SUMMARY: The chapter "Theory Base of Accounting" focuses on the fundamental concepts and principles that form the foundation of accounting practices. KEY TOPICS: Generally Accepted Accounting Principles (GAAP), accounting concepts, accounting conventions, accrual basis of accounting, cash basis of accounting, consistency principle, materiality principle, prudence principle, matching principle, full disclosure principle.

The principle that requires the same accounting method to be used over time is:

AGoing concern

BConsistency

CMateriality

DDisclosure

Check answerHide answer

Correct answer: Option 2 — Consistency

Q51 Mark

Under which concept is the business considered separate from its owner?

AMoney measurement

BBusiness entity

CGoing concern

DCost

Check answerHide answer

Correct answer: Option 2 — Business entity

Q61 Mark

What does the accrual basis of accounting recognize?

ATransactions when cash is received

BTransactions when they occur, regardless of cash flow

COnly expenses when paid

DOnly revenues when earned

Check answerHide answer

Correct answer: Option 2 — Transactions when they occur, regardless of cash flow

Q71 Mark

Which principle requires that all information relevant to a company's financial performance be disclosed?

AMateriality Principle

BFull Disclosure Principle

CPrudence Principle

DMatching Principle

Check answerHide answer

Correct answer: Option 2 — Full Disclosure Principle

Q81 Mark

The matching principle is primarily concerned with which of the following?

ARecording revenues only when cash is received

BMatching expenses with revenues in the same period

CRecording all transactions at their historical cost

DRecognizing profits only when they are realized

Check answerHide answer

Correct answer: Option 2 — Matching expenses with revenues in the same period

Q91 Mark

Which accounting concept assumes that a business will continue to operate indefinitely?

AGoing Concern Concept

BConsistency Concept

CAccrual Concept

DEntity Concept

Check answerHide answer

Correct answer: Option 1 — Going Concern Concept

Q101 Mark

What is the purpose of the prudence principle in accounting?

ATo ensure profits are recorded when earned

BTo avoid overstating assets and income

CTo ensure all expenses are recorded immediately

DTo allow flexibility in financial reporting

Check answerHide answer

Correct answer: Option 2 — To avoid overstating assets and income

Q111 Mark

Which of the following is an example of an accounting convention?

AGoing Concern

BMateriality

CConsistency

DAll of the above

Check answerHide answer

Correct answer: Option 4 — All of the above

Q121 Mark

The cash basis of accounting recognizes revenues and expenses when:

AThey are earned

BThey are incurred

CCash is received or paid

DThey are recorded in the books

Check answerHide answer

Correct answer: Option 3 — Cash is received or paid

Q131 Mark

Which principle states that financial statements should not mislead users?

AMateriality Principle

BPrudence Principle

CConsistency Principle

DFull Disclosure Principle

Check answerHide answer

Correct answer: Option 1 — Materiality Principle

Q141 Mark

The consistency principle is important because it:

AEnsures comparability of financial statements over time

BAllows for changes in accounting methods without disclosure

CRequires that all financial transactions be recorded at market value

DEncourages the use of cash basis accounting

Check answerHide answer

Correct answer: Option 1 — Ensures comparability of financial statements over time

Q151 Mark

Which accounting concept emphasizes that expenses should be matched with revenues?

APrudence Principle

BMatching Principle

CMateriality Principle

DAccrual Concept

Check answerHide answer

Correct answer: Option 2 — Matching Principle

Short Answer Questions10 questions

Q163 Marks

Explain the dual aspect concept with one example.

View sample solutionHide solution

Every transaction has two aspects of equal value — a debit and a credit — recorded in the books. Example: when ₹10000 cash is invested by the owner, Cash A/c is debited (asset increase) and Capital A/c is credited (owner's equity increase). The accounting equation Assets = Liabilities + Capital must always balance after each transaction.

Q173 Marks

Explain the going concern assumption.

View sample solutionHide solution

Going concern assumes the business will continue to operate for the foreseeable future and has no intention to liquidate. Hence assets are valued at cost less depreciation (not at liquidation value), and long-term contracts are entered into. If management believes liquidation is imminent, this assumption is dropped and assets are measured at net realisable value.

Q183 Marks

Distinguish between the cash and accrual basis of accounting.

View sample solutionHide solution

Under cash basis, revenue is recognised when cash is received and expenses when cash is paid; simple but does not match revenues with related expenses. Under accrual basis, revenue is recognised when earned and expenses when incurred, regardless of cash flow; provides a true and fair view of profit. Accrual is mandatory under the Companies Act 2013 for companies in India.

Q193 Marks

Define the materiality concept and give an example.

View sample solutionHide solution

Materiality means accounting reports should disclose all items significant enough to influence user decisions, while immaterial items can be aggregated or ignored. Example: a ₹10 stationery purchase need not be itemised on the balance sheet, but a ₹10 lakh equipment purchase must be disclosed separately. Materiality is judged in relation to the size and nature of the enterprise.

Q203 Marks

What is the purpose of accounting standards?

View sample solutionHide solution

Accounting standards are written policy documents issued by recognised bodies (e.g., ICAI in India) that prescribe rules for measurement and disclosure of accounting transactions. Their purposes: (i) ensure uniformity and comparability of financial statements; (ii) reduce subjectivity and bias; (iii) enhance reliability; (iv) provide guidance to accountants; and (v) facilitate audit and regulatory oversight.

Q213 Marks

What are Generally Accepted Accounting Principles (GAAP)?

View sample solutionHide solution

Generally Accepted Accounting Principles (GAAP) are a set of rules and standards that govern financial accounting and reporting in a particular jurisdiction. They ensure consistency, transparency, and comparability of financial statements across different entities.

Q223 Marks

Describe the consistency principle in accounting.

View sample solutionHide solution

The consistency principle states that once an accounting method is adopted, it should be used consistently throughout the financial reporting period. This ensures that financial statements are comparable over time, allowing users to analyze trends and make informed decisions.

Q233 Marks

What is the matching principle in accounting?

View sample solutionHide solution

The matching principle requires that expenses be matched with the revenues they help to generate within the same accounting period. This ensures that a company's financial performance is accurately reflected in its income statement.

Q243 Marks

Explain the prudence principle in accounting.

View sample solutionHide solution

The prudence principle, also known as the conservatism principle, dictates that accountants should anticipate no profits but anticipate all losses. This means that revenues should only be recognized when they are realized, while potential expenses should be recognized as soon as they are foreseeable.

Q253 Marks

What is the full disclosure principle in accounting?

View sample solutionHide solution

The full disclosure principle requires that all relevant financial information be disclosed in the financial statements or accompanying notes. This ensures that users have all necessary information to make informed decisions regarding the financial health of an entity.

Long Answer Questions6 questions

Q266 Marks

Explain any five fundamental accounting concepts: business entity, money measurement, going concern, cost concept, and dual aspect.

View sample solutionHide solution

(1) Business entity — the business is treated as a separate entity distinct from its owner; owner's personal transactions are kept out of the books. (2) Money measurement — only transactions that can be expressed in money are recorded; events like goodwill among employees are excluded. (3) Going concern — the business is assumed to continue indefinitely; assets are valued at historical cost less depreciation. (4) Cost concept — assets are recorded at the price paid to acquire them (historical cost), not at current market value. (5) Dual aspect — every transaction has two aspects (debit and credit) of equal value, leading to the accounting equation Assets = Liabilities + Capital. Together these concepts form the foundation of double-entry book-keeping.

Q276 Marks

Explain the conservatism (prudence) and consistency conventions with examples.

View sample solutionHide solution

Conservatism (prudence) — anticipate no profits but provide for all possible losses; the accountant chooses the option that least overstates assets or income. Examples: (i) closing stock valued at lower of cost or net realisable value; (ii) provision for doubtful debts is created even when actual default has not occurred; (iii) anticipated profit on a long-term contract is not recognised until earned. Consistency — once an accounting policy is chosen, it should be applied consistently from period to period so that the financial statements are comparable. If a change is necessary (e.g., a different depreciation method), the change and its impact must be disclosed in the notes. Together, these conventions reduce manipulation and enhance reliability.

Q286 Marks

Discuss the difference between cash basis and accrual basis of accounting with a numerical example.

View sample solutionHide solution

Cash basis: revenue and expenses are recorded only when cash is received or paid. Accrual basis: revenue is recorded when earned and expenses when incurred, regardless of cash. Example: Ramesh Traders sells goods worth ₹50000 in March 2024 on credit. The customer pays in May 2024. Salary of ₹20000 for March is paid in April. Under cash basis: March 2024 — no revenue from this sale (cash not received), no salary expense (not paid); May — revenue ₹50000 booked. Under accrual basis: March — revenue ₹50000 recognised, salary expense ₹20000 booked, so March profit reflects actual operations. Accrual is mandatory for companies under the Companies Act 2013 because it gives a true and fair view of profitability.

Q296 Marks

Explain the accounting standards (AS) and their objectives. Also state any three accounting standards prescribed by ICAI.

View sample solutionHide solution

Accounting standards are written documents issued by recognised expert bodies that specify how transactions and events should be recorded and reported. In India ICAI issues AS for non-corporate entities and Ind AS (converged with IFRS) for listed and large corporates. Objectives: (i) bring uniformity and comparability across enterprises; (ii) reduce alternative accounting treatments; (iii) enhance reliability of financial statements; (iv) facilitate audit and regulatory compliance. Examples: AS-1 (Disclosure of Accounting Policies), AS-2 (Valuation of Inventories — lower of cost or net realisable value), AS-9 (Revenue Recognition — when significant risks and rewards transfer to buyer), AS-10 (Property Plant and Equipment), AS-26 (Intangible Assets).

Q306 Marks

Explain the meaning of GST and its features.

View sample solutionHide solution

Goods and Services Tax (GST) is a comprehensive indirect tax on the supply of goods and services in India implemented on 1 July 2017 replacing multiple central and state taxes (excise, service tax, VAT, octroi, etc.). Features: (1) Destination-based — tax accrues to the state where the goods/services are consumed. (2) Multi-stage with input tax credit — tax is collected at each stage but credit is given for tax paid on inputs, eliminating cascading. (3) Dual structure — Central GST (CGST) + State GST (SGST) for intra-state supplies; Integrated GST (IGST) for inter-state supplies. (4) Common tax base across states. (5) Compliance through GSTN portal — registration, return filing, invoice matching. (6) Slabs of 0%, 5%, 12%, 18%, and 28%. Benefits include simpler tax structure, reduced compliance burden, and a unified national market.

Q316 Marks

Compare cash discount and trade discount with the help of a table.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): Fixed assets are recorded at cost and depreciated over their useful life.

Reason (R): The going concern assumption holds that the business will continue operations long enough to use up the asset.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Every transaction is recorded in two accounts.

Reason (R): The dual aspect concept says each transaction has a giving and a receiving aspect of equal value.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): Closing stock is valued at the lower of cost or net realisable value.

Reason (R): Conservatism states profits should not be anticipated while losses should be provided for.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Companies in India must follow the accrual basis of accounting.

Reason (R): The Companies Act 2013 mandates accrual-based reporting for all companies.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): An enterprise should not change its method of depreciation every year.

Reason (R): The consistency principle requires the same accounting policy to be followed from period to period.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): The matching principle ensures that expenses are recognized in the same period as the revenues they help to generate.

Reason (R): This principle is crucial for accurately reflecting the profitability of an enterprise during a specific accounting period.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): The materiality principle allows accountants to overlook small errors in financial statements.

Reason (R): This principle states that all significant information must be disclosed in financial statements.

Show explanationHide explanation

Correct answer: Option 3 —

A is true, but R is false.

Q391 Mark

Assertion (A): The consistency principle requires that once an accounting method is adopted, it should be used consistently in future accounting periods.

Reason (R): This principle enhances comparability of financial statements over time.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: The business is treated as separate from its owner.

Statement 2: The owner's drawings are recorded as a deduction from capital not as an expense.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Only transactions measurable in money are recorded.

Statement 2: Qualitative information about employee morale is not recorded in the books.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Assets are recorded at the price paid to acquire them.

Statement 2: Subsequent changes in market value do not change the recorded cost.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Material items must be disclosed separately in the financial statements.

Statement 2: Immaterial items may be aggregated for the sake of conciseness.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: GST is a destination-based indirect tax.

Statement 2: Inter-state supplies attract IGST collected by the central government.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: The accrual basis of accounting recognizes revenues and expenses when they are incurred, regardless of cash transactions.

Statement 2: The cash basis of accounting recognizes revenues and expenses only when cash is received or paid.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q461 Mark

Statement 1: The consistency principle allows businesses to change their accounting methods as frequently as they wish.

Statement 2: The matching principle ensures that expenses are matched to the revenues they help to generate in the same period.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: The full disclosure principle requires that all relevant financial information be disclosed in the financial statements.

Statement 2: The prudence principle suggests that profits should be recorded as soon as they are anticipated.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Case Study / Passage Questions3 questions

Q483 Marks

Mr Khanna runs a textile shop. He has acquired a delivery van for ₹500000 and recorded it at the price he expects to sell it at next year (₹400000). He has also left out a credit purchase of cloth from his books because he has not yet paid for it.

Recording the van at expected sale price violates which concept?

AMoney measurement

BCost concept

CGoing concern

DRealisation

Leaving out the credit purchase violates which concept?

ADual aspect

BMoney measurement

CConservatism

DGoing concern

Explain how Khanna should correct his books with reference to accounting concepts.

Show answersHide answers

1. Option 2 — Cost concept

2. Option 1 — Dual aspect

3. Both errors should be corrected. The van must be recorded at its acquisition cost ₹500000 — the cost concept requires fixed assets to be recorded at the price actually paid, not market or expected value. Subsequent depreciation can be charged but the original cost stays. The credit purchase must be recorded — every transaction has a dual aspect (debit Purchases, credit Creditor) regardless of cash flow. Recording both aspects keeps the accounting equation balanced and ensures reliable books.

Q493 Marks

Sneha is opening an online stationery shop. Her CA explains GST registration is mandatory if her annual turnover exceeds ₹40 lakh (₹20 lakh for special category states). Sneha wonders why GST has replaced the older indirect taxes and how she will collect and pay it.

GST is classified as a:

ADirect tax

BIndirect tax

CWealth tax

DProperty tax

GST is:

AOrigin-based

BDestination-based

CRandom

DEqual in all states

Explain GST and its key features for Sneha's business.

Show answersHide answers

1. Option 2 — Indirect tax

2. Option 2 — Destination-based

3. GST replaced VAT, service tax, excise, and several other taxes from 1 July 2017 to create one unified indirect-tax system. Features: (1) destination-based — tax goes to the state of consumption; (2) multi-stage with input tax credit — tax is collected at each stage but the seller can offset tax paid on inputs against tax collected on outputs, eliminating cascading; (3) dual structure — CGST + SGST for intra-state sales, IGST for inter-state; (4) compliance through the GSTN portal — registration, monthly returns, e-way bills; (5) slabs of 0%, 5%, 12%, 18%, 28%. Benefit: simpler, cheaper compliance and a unified national market.

Q503 Marks

M/s Rohan Traders is incorporated as a Pvt Ltd company. The directors propose to follow cash basis since it is simpler. The CA insists on accrual basis. Rohan is asked to decide.

Under the Companies Act 2013 a company must follow:

ACash basis

BAccrual basis

CEither

DBoth at the same time

To match revenues with the related expenses you must use:

ACash basis

BAccrual basis

CBoth

DSingle entry

Should Rohan Traders follow cash or accrual basis? Explain.

Show answersHide answers

1. Option 2 — Accrual basis

2. Option 2 — Accrual basis

3. Accrual basis is mandatory for companies under the Companies Act 2013 because it gives a true and fair view of profit. Under accrual, revenue is recognised when earned (e.g., when goods are delivered) and expenses when incurred (e.g., salary for the period worked) regardless of cash flow. This matches revenues with the costs incurred to produce them — the matching principle. Cash basis (revenue when cash received, expense when paid) is simpler but distorts profit when there are credit transactions or year-end adjustments. The CA's advice is correct and the directors must follow accrual basis.

Table-Based Questions4 questions

Q513 Marks

Compare key accounting concepts and their applications:

Concept

Statement

Application

Business entity

Business is separate from owner

Owner's drawings deducted from capital

Money measurement

Only money-quantifiable items

Goodwill of brand not recorded

Going concern

Business will continue indefinitely

Assets at cost less depreciation

Cost concept

Assets recorded at acquisition cost

Plant at original price not market

Dual aspect

Every transaction has two aspects

Equal debit and credit

Goodwill of a brand is not recorded due to:

ABusiness entity

BMoney measurement

CGoing concern

DCost

Recording machinery at the price paid (not market) follows:

ACost concept

BGoing concern

CMoney measurement

DConservatism

Why are these concepts called 'fundamental'?

Show answersHide answers

1. Option 2 — Money measurement

2. Option 1 — Cost concept

3. All five fundamental concepts work together. The business entity concept allows separate books of business and owner. Money measurement keeps the books objective. Going concern lets us write off assets over their life. Cost concept anchors valuations to verifiable amounts. Dual aspect ensures the books balance. Together they form the basis of double-entry accounting. Violating any one (e.g., mixing personal and business expenses) compromises the reliability of the financial statements.

Q523 Marks

Study the GST slabs and applicable goods/services:

Slab

Applicable to (examples)

Type

0%

Essentials: milk, eggs, fresh vegetables

Exempt

5%

Coal, sugar, life-saving drugs

Lower

12%

Butter, cheese, mobile phones

Standard

18%

Hair oil, toothpaste, soap

Most goods

28%

Luxury: cars, ACs, tobacco

Highest

Fresh milk attracts which GST rate?

A0%

B5%

C18%

D28%

A luxury car attracts which GST rate?

A5%

B12%

C18%

D28%

Why does GST have multiple rate slabs?

Show answersHide answers

1. Option 1 — 0%

2. Option 4 — 28%

3. GST has multiple slabs to ensure essentials remain affordable while luxury and demerit goods bear higher tax. Slab assignment: 0% for life essentials, 5% for items of mass consumption, 12-18% for most consumer items (the most common slabs), and 28% for luxury items, sin goods (tobacco, alcohol substitutes) and demerit items (often with additional cess). The GST Council periodically reviews slabs to balance revenue and inflation. Compliance is through the GSTN portal — every taxable supply is logged and matched with the buyer's records.

Q536 Marks

Apply each accounting concept to the scenarios in the table and identify the principle being followed (or violated).

Scenario

Concept applied

Owner's drawings deducted from capital

? (Business entity)

Brand goodwill not recorded

? (Money measurement)

Plant at cost less depreciation

? (Going concern + Cost)

Closing stock at lower of cost or NRV

? (Conservatism)

Revenue when earned not when cash received

? (Accrual / Revenue recognition)

Q546 Marks

Compute GST liability for the following intra-state sale: invoice value ₹50000, CGST 9%, SGST 9%. Also compute liability for inter-state sale of ₹50000 at IGST 18%.

Quantity

Intra-state sale

Inter-state sale

Invoice (excl. tax)

₹50000

₹50000

CGST 9%

? ₹4500

—

SGST 9%

? ₹4500

—

IGST 18%

—

? ₹9000

Invoice incl. tax

? ₹59000

? ₹59000

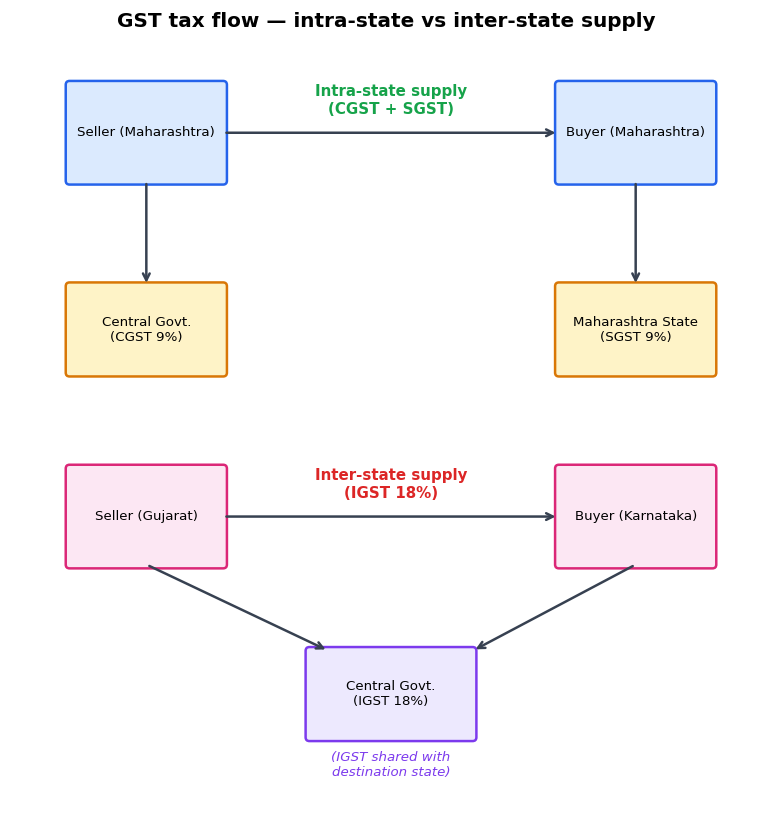

Picture-Based Questions1 question

Q553 Marks

Study the GST tax-flow diagram and answer:

An intra-state supply means:

ATwo states involved

BSame state seller and buyer

CNo GST applicable

DExports

Inter-state supply attracts:

ACGST + SGST

BIGST only

CNo tax

DVAT

Explain CGST, SGST, and IGST and how they apply to intra-state vs inter-state supplies.

Show answersHide answers

1. Option 2 — Same state seller and buyer

2. Option 2 — IGST only

3. GST is a destination-based indirect tax. For an INTRA-state supply (seller and buyer in the same state), the tax is split equally into Central GST (CGST) collected by the central government and State GST (SGST) collected by the state government. For an INTER-state supply (seller and buyer in different states), Integrated GST (IGST) is collected by the central government and later shared with the destination state. The total GST rate is the same in both cases (e.g., 18% = 9%+9% for intra-state, or 18% IGST for inter-state) — only the routing of tax revenue between Centre and States differs. Input tax credit (ITC) makes the GST a value-added tax: tax paid on inputs is offset against tax collected on outputs, so only the value addition at each stage is effectively taxed.