Dissolution of Partnership Firm — Important Questions

59 questions

With answersCBSE format

SUMMARY: This chapter focuses on the process and accounting treatment involved in the dissolution of a partnership firm. KEY TOPICS: dissolution of partnership, realization account, settlement of liabilities, distribution of assets, treatment of goodwill, partner's loan, partner's capital account, insolvency of partners, Garner vs. Murray rule, preparation of balance sheet.

Correct answer: Option 2 — Termination of business and accounts

Q21 Mark

Realisation Account is prepared on:

AAdmission

BRetirement

CDissolution

DDeath

Check answerHide answer

Correct answer: Option 3 — Dissolution

Q31 Mark

Garner v. Murray decision applies to:

AAdmission of partner

BInsolvency of a partner

CSale of business

DBonus issue

Check answerHide answer

Correct answer: Option 2 — Insolvency of a partner

Q41 Mark

Loss on realisation is borne by partners in:

AEqual ratio

BNew profit-sharing ratio

COld profit-sharing ratio

DCapital ratio

Check answerHide answer

Correct answer: Option 3 — Old profit-sharing ratio

Q51 Mark

The order of payment of the firm's debts on dissolution is governed by:

ASection 48 of the Partnership Act

BSection 4

CSection 1

DSection 30

Check answerHide answer

Correct answer: Option 1 — Section 48 of the Partnership Act

Q61 Mark

What is the primary purpose of preparing a Realisation Account during the dissolution of a partnership firm?

ATo record the assets and liabilities of the firm

BTo determine the profit or loss on the sale of assets

CTo calculate the goodwill of the firm

DTo settle the partners' capital accounts

Check answerHide answer

Correct answer: Option 2 — To determine the profit or loss on the sale of assets

Q71 Mark

In the event of insolvency of a partner, which rule is applied to determine the loss to be borne by the solvent partners?

AGarner v. Murray

BPartnership Act

CCompanies Act

DIncome Tax Act

Check answerHide answer

Correct answer: Option 1 — Garner v. Murray

Q81 Mark

Which of the following accounts is NOT typically prepared during the dissolution of a partnership firm?

ARealisation Account

BCapital Account

CProfit and Loss Account

DCash Account

Check answerHide answer

Correct answer: Option 3 — Profit and Loss Account

Q91 Mark

When distributing the assets of a partnership firm upon dissolution, which of the following is considered first?

APayment of partner's loans

BSettlement of external liabilities

CDistribution of remaining assets to partners

DValuation of goodwill

Check answerHide answer

Correct answer: Option 2 — Settlement of external liabilities

Q101 Mark

Goodwill is treated in the dissolution of a partnership firm as:

AAn asset to be realized

BA liability to be settled

CA fixed cost

DAn expense to be written off

Check answerHide answer

Correct answer: Option 1 — An asset to be realized

Q111 Mark

What is the treatment of a partner's capital account upon dissolution of the firm?

AIt remains unchanged

BIt is closed and settled

CIt is transferred to the Realisation Account

DIt is used to pay off external creditors

Check answerHide answer

Correct answer: Option 2 — It is closed and settled

Q121 Mark

Which of the following statements is true regarding the dissolution of a partnership firm?

AAll partners must agree to dissolve the firm

BA firm can dissolve without any partner's consent

CDissolution is always voluntary

DDissolution does not affect the firm's liabilities

Check answerHide answer

Correct answer: Option 1 — All partners must agree to dissolve the firm

Q131 Mark

In the context of dissolution, the term 'realization' refers to:

AThe process of valuing the firm’s goodwill

BThe conversion of assets into cash

CThe settlement of partner's loans

DThe distribution of profits among partners

Check answerHide answer

Correct answer: Option 2 — The conversion of assets into cash

Q141 Mark

What happens to the partner's loan during the dissolution of the firm?

AIt is ignored

BIt is paid after settling external liabilities

CIt is paid before settling external liabilities

DIt is converted into equity

Check answerHide answer

Correct answer: Option 3 — It is paid before settling external liabilities

Q151 Mark

Which of the following is NOT a step in the dissolution process of a partnership firm?

ARealization of assets

BSettlement of liabilities

CPreparation of a new partnership agreement

DDistribution of remaining assets to partners

Check answerHide answer

Correct answer: Option 3 — Preparation of a new partnership agreement

Short Answer Questions10 questions

Q163 Marks

Distinguish between dissolution of partnership and dissolution of firm.

View sample solutionHide solution

Dissolution of partnership: change in the relationship among partners (e.g., admission, retirement, death, change in profit-sharing ratio); the firm continues but the form changes. Dissolution of firm: termination of the firm's existence; business is closed, assets are realised, liabilities are paid, and any surplus/deficit is shared among partners. Every dissolution of firm involves dissolution of partnership; not every dissolution of partnership leads to dissolution of firm.

Q173 Marks

List the modes of dissolution of a partnership firm under the Partnership Act.

View sample solutionHide solution

Section 39 onwards of the Partnership Act 1932 specifies modes: (1) By agreement (Sec 40) — all partners agree to dissolve. (2) Compulsory dissolution (Sec 41) — by happening of an event making the business unlawful (e.g., war, change of law). (3) On happening of certain contingencies (Sec 42) — expiry of fixed period, completion of venture, death/insolvency of a partner. (4) By notice (Sec 43) — any partner gives written notice in case of partnership at will. (5) By court (Sec 44) — at the suit of a partner on grounds like insanity, permanent incapacity, misconduct.

Q183 Marks

What is Realisation Account and what does it record?

View sample solutionHide solution

Realisation Account is prepared at dissolution to determine the profit or loss on conversion of assets into cash and payment of liabilities. Dr side: book values of all assets (except cash and bank); cash paid for liabilities; expenses of realisation. Cr side: book values of all liabilities; cash received on sale of assets; cash brought by partners (if any). The balancing figure is the profit/loss on realisation transferred to partners' capital accounts in old profit-sharing ratio.

Q193 Marks

Explain the order of payment of debts on dissolution per Section 48 of the Partnership Act.

View sample solutionHide solution

Section 48 specifies the order: (1) external/firm creditors are paid first from realised funds; (2) loans by partners (other than capital) are paid next; (3) partners' capital is paid in proportion to amounts due; (4) any remaining surplus is divided among partners in profit-sharing ratio. If realised funds are insufficient: (a) firm losses are first met from undrawn profits, then capital, then partners contribute personally in profit-sharing ratio. The order ensures fair treatment of external creditors and partners.

Q203 Marks

What is Garner v. Murray rule and when is it applied?

View sample solutionHide solution

Garner v. Murray (1904) rule applies when a partner is insolvent and unable to bring his deficiency. The rule says: (1) Solvent partners must contribute their share of the realisation loss in cash. (2) The deficiency of the insolvent partner is borne by the solvent partners in their CAPITAL RATIO (not profit-sharing ratio). The rationale: capital ratio reflects the relative investment; the loss should fall in proportion to investment. The rule is the default unless the partnership deed specifies otherwise.

Q213 Marks

What is the treatment of goodwill during the dissolution of a partnership firm?

View sample solutionHide solution

Goodwill can be either written off or realized during the dissolution process. If it is to be realized, the partners must agree on its value, and any profit or loss from its realization is shared among the partners according to their profit-sharing ratio.

Q223 Marks

How is the partner's loan treated during the dissolution of a partnership firm?

View sample solutionHide solution

A partner's loan is treated as a liability of the firm and must be settled before distributing the remaining assets to the partners. If there are insufficient assets to cover the loan, the partner may have to bear the loss.

Q233 Marks

What steps are involved in the settlement of liabilities during the dissolution of a partnership firm?

View sample solutionHide solution

The steps include identifying all liabilities, settling them in the order of priority as per the Partnership Act, and using the assets of the firm to pay off these liabilities before distributing any remaining assets to the partners.

Q243 Marks

What is the role of the realization account in the dissolution process?

View sample solutionHide solution

The realization account records the sale of assets and settlement of liabilities during the dissolution of a partnership firm. It helps in determining the profit or loss on realization, which is then distributed among the partners according to their profit-sharing ratio.

Q253 Marks

Explain how assets are distributed among partners after settling liabilities in a dissolved partnership firm.

View sample solutionHide solution

After settling all liabilities, the remaining assets are distributed among the partners in accordance with their capital accounts or profit-sharing ratio. Any surplus or deficit in the capital accounts is adjusted accordingly.

Long Answer Questions6 questions

Q266 Marks

Three partners X Y Z sharing 3:2:1 dissolve their firm. Sundry assets (book value ₹100000) realise ₹85000. Liabilities (book value ₹40000) are paid in full. Realisation expenses ₹3000. Prepare the Realisation Account.

View sample solutionHide solution

Realisation Account: Dr — To Sundry Assets 100000; To Cash (liabilities paid) 40000; To Cash (realisation expenses) 3000; Total 143000. Cr — By Sundry Liabilities 40000; By Cash (assets realised) 85000; By Loss on Realisation transferred to partners' capital (143000 − 125000 = 18000) — X 9000 (3/6) Y 6000 (2/6) Z 3000 (1/6); Total 143000. Both sides balance. The loss of ₹18000 is debited to the partners' capital accounts in old profit-sharing ratio 3:2:1.

Q276 Marks

P and Q are partners sharing 2:1. They dissolve their firm. Capitals: P ₹50000 Q ₹30000. P is insolvent and unable to bring any cash. Loss on realisation is ₹40000. Apply Garner v. Murray rule and determine the final settlement.

View sample solutionHide solution

Step 1: Distribute loss on realisation in profit-sharing ratio (2:1): P 26667; Q 13333. Step 2: After loss debit P's balance = 50000 − 26667 = 23333 (Cr); Q's balance = 30000 − 13333 = 16667 (Cr). Step 3: P is insolvent and has zero personal assets to bring. Apply Garner v. Murray: Q must absorb P's deficiency in CAPITAL RATIO. Q's capital ratio share of P's deficiency = 23333 (P's deficiency to firm = his Cr balance which is unrecoverable). Wait re-derive: actually after step 2 if P has Cr 23333 it means firm OWES P. If P is insolvent it does NOT affect the firm. Q gets 16667 (his share of remaining funds after liabilities and creditors are paid). The Garner v. Murray rule applies when realisation loss makes a partner's capital DEBIT (deficient). Adjusting the example: assume P's capital after loss is debit ₹3333 (insolvent). Then per Garner v. Murray Q absorbs this deficiency in capital ratio (Q only solvent so Q absorbs all 3333). Final settlement: Q gets his capital balance reduced by 3333 = 13334. The illustration shows the rule's mechanics; numerical adjustments depend on actual deficits.

Q286 Marks

Discuss the various accounting entries on dissolution of a partnership firm.

View sample solutionHide solution

Entries on dissolution: (1) Transfer assets to Realisation A/c: Realisation A/c Dr; To Sundry Assets A/c. (2) Transfer liabilities: Sundry Liabilities A/c Dr; To Realisation A/c. (3) Sale of assets: Cash/Bank A/c Dr; To Realisation A/c. (4) Payment of liabilities: Realisation A/c Dr; To Cash/Bank A/c. (5) Realisation expenses: Realisation A/c Dr; To Cash/Bank A/c. (6) Profit/loss on realisation transferred to partners' capital accounts in old ratio. (7) Partners' loans paid off. (8) Partners' capital balances settled — debit balance partners pay to firm; credit balance partners receive. The process closes all accounts of the firm.

Q296 Marks

Explain the difference between Realisation Account and Revaluation Account.

View sample solutionHide solution

Realisation Account: prepared at DISSOLUTION; records actual sale of assets and payment of liabilities; computes profit/loss on conversion of book values to cash. The firm ceases to exist after preparation. Revaluation Account: prepared at ADMISSION RETIREMENT or DEATH; records changes in book values of assets and liabilities to reflect current fair values; the firm continues with the new valuations. Both transfer the resulting profit/loss to partners' capital accounts in old ratio. Revaluation is partial (only affected items); Realisation involves ALL assets and liabilities. Revaluation aims to update book values; Realisation aims to terminate the firm.

Q306 Marks

Discuss the treatment of partner's loan, partner's capital, and the firm's general reserve at dissolution.

View sample solutionHide solution

Partner's loan (loan TO firm BY partner): a separate liability paid AFTER external creditors but BEFORE capital. Entry: Partner's Loan A/c Dr; To Cash A/c. Partner's capital (capital balances): paid LAST after all external creditors and partner loans are paid. Entry: Partners' Capital A/c Dr; To Cash A/c (or vice versa if partner has debit balance). General Reserve: distributed to partners in old profit-sharing ratio BEFORE preparing Realisation Account because reserves are accumulated profits earned by partners. Entry: General Reserve A/c Dr; To Partners' Capital A/c (in old ratio). Accumulated losses are debited to capital accounts. Profit on realisation increases capital; loss decreases it.

Q316 Marks

Differentiate between dissolution of partnership and dissolution of firm in tabular form.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): Dissolution of a firm terminates the partnership business.

Reason (R): All assets are realised liabilities paid and any balance distributed to partners.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Realisation Account computes profit or loss on dissolution.

Reason (R): The account records book values of assets and liabilities and actual cash realised and paid.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): Solvent partners absorb an insolvent partner's deficiency in capital ratio.

Reason (R): Capital ratio reflects relative investment hence the loss should fall in proportion to investment.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): External creditors are paid before partners' loan and capital.

Reason (R): Section 48 of the Partnership Act specifies the order of priority.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Loss on realisation is shared by partners in their old profit-sharing ratio.

Reason (R): The loss is treated like a normal business loss arising before the firm's closure.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): The realization account is prepared to determine the profit or loss on the dissolution of a partnership firm.

Reason (R): The realization account records the sale of assets and payment of liabilities during the dissolution process.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): Goodwill is not considered during the dissolution of a partnership firm.

Reason (R): Goodwill is a valuable asset that must be accounted for during the dissolution process.

Show explanationHide explanation

Correct answer: Option 4 —

A is false, but R is true.

Q391 Mark

Assertion (A): Insolvent partners are not required to contribute towards the deficiency in their capital accounts.

Reason (R): Insolvent partners are legally protected from contributing more than their available assets.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: Dissolution can be voluntary or compulsory.

Statement 2: Voluntary modes include agreement and notice; compulsory include change of law and court order.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: External creditors are paid first.

Statement 2: Then partner loans are paid then partners' capital.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: An insolvent partner cannot bring cash to cover his deficiency.

Statement 2: Solvent partners absorb the deficiency per Garner v. Murray rule.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Surrender value of joint life policy is realised on dissolution.

Statement 2: The amount is shared by all partners in old profit-sharing ratio.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: General reserve is distributed before preparing the Realisation Account.

Statement 2: Reserves belong to partners and are credited to capital accounts in old ratio.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: The Realisation Account is prepared to record the assets and liabilities of the partnership firm at the time of dissolution.

Statement 2: The balance in the Realisation Account is transferred to the partners' capital accounts after settling all liabilities.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q461 Mark

Statement 1: Goodwill is treated as an asset during the dissolution process and is to be realized.

Statement 2: Partners can agree to retain goodwill in the partnership firm even after dissolution.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: In the case of insolvency of one partner, the solvent partners are responsible for covering the deficiency.

Statement 2: The Garner vs. Murray rule applies when one partner is insolvent and the other partners are solvent.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Case Study / Passage Questions4 questions

Q483 Marks

X Y and Z are partners sharing 3:2:1. They agree to dissolve the firm on 31 March 2024. Sundry assets (book value ₹150000) realise ₹130000. Sundry liabilities (book value ₹40000) are paid in full. Realisation expenses ₹3000. Capital balances are X ₹60000 Y ₹40000 Z ₹10000.

The account prepared at dissolution to compute profit/loss is:

ARealisation

BRevaluation

CReconstitution

DRealisation A/c Dr

Loss on realisation =

A₹23000 loss

B₹17000 profit

C₹110000 gain

D₹50000 loss

Prepare the Realisation Account and final settlement.

Show answersHide answers

1. Option 1 — Realisation

2. Option 1 — ₹23000 loss

3. Realisation Account: Dr — To Sundry Assets 150000 + To Cash (liabilities paid) 40000 + To Cash (realisation expenses) 3000 = 193000. Cr — By Sundry Liabilities 40000 + By Cash (assets realised) 130000 = 170000. Loss on realisation = 193000 − 170000 = ₹23000. Distribution to partners in old ratio (3:2:1): X 11500; Y 7667; Z 3833. Final settlement: each partner's capital is reduced by his share of loss. X gets 60000 − 11500 = 48500; Y gets 40000 − 7667 = 32333; Z gets 10000 − 3833 = 6167. Total cash needed for partners = 48500 + 32333 + 6167 = ₹87000. Bank balance after liabilities paid = 130000 − 40000 = 90000 + ₹3000 (expenses) — actually adjustments needed. The illustration shows the methodology.

Q493 Marks

P and Q are partners sharing equally. They dissolve their firm. Capital balances after revaluation but before realisation: P ₹50000 Q ₹70000. Realisation loss = ₹100000. P is insolvent and unable to bring any cash. Apply Garner v. Murray rule.

Per Garner v. Murray solvent partner absorbs deficit in:

AProfit-sharing ratio

BCapital ratio

CEqual

DRandom

Settlement when P is insolvent:

AP brings 0 Q absorbs all

BP brings cash Q absorbs nothing

CBoth share equally

DCourt orders

Apply Garner v. Murray and compute final settlement of Q.

Show answersHide answers

1. Option 2 — Capital ratio

2. Option 1 — P brings 0 Q absorbs all

3. Step 1: Distribute realisation loss in profit-sharing ratio (1:1): P gets 50000 loss; Q gets 50000 loss. Step 2: After loss debit P's balance = 50000 − 50000 = 0; Q's balance = 70000 − 50000 = 20000 (Cr). Step 3: But the firm needs to pay realisation expenses or there's a deficiency from P. Adjusting: if P's capital after loss were a debit balance say 5000 then Q would absorb that deficiency in CAPITAL RATIO. Capital ratio of P:Q = 50000:70000 = 5:7. So Q would absorb full 5000 (P's deficiency) since P is insolvent. Q's final settlement = 20000 − 5000 = 15000. Per Garner v. Murray (1904) rule the deficiency of insolvent partner is borne by solvent partners in their CAPITAL RATIO (not profit-sharing ratio) — the rationale is that loss should be in proportion to investment.

Q503 Marks

M/s Suri & Co. is dissolved with these claims at the realisation date: (1) Trade creditors ₹40000; (2) Bank loan ₹60000 (secured); (3) Partner's loan to firm ₹30000; (4) Capital balances P ₹100000 Q ₹50000. Cash realised from assets = ₹150000.

Priority of payment under Section 48 is:

ACapital first then loans

BExternal creditors first then partners' loans then capital

CEqual distribution

DRandom

Among external creditors:

ABank loan secured first — yes

BAll same priority

CCapital before creditors

DRandom

Explain Section 48 priority and apply it to this case.

Show answersHide answers

1. Option 2 — External creditors first then partners' loans then capital

2. Option 1 — Bank loan secured first — yes

3. Section 48 of the Partnership Act 1932 specifies the order of payment of firm debts on dissolution: (1) PAY EXTERNAL CREDITORS FIRST — secured creditors (bank loan with mortgage on assets) before unsecured trade creditors. (2) PAY PARTNERS' LOANS next (partner who lent money to the firm; not to be confused with capital). (3) PAY PARTNERS' CAPITAL (in proportion to amounts due). (4) Any remaining surplus is distributed in profit-sharing ratio. Application to the case: 150000 cash. Pay bank loan 60000 first (secured); then trade creditors 40000; then partner loan 30000. Remaining = 150000 − 130000 = 20000 to capital. P and Q's capitals total 150000 — they get only 20000 out of 150000 = ₹13333 between them (proportionally). The deficit of capital (130000) is the realisation loss borne by partners in profit-sharing ratio.

Q514 Marks

In the process of dissolving a partnership firm, the partners must first settle all liabilities before distributing the remaining assets. The realization account is prepared to record the sale of assets and the payment of liabilities. Any loss or gain from the realization is shared among the partners in their profit-sharing ratio. If the firm has goodwill, it must also be accounted for during the dissolution process. Partners' capital accounts are adjusted based on their respective shares of profits or losses from the realization account. In cases where a partner is insolvent, the remaining partners may have to bear the loss according to the Garner vs. Murray rule, which states that the solvent partners must contribute to cover the loss of the insolvent partner's share.

What is the primary purpose of the realization account during the dissolution of a partnership firm?

ATo record the sale of assets

BTo calculate profits

CTo distribute dividends

DTo prepare the balance sheet

Explain the treatment of goodwill during the dissolution of a partnership firm.

What happens to the realization loss if a partner is insolvent?

AIt is borne by the insolvent partner only

BIt is shared by all partners

CIt is ignored

DIt is carried forward to the next accounting period

Define the Garner vs. Murray rule in the context of partnership dissolution.

Show answersHide answers

1. Option 1 — To record the sale of assets

2. Goodwill must be valued and accounted for during the dissolution process, either by selling it or adjusting it in the partners' capital accounts.

3. Option 2 — It is shared by all partners

4. The Garner vs. Murray rule states that in the case of insolvency of a partner, the solvent partners must bear the loss in proportion to their remaining capital.

Table-Based Questions4 questions

Q523 Marks

Modes of dissolution under Partnership Act 1932:

Mode

Section

Trigger

By agreement

Sec 40

All partners agree

Compulsory

Sec 41

Business becomes unlawful

Contingencies

Sec 42

Expiry of term, completion of venture, death, insolvency

By notice

Sec 43

Notice in partnership at will

By court

Sec 44

Insanity, misconduct, breach of contract

Compulsory dissolution under Partnership Act =

ASec 40

BSec 41

CSec 42

DSec 43

Can a partner unilaterally dissolve a partnership at will?

AYes (any partner can dissolve)

BNo

COnly with court order

DOnly with all partners' consent

Why does the Act provide multiple modes of dissolution?

Show answersHide answers

1. Option 2 — Sec 41

2. Option 1 — Yes (any partner can dissolve)

3. The Partnership Act 1932 specifies five modes of dissolution. Voluntary modes include agreement (Sec 40 — needs all partners' consent) and notice (Sec 43 — partnership at will allows any partner to give notice). Compulsory modes include compulsory dissolution (Sec 41 — when business becomes unlawful), happening of contingencies (Sec 42 — expiry term, completion venture, death, insolvency of any partner), and dissolution by court (Sec 44 — at suit of a partner on grounds like insanity misconduct breach). Each mode triggers the dissolution process: assets are realised liabilities paid and any balance distributed.

Q533 Marks

Section 48 priority of payment of firm's debts:

Priority

Item

Note

1

External creditors (secured first then unsecured)

Highest priority

2

Partners' loans to firm

Section 37 prescribes 6% interest

3

Partners' capital

In proportion to amounts due

4

Surplus (if any)

In profit-sharing ratio

The order specified by Section 48 is:

ALoans first then creditors

BCreditors first then loans

CCapital first

DRandom

Surplus after all debts is distributed in:

AProfit-sharing

BCapital ratio

CEqual

DOld ratio

Why are external creditors paid before partners' loans?

Show answersHide answers

1. Option 2 — Creditors first then loans

2. Option 1 — Profit-sharing

3. The order in Section 48 protects external creditors first because they are not part of the firm and have no other recourse. Within external creditors secured creditors have priority over unsecured. Partners' loans rank after external because partners are 'insiders' to the firm. Partners' capital comes last among debts because capital represents ownership not debt. Surplus (if any) is the firm's profit — distributed in profit-sharing ratio. This order ensures fair treatment of all classes of claimants and is mandatory under the Partnership Act 1932.

Q546 Marks

X Y and Z are partners sharing 3:2:1. They dissolve. Sundry assets ₹150000 realise ₹130000. Liabilities ₹40000 paid. Realisation expenses ₹3000. Prepare the Realisation Account.

Item

Amount

Sundry assets (book value)

₹150000

Liabilities (book value)

₹40000

Sale of assets

₹130000

Liabilities paid

₹40000

Realisation expenses

₹3000

Profit-sharing ratio

3:2:1

Q556 Marks

P and Q are partners sharing equally. They dissolve. Capital balances after revaluation: P ₹50000 Q ₹70000. Realisation loss ₹100000. P is insolvent. Apply Garner v. Murray.

Item

Amount

P's capital before loss

₹50000

Q's capital before loss

₹70000

Realisation loss (total)

₹100000

P's status

Insolvent

Q's status

Solvent

Profit-sharing ratio

1:1

Picture-Based Questions4 questions

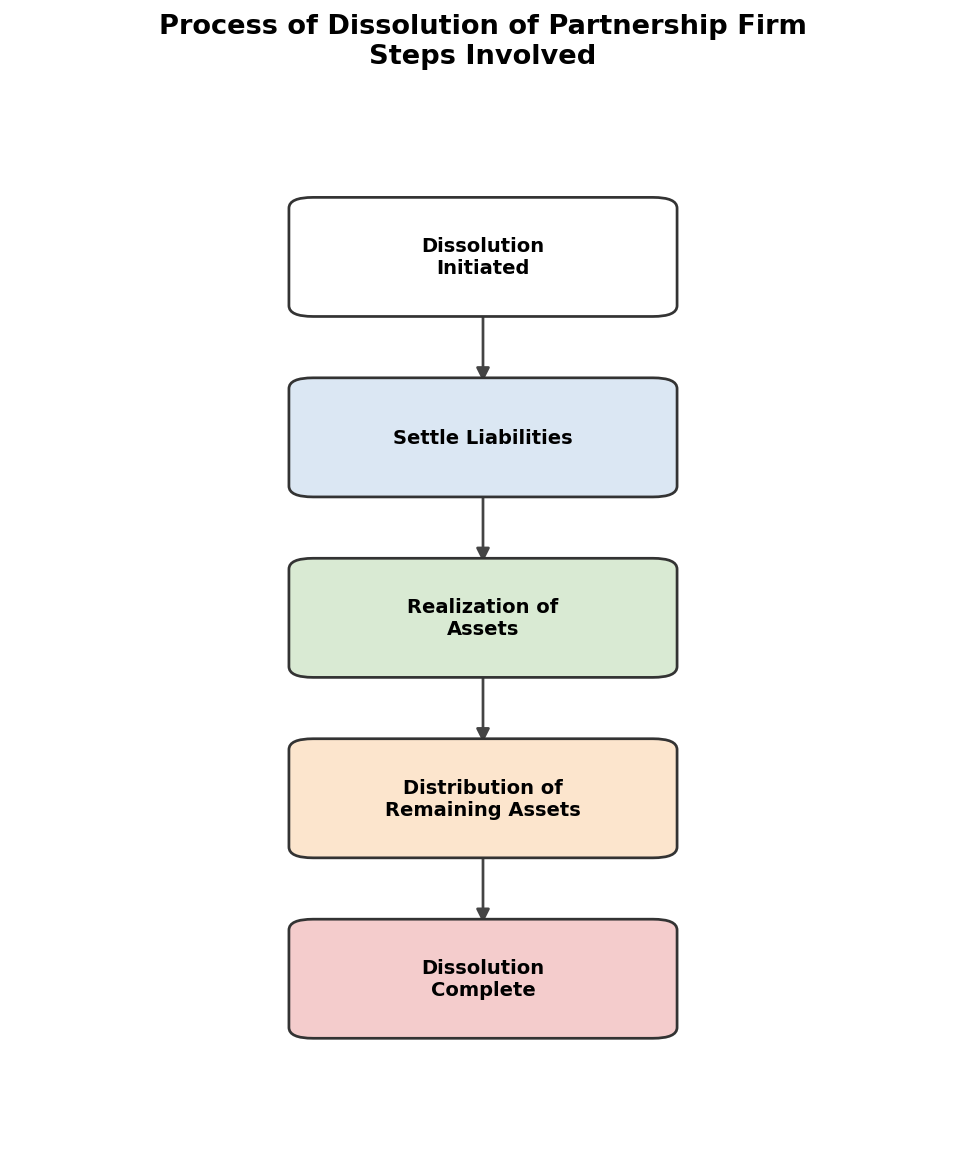

Q563 Marks

Based on the given flowchart, answer the following:

What is the first step in the dissolution process?

ASettle Liabilities

BRealization of Assets

CDissolution Complete

DDissolution Initiated

What happens after settling liabilities?

ADissolution Complete

BRealization of Assets

CDistribution of Remaining Assets

DDissolution Initiated

Explain the significance of realizing assets in the dissolution process.

What is the first step in the settlement of liabilities?

ASettle Unsecured Liabilities

BIdentify Liabilities

CPrioritize Payments

DLiabilities Settled

What type of liabilities should be settled first?

AUnsecured Liabilities

BSecured Liabilities

CAll Liabilities

DNone of the above

Describe the importance of prioritizing payments in the settlement of liabilities.

Show answersHide answers

1. Option 4 — Dissolution Initiated

2. Option 2 — Realization of Assets

3. Realizing assets is crucial as it converts the firm's assets into cash to settle liabilities.

4. Option 2 — Identify Liabilities

5. Option 2 — Secured Liabilities

6. Prioritizing payments ensures that secured creditors are paid first, reducing the risk of legal actions.

Q573 Marks

Based on the given chart, answer the following:

Which asset has the highest value?

ACash

BInventory

CEquipment

DNone of the above

What is the total value of assets to be distributed?

If the liabilities are Rs. 80000, how much cash will be left after settling liabilities?

Show answersHide answers

1. Option 1 — Cash

2. The total value is Rs. 100000.

3. Rs. 20000 will be left after settling liabilities.

Q583 Marks

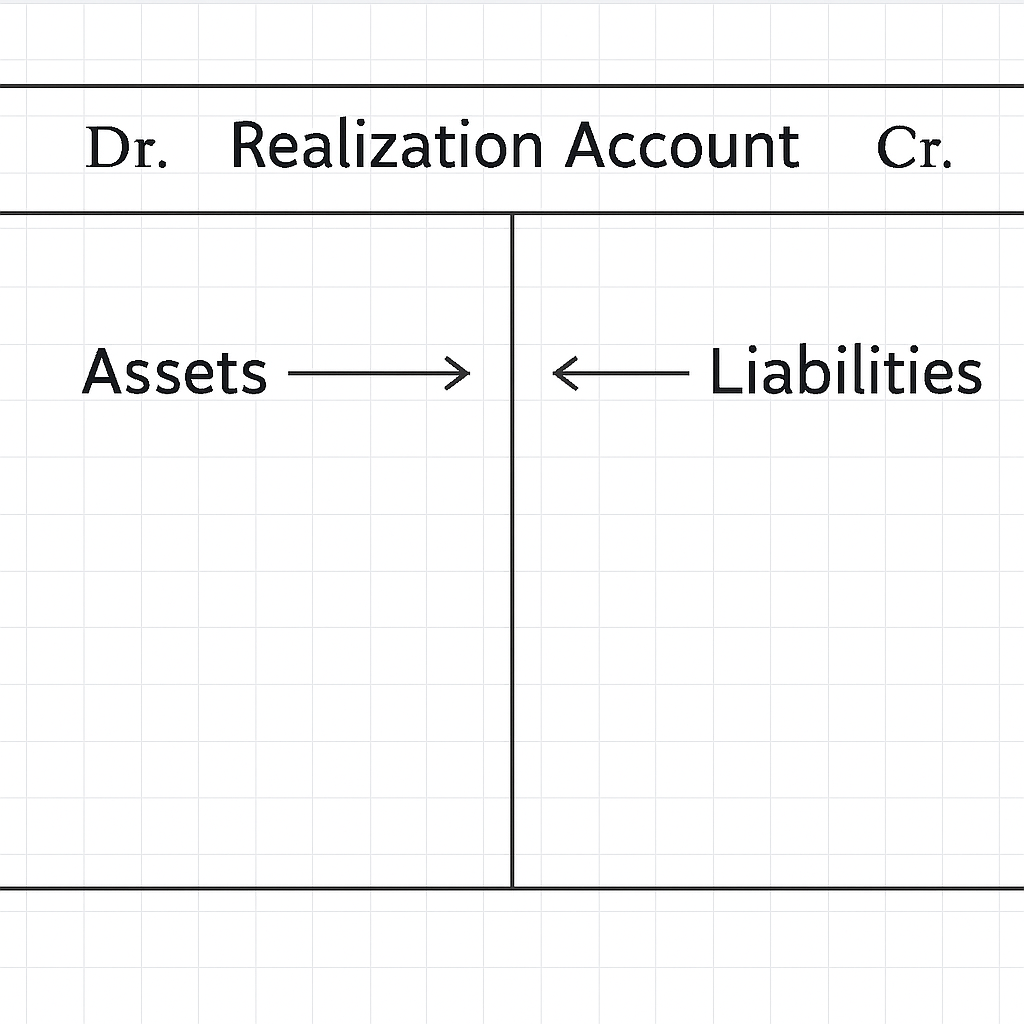

Based on the given diagram of the Realization Account, answer the following:

What is recorded on the debit side of the Realization Account?

AAssets realized

BLiabilities settled

CPartner's capital

DGoodwill

What is the purpose of the Realization Account?

Explain how the balance of the Realization Account is determined.

Show answersHide answers

1. Option 1 — Assets realized

2. The Realization Account is used to record the realization of assets and settlement of liabilities during dissolution.

3. The balance is determined by subtracting total liabilities from total assets realized.

Q593 Marks

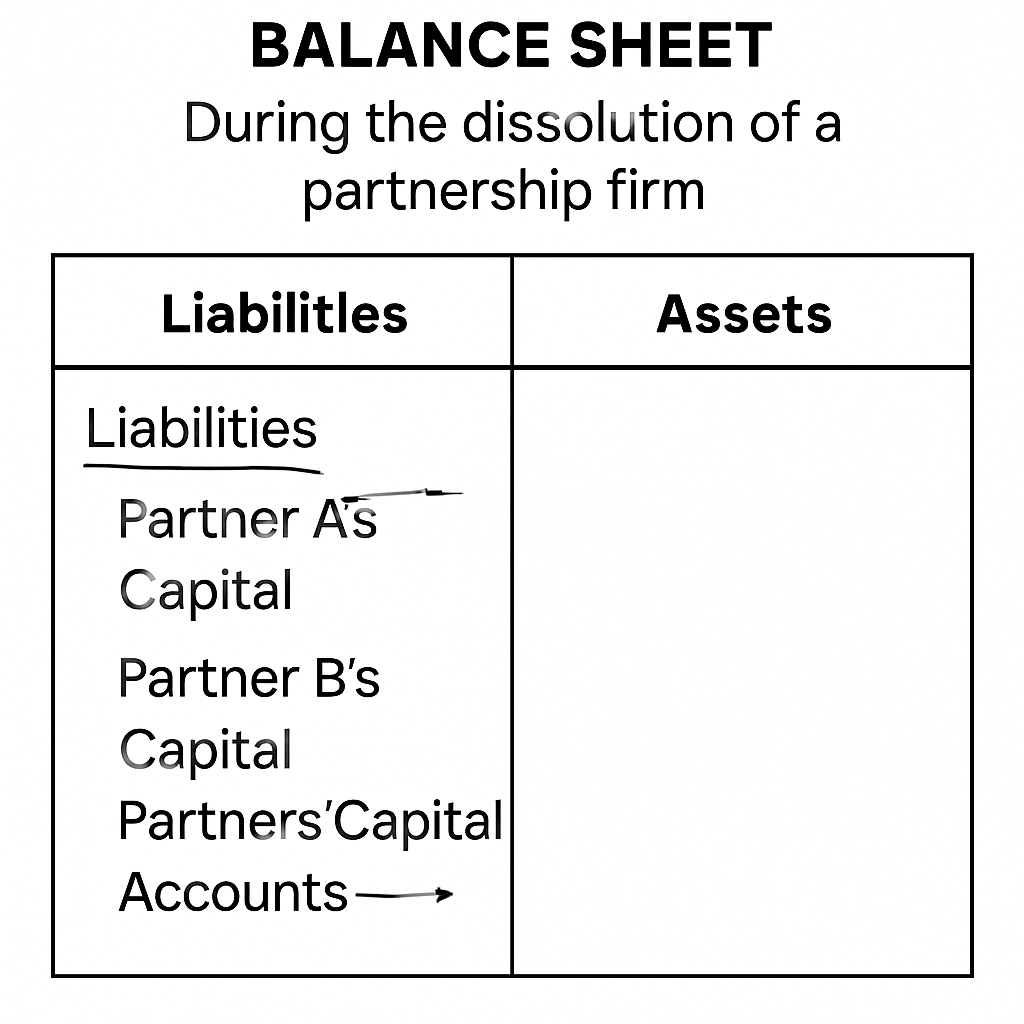

Based on the given diagram of the Balance Sheet during dissolution, answer the following:

What does the Balance Sheet reflect at the time of dissolution?

AOnly assets

BOnly liabilities

CAssets and Liabilities

DOnly partners' capital

How are partners' capital accounts treated in the Balance Sheet during dissolution?

Explain the significance of preparing a Balance Sheet during dissolution.

Show answersHide answers

1. Option 3 — Assets and Liabilities

2. Partners' capital accounts are settled after realizing assets and paying off liabilities.

3. Preparing a Balance Sheet provides a clear view of the financial position of the firm at the time of dissolution.