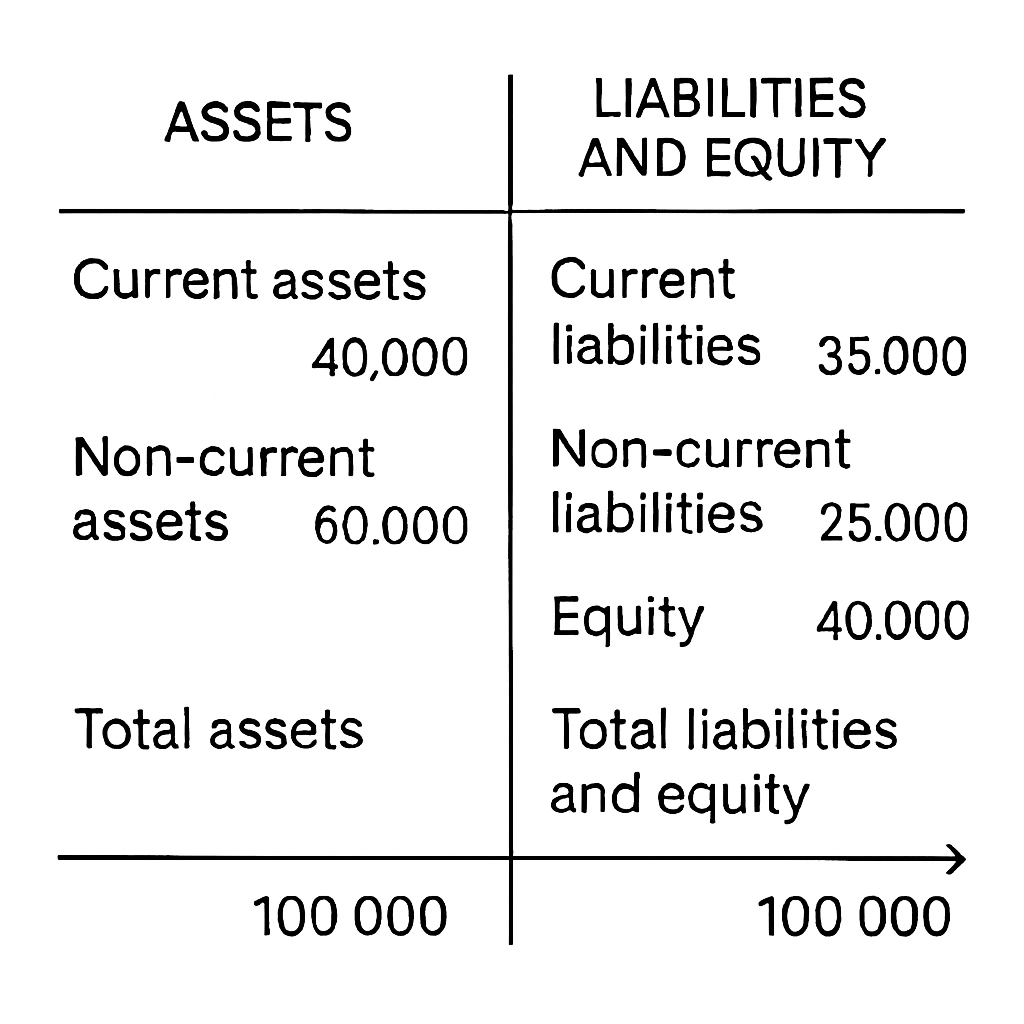

Q583 Marks

Based on the given diagram of the Balance Sheet, answer the following:

What are the two main sections of the Balance Sheet?

AAssets and Liabilities

BIncome and Expenses

CRevenue and Profit

DCash and Bank

What does the Assets section represent?

Which of the following is typically found under Liabilities?