1. Option 2 — Manufacturing Services

2. Option 3 — Five

3. Life Insurance provides financial protection against the risk of death or disability of a person, whereas General Insurance covers risks related to property, goods, vehicles, health, and other non-life assets.

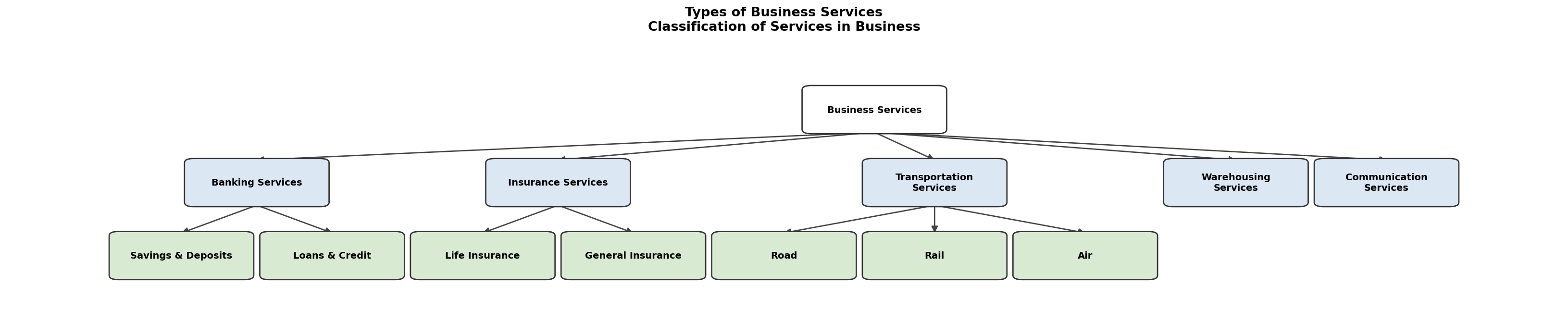

4. Warehousing services are important because they help in storing goods from the time of production until they are needed for consumption or sale, thus bridging the gap between production and consumption and ensuring a steady supply of goods.

5. Option 4 — Inventory (Perishability)

6. Option 2 — Inseparability

7. Inconsistency means that the quality of services varies from one provider to another and even from one occasion to another. For example, the haircut given by the same barber may differ in quality on different days depending on his mood, health, or skill level.

8. Intangibility means services cannot be seen, touched, or felt before purchase, making it difficult for customers to evaluate them beforehand. For example, a customer cannot assess the quality of a legal consultation before actually receiving it, which makes it hard to build customer trust and confidence.

9. Option 3 — Current Account

10. Option 3 — Mobile Banking

11. Overdraft is a facility provided to current account holders to withdraw more than the balance in their account up to a certain limit, usually for a short period. Cash Credit is a short-term loan facility where a borrower can withdraw money up to a sanctioned limit against security of stock or assets, and interest is charged only on the amount actually withdrawn.

12. 1. Collection of Cheques and Bills: Banks collect cheques, bills of exchange, and other negotiable instruments on behalf of their customers and credit the proceeds to their accounts. 2. Payment of Insurance Premium: Banks make payments of insurance premiums, utility bills, and other dues on behalf of their customers as per standing instructions, making financial management convenient.

13. Option 3 — Principle of Insurable Interest

14. Option 4 — Marine Insurance

15. The Principle of Indemnity states that insurance is meant to compensate the insured for the actual financial loss suffered, and not to allow the insured to make a profit from the insurance claim. The insured can only claim the amount of actual loss, not more. It does not apply to Life Insurance because human life cannot be valued in monetary terms — the loss of life or disability cannot be precisely measured financially, so the insured receives the full sum assured regardless of the actual financial loss.

16. Term Insurance provides pure life cover for a specific period. If the insured dies during the term, the nominee receives the sum assured. If the insured survives the term, no maturity benefit is paid. It is the most affordable form of life insurance. Endowment Policy combines life insurance with savings. It provides the sum assured either on the death of the insured during the policy term or on survival till the end of the policy term (maturity). It offers both protection and a savings component, making it more expensive than term insurance.

17. Option 3 — 5

18. Option 3 — Water

19. Life Insurance covers the risk of death or disability of a person and provides financial protection to the insured's family. General Insurance covers risks related to property, goods, vehicles, health, etc., and does not involve human life.

20. Warehousing creates time utility by storing goods from the time of production until they are needed for consumption. It helps businesses maintain a steady supply of goods, protects them from seasonal price fluctuations, and ensures availability of goods throughout the year.

21. Option 3 — Inseparability

22. Option 2 — Services cannot be seen, touched, or felt before purchase

23. Inconsistency means that the quality of services is not uniform and varies depending on the service provider, time, and circumstances. For example, the quality of medical treatment provided by two different doctors for the same illness may differ significantly.

24. Since services cannot be stored, any unused service capacity is lost forever, leading to revenue loss. For example, an empty airline seat on a flight cannot be stored and sold later — once the flight departs, that revenue opportunity is permanently lost. This forces businesses to carefully manage demand and supply.

25. Option 3 — Current Account

26. Option 4 — Internet Banking

27. Overdraft is a facility given to current account holders to withdraw more than the balance in their account up to a specified limit. Cash Credit is a short-term loan facility where the borrower can withdraw money up to a sanctioned limit against security of stock or assets. Interest is charged only on the amount actually withdrawn in both cases.

28. 1. Convenience: E-Banking services like Internet Banking and Mobile Banking allow customers to perform transactions 24x7 from anywhere without visiting the bank branch. 2. Time-saving: ATMs and online platforms enable quick fund transfers, bill payments, and account management, saving significant time for customers and businesses.

29. Option 3 — Road

30. Option 2 — Pipeline

31. 1. Limited Reach: Rail transport is restricted to fixed tracks and cannot reach remote or rural areas, whereas road transport can reach almost any location. 2. Flexibility: Road transport offers door-to-door delivery and greater flexibility in routes and schedules, making it more convenient for businesses, especially for short distances and small consignments.

32. 1. High Cost: Air transport is the most expensive mode of transportation, making it unsuitable for carrying bulk or low-value goods. 2. Limited Capacity: Aircraft have limited cargo space compared to ships or trains, restricting the volume and weight of goods that can be transported at one time.

33. Option 3 — Subrogation

34. Option 3 — Term Insurance

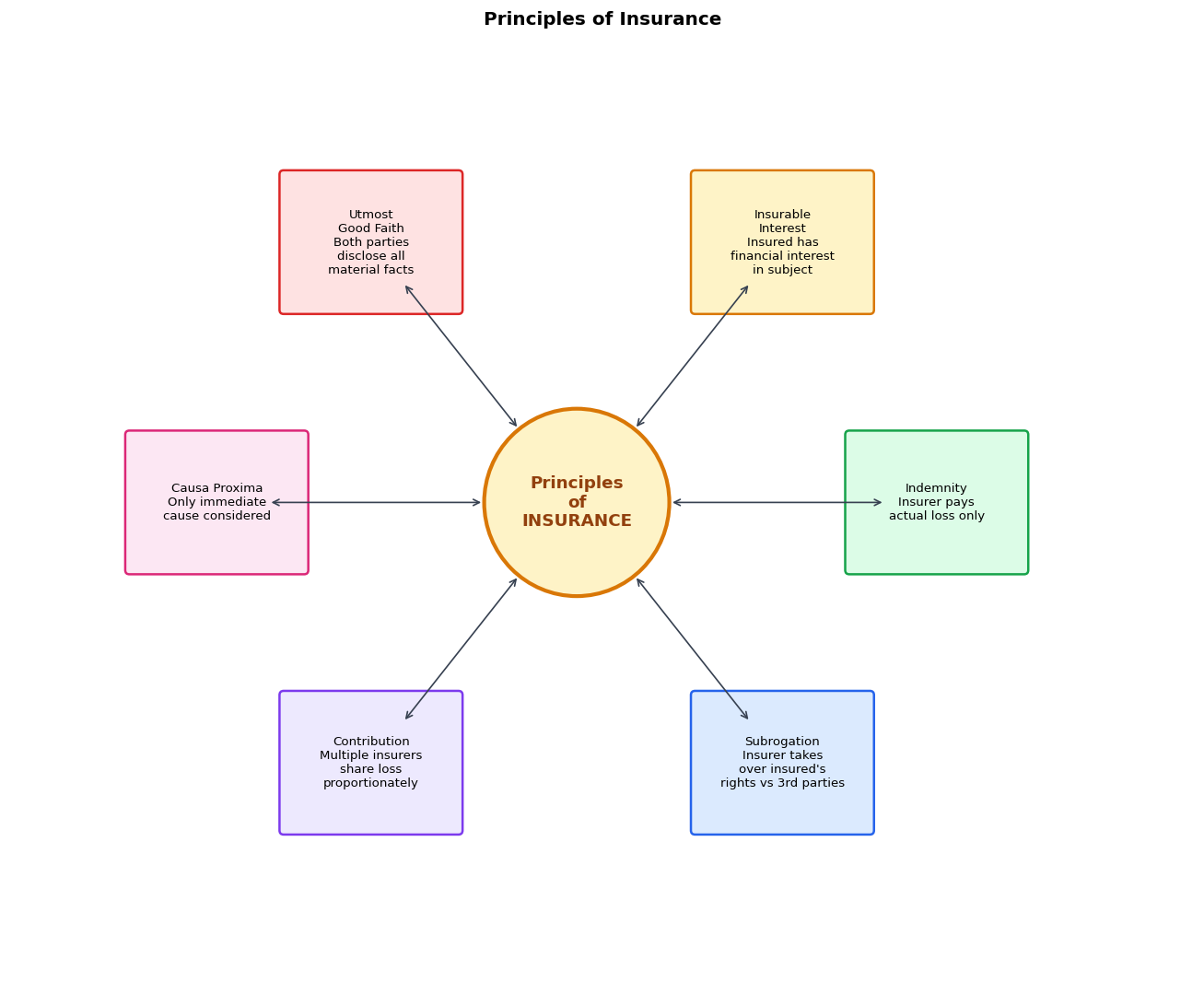

35. The principle of Utmost Good Faith (Uberrimae Fidei) requires both the insurer and the insured to disclose all material facts truthfully and completely at the time of entering into the insurance contract. For example, a person taking a life insurance policy must disclose any pre-existing medical conditions. If the insured conceals material information, the insurer has the right to cancel the policy.

36. The principle of Indemnity states that the insured should be compensated only to the extent of actual loss suffered, not more. However, this principle does not apply to Life Insurance because human life cannot be valued in monetary terms. The loss of life is immeasurable, so the insurer pays the full sum assured as agreed in the policy, regardless of any calculation of actual financial loss. This is why Life Insurance is a contract of assurance, not indemnity.

37. The two sub-types of Insurance Services shown are Life Insurance and General Insurance.

38. Option 4 — Warehousing Services

39. 1. Services are intangible (cannot be touched or seen), whereas goods are tangible. 2. Services are inseparable from the provider, whereas goods can be separated from their producer.

40. Option 3 — Current Account

41. In a Fixed Deposit Account, a lump sum amount is deposited for a fixed period of time and earns a higher rate of interest compared to other accounts.

42. Option 4 — Recurring Deposit Account

43. E-banking (electronic banking) refers to the use of electronic means to conduct banking transactions over the internet. Two services offered: 1. Online fund transfer (NEFT/RTGS) 2. Online bill payment and account management.

44. Option 3 — Utmost Good Faith

45. The principle of Subrogation states that after the insurer compensates the insured for the loss, the rights of the insured over the damaged property are transferred to the insurer. The insurer can then recover the amount from the third party responsible for the loss.

46. Option 2 — Indemnity

47. No, a person cannot insure the life of a stranger. According to the principle of Insurable Interest, the insured must have a financial stake or interest in the subject matter of insurance. A stranger's life does not cause any financial loss to the person, so there is no insurable interest.

48. Option 3 — Rail Transport

49. The two sub-types are: 1. Inland Water Transport and 2. Ocean Transport. Advantage of Ocean Transport: It is the cheapest mode for carrying large volumes of goods across international borders.

50. Option 2 — Petroleum, natural gas, and liquids

51. Air Transport is suitable for perishable and high-value goods because: 1. It is the fastest mode of transport, reducing transit time and preventing spoilage of perishable goods. 2. It provides high security and reliability, making it ideal for valuable or fragile items.

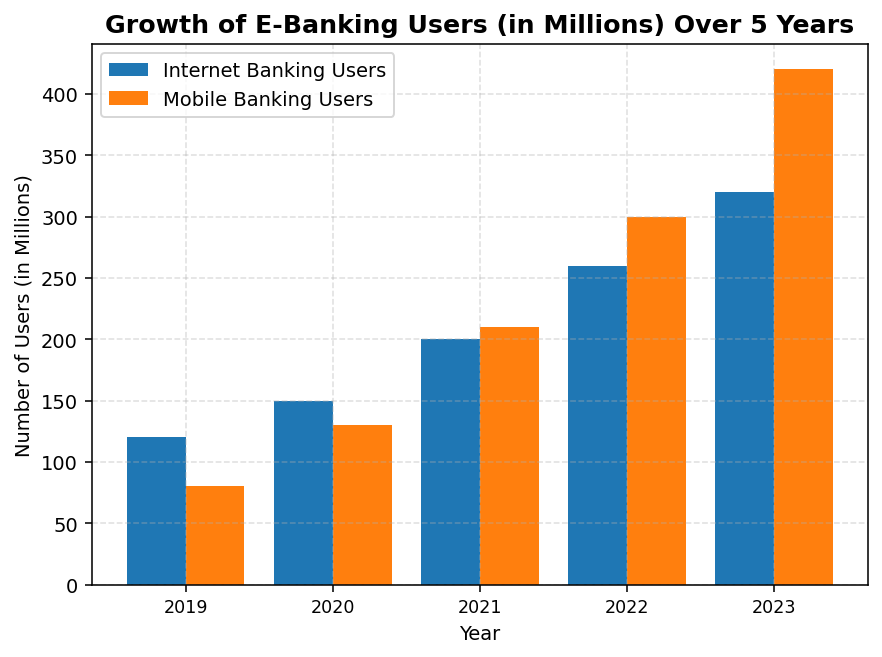

52. Option 3 — 330 million

53. The highest single-year increase was from 2022 to 2023, with an increase of 450 - 350 = 100 million users.

54. Option 3 — Physical presence required for every transaction

55. The steady growth in e-banking users shows increasing adoption of digital banking. Benefits: For businesses — faster payments, reduced transaction costs, easy access to credit and financial services. For customers — convenience of banking from anywhere, 24/7 access, quick fund transfers, and reduced need to visit bank branches.

56. Option 3 — Manufacturing Services

57. The diagram shows Life Insurance and General Insurance as sub-types. Life Insurance covers the risk of death or disability of a person and provides financial security to the family, whereas General Insurance covers risks related to property, goods, vehicles, health, etc., and is typically a short-term contract renewed annually.

58. Option 2 — It provides storage facilities and helps create time utility

59. The two sub-types of Communication Services shown are Postal Services and Telecom Services. Postal Services help in sending letters, parcels, and money orders, facilitating correspondence between businesses and customers. Telecom Services (telephone, internet, mobile) enable instant communication, support e-commerce, and help businesses coordinate operations efficiently across long distances.

60. Option 3 — Balance Enquiry

61. NEFT (National Electronic Funds Transfer) allows transfer of funds in batches at specific time intervals and is suitable for smaller amounts with no minimum limit. RTGS (Real Time Gross Settlement) enables real-time, individual transaction-by-transaction settlement and is used for large-value transactions (minimum ₹2 lakh). RTGS is faster as settlement is immediate, while NEFT operates in hourly batches.

62. Option 3 — Point of Sale (POS)

63. Two advantages of e-banking for businesses are: (1) Convenience and Time-Saving: Through Internet Banking and Mobile Banking (UPI, SMS Banking), businesses can transfer funds, pay bills, and manage accounts 24x7 without visiting a bank branch, saving time and effort. (2) Quick and Secure Fund Transfers: Using EFT services like NEFT and RTGS, businesses can transfer large amounts quickly and securely to suppliers, employees, or partners anywhere in the country, improving cash flow management and reducing the risk associated with handling physical cash.