Accounts from Incomplete Records — Important Questions

59 questions

With answersCBSE format

SUMMARY: The chapter "Accounts from Incomplete Records" focuses on understanding how to prepare financial statements when complete accounting records are not available. KEY TOPICS: single entry system, statement of affairs, ascertainment of profit or loss, conversion method, limitations of incomplete records, preparation of trading and profit and loss account, balance sheet preparation, difference between single entry and double entry system, adjustments in incomplete records.

Profit under single entry system can be ascertained by:

ACapital comparison method

BTrial balance method

CP&L method

DAll of these

Check answerHide answer

Correct answer: Option 1 — Capital comparison method

Q31 Mark

Statement of affairs is prepared to find:

ACapital

BProfit

CCash balance

DBank balance

Check answerHide answer

Correct answer: Option 1 — Capital

Q41 Mark

The single entry system is generally used by:

ALimited companies

BSmall traders

CBanks

DGovernment

Check answerHide answer

Correct answer: Option 2 — Small traders

Q51 Mark

Drawings are added to closing capital because:

AThey reduced capital

BThey are an income

CThey are an expense

DThey are a loan

Check answerHide answer

Correct answer: Option 1 — They reduced capital

Q61 Mark

Under the single entry system of book-keeping, which of the following accounts are fully and systematically maintained?

AReal and Nominal Accounts

BPersonal Accounts and Cash Book

CNominal Accounts and Cash Book

DReal and Personal Accounts

Check answerHide answer

Correct answer: Option 2 — Personal Accounts and Cash Book

Q71 Mark

What is the primary conceptual difference between a Balance Sheet and a Statement of Affairs?

AA Balance Sheet shows assets and liabilities, whereas a Statement of Affairs only shows capital.

BA Balance Sheet is prepared from a complete set of double-entry books, whereas a Statement of Affairs is prepared from incomplete records where ledger balances are not fully available.

CA Balance Sheet is prepared only for partnerships, whereas a Statement of Affairs is prepared only for sole proprietorships.

DA Balance Sheet is prepared at the beginning of the financial year, whereas a Statement of Affairs is prepared at the end.

Check answerHide answer

Correct answer: Option 2 — A Balance Sheet is prepared from a complete set of double-entry books, whereas a Statement of Affairs is prepared from incomplete records where ledger balances are not fully available.

Q81 Mark

Given: Opening Debtors ₹40,000; Cash received from Debtors ₹1,20,000; Discount allowed ₹5,000; Bad debts written off ₹3,000; Closing Debtors ₹50,000. What is the amount of Credit Sales for the year?

A₹1,38,000

B₹1,30,000

C₹1,46,000

D₹1,28,000

Check answerHide answer

Correct answer: Option 1 — ₹1,38,000

Q91 Mark

Why is it not possible to prepare a Trial Balance under the single entry system of book-keeping?

ABecause ledger accounts are not balanced at the end of the year.

BBecause both the debit and credit aspects of every transaction are not recorded.

CBecause cash transactions are completely omitted from the books.

DBecause personal accounts are not maintained at all.

Check answerHide answer

Correct answer: Option 2 — Because both the debit and credit aspects of every transaction are not recorded.

Q101 Mark

To find out the opening capital of a business under the Statement of Affairs method, we must prepare a:

AClosing Statement of Affairs

BOpening Balance Sheet

COpening Statement of Affairs

DSummary Cash Book

Check answerHide answer

Correct answer: Option 3 — Opening Statement of Affairs

Q111 Mark

Given: Opening Creditors ₹30,000; Closing Creditors ₹25,000; Cash paid to Creditors ₹85,000; Discount received ₹2,000; Bills Payable accepted during the year ₹10,000. Calculate the credit purchases for the year.

A₹92,000

B₹82,000

C₹1,12,000

D₹90,000

Check answerHide answer

Correct answer: Option 1 — ₹92,000

Q121 Mark

While calculating profit or loss under the Statement of Affairs method, fresh capital introduced during the year is:

AAdded to the closing capital

BDeducted from the closing capital

CIgnored completely

DMultiplied by the rate of interest and added to opening capital

Check answerHide answer

Correct answer: Option 2 — Deducted from the closing capital

Q131 Mark

In the conversion method of incomplete records, if we need to find the 'Total Sales' of the business, we must add:

ACredit sales and credit purchases

BCash sales and cash purchases

CCash sales and credit sales

DCash sales and bills receivable received

Check answerHide answer

Correct answer: Option 3 — Cash sales and credit sales

Q141 Mark

Capital at the end of the year was ₹1,80,000. Drawings during the year were ₹30,000. Fresh capital introduced was ₹20,000. If the profit earned during the year was ₹45,000, what was the opening capital of the business?

A₹1,45,000

B₹1,85,000

C₹1,35,000

D₹1,55,000

Check answerHide answer

Correct answer: Option 1 — ₹1,45,000

Q151 Mark

Which of the following is a major limitation of maintaining incomplete records?

AIt is highly expensive and time-consuming to maintain.

BIt is not acceptable to tax authorities like Income Tax departments.

CIt requires highly skilled and professional accountants to maintain.

DIt is only suitable for large multinational corporations.

Check answerHide answer

Correct answer: Option 2 — It is not acceptable to tax authorities like Income Tax departments.

Short Answer Questions10 questions

Q163 Marks

Define single entry system and state its main features.

View sample solutionHide solution

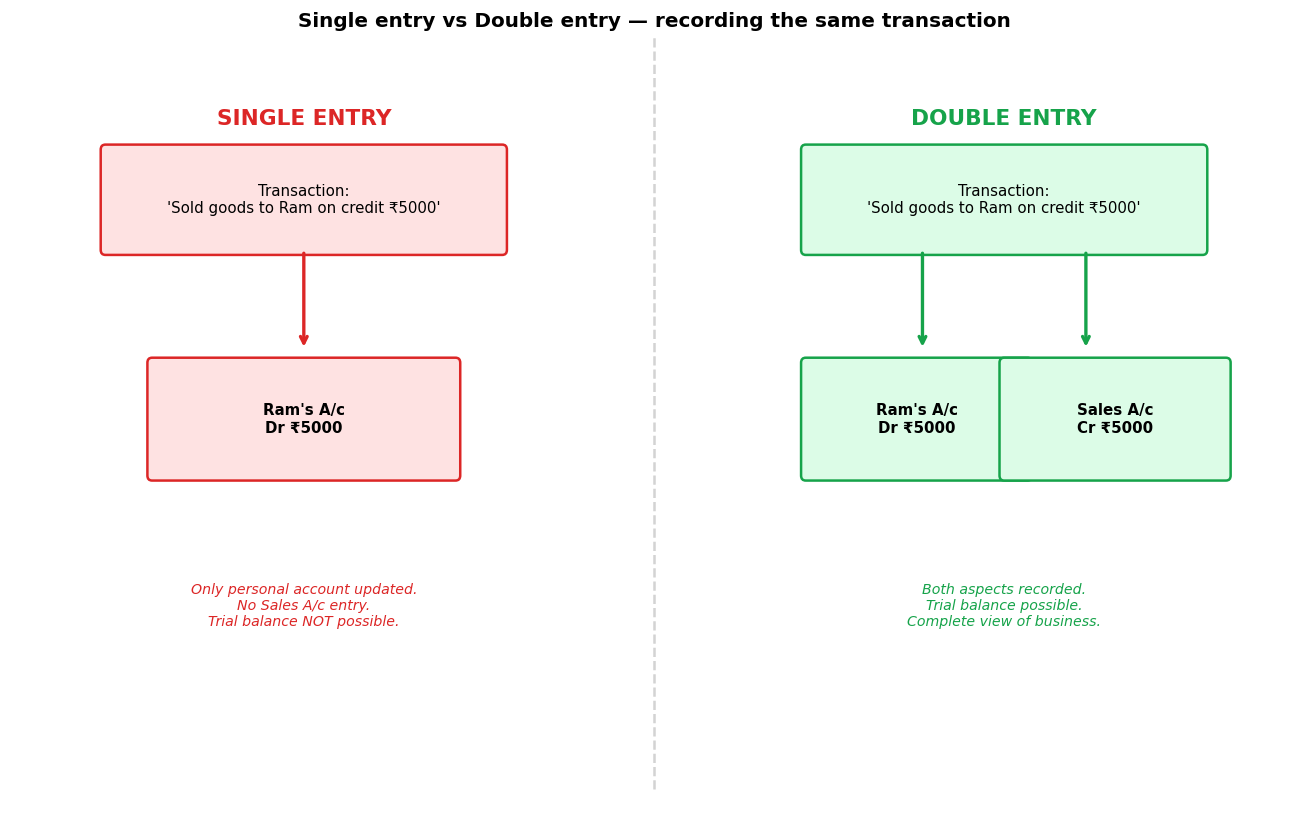

Single entry system is a method of book-keeping where complete double-entry rules are not followed; only personal accounts (debtors and creditors) and cash are usually maintained, with real and nominal accounts often missing. Features: (i) only some transactions are recorded with both aspects; (ii) suitable for small businesses with simple operations; (iii) does not produce a trial balance; (iv) profits estimated through capital comparison rather than P&L Account.

Q173 Marks

Distinguish between single entry system and double entry system.

View sample solutionHide solution

Double entry — every transaction recorded with both debit and credit; complete set of books; trial balance can be prepared; reliable. Single entry — only some transactions with both aspects; mostly personal accounts; no trial balance; less reliable. Double entry follows scientific approach; single entry is incomplete and unscientific. Companies and audited firms must use double entry; small traders may use single entry but it is not recognised by tax authorities.

Q183 Marks

How is profit calculated under the statement of affairs method?

View sample solutionHide solution

Statement of affairs method (capital comparison): Profit = Closing Capital − Opening Capital + Drawings − Additional Capital. Steps: (i) prepare statement of affairs at the start to find opening capital (Assets − Liabilities). (ii) Prepare statement of affairs at the end to find closing capital. (iii) Apply the formula. Example: opening capital ₹50000, closing ₹70000, drawings ₹15000, additional capital ₹10000. Profit = 70000 − 50000 + 15000 − 10000 = ₹25000.

Q193 Marks

List any three limitations of single entry system.

View sample solutionHide solution

(i) Incomplete information — many accounts are missing so true profit and financial position cannot be ascertained. (ii) No arithmetic check — trial balance cannot be prepared, so errors and frauds may go undetected. (iii) Difficult to obtain credit — banks and lenders demand complete records. (iv) Unsuitable for tax purposes — income tax authorities may reject the records. (v) Comparison across periods is unreliable.

Q203 Marks

What is meant by statement of affairs and how does it differ from balance sheet?

View sample solutionHide solution

Statement of affairs is a statement listing assets and liabilities of a business prepared from incomplete records to ascertain capital. Unlike a balance sheet (which is prepared from a tallied trial balance), statement of affairs is based on physical verification, estimates, and partial records. Capital in statement of affairs is the BALANCING figure (Assets − Liabilities = Capital), not derived from the books. It is less reliable and often used only when proper records are unavailable.

Q213 Marks

What is the primary purpose of maintaining incomplete records in accounting?

View sample solutionHide solution

The primary purpose of maintaining incomplete records is to provide a simplified method of recording financial transactions without the need for a full double entry system. This is particularly useful for small businesses that may not have the resources for comprehensive accounting.

Q223 Marks

Explain how the conversion method is used in incomplete records.

View sample solutionHide solution

The conversion method involves converting the incomplete records into a double entry system by estimating the missing figures based on available data. This allows for the preparation of financial statements like profit and loss accounts and balance sheets.

Q233 Marks

What are the key features of a statement of affairs?

View sample solutionHide solution

The key features of a statement of affairs include a summary of assets and liabilities, similar to a balance sheet, but it is prepared when complete records are not available. It serves to show the financial position of the business at a specific point in time.

Q243 Marks

How can one ascertain profit or loss using the statement of affairs method?

View sample solutionHide solution

Profit or loss can be ascertained by comparing the statement of affairs at the beginning and end of the accounting period. The difference in net worth, adjusted for any additional capital introduced or withdrawals made, indicates the profit or loss for the period.

Q253 Marks

What adjustments might be necessary when preparing accounts from incomplete records?

View sample solutionHide solution

Adjustments may include accounting for outstanding expenses, prepaid expenses, accrued income, and any changes in capital introduced or withdrawn during the period. These adjustments ensure that the financial statements reflect the true financial position.

Long Answer Questions6 questions

Q266 Marks

From the following data, ascertain the profit using statement of affairs method: Opening capital ₹120000; Closing capital ₹160000; Drawings ₹20000; Additional capital introduced ₹15000.

View sample solutionHide solution

Profit = Closing Capital − Opening Capital + Drawings − Additional Capital. = 160000 − 120000 + 20000 − 15000 = ₹45000. Logic: closing capital reflects all changes during the year. Drawings reduced capital so they must be added back; additional capital increased capital from external source so deducted. The remaining increase represents profit retained in the business. This is the simplest profit calculation under single entry.

Q276 Marks

From the following statement of affairs of Mr Roy at 1 April 2023 and 31 March 2024, find the profit for the year ending 31 March 2024. Drawings ₹18000 and additional capital ₹12000. Statement of affairs items: (1 Apr 2023) Cash ₹10000, Stock ₹35000, Debtors ₹25000, Furniture ₹20000, Creditors ₹15000. (31 Mar 2024) Cash ₹15000, Stock ₹50000, Debtors ₹35000, Furniture ₹18000, Creditors ₹20000.

View sample solutionHide solution

Opening capital (1 Apr 2023) = Total assets − Liabilities = (10000 + 35000 + 25000 + 20000) − 15000 = 90000 − 15000 = ₹75000. Closing capital (31 Mar 2024) = (15000 + 50000 + 35000 + 18000) − 20000 = 118000 − 20000 = ₹98000. Profit for the year = Closing capital − Opening capital + Drawings − Additional capital = 98000 − 75000 + 18000 − 12000 = ₹29000.

Q286 Marks

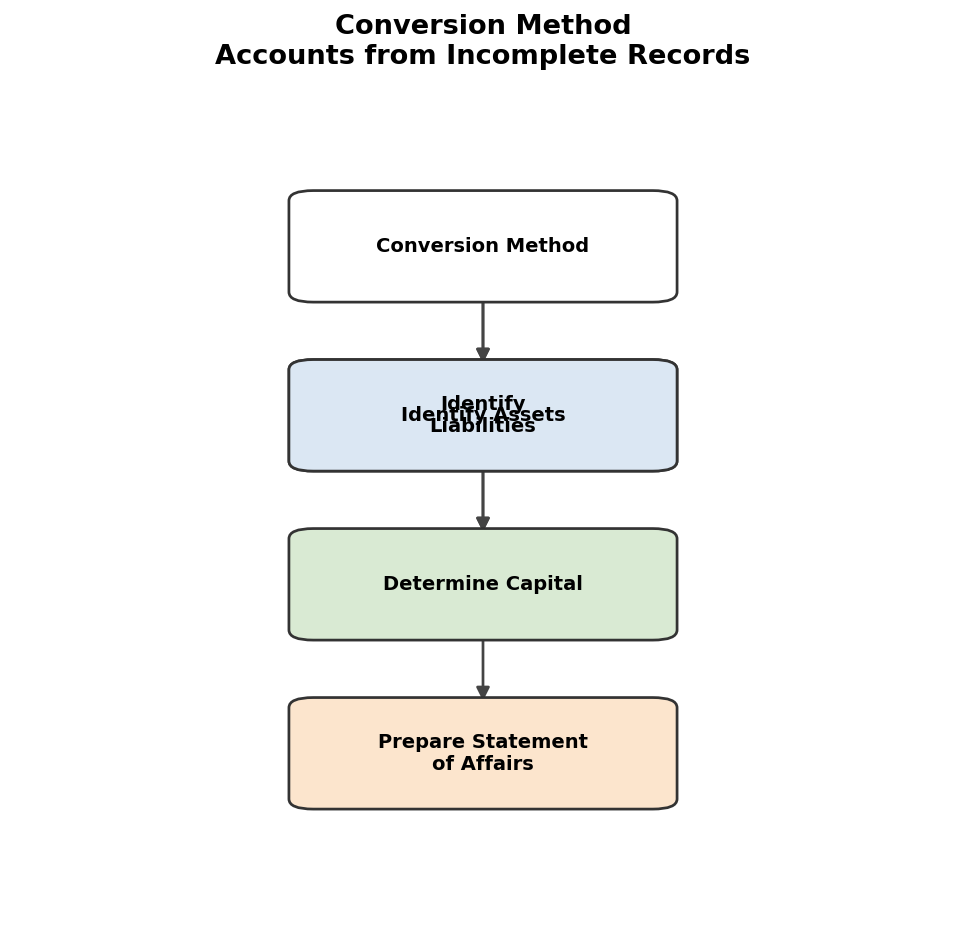

Discuss the conversion method of single entry to double entry.

View sample solutionHide solution

The conversion method involves converting single-entry records into a complete double-entry system to prepare proper financial statements. Steps: (1) Reconstruct missing records by examining bills, vouchers, bank statements, and cash memos. (2) Prepare opening statement of affairs to find opening capital. (3) Compute totals of credit sales (using debtors A/c) and credit purchases (using creditors A/c) by analysing customer and supplier accounts. (4) Aggregate cash receipts and payments from cash records or bank statements. (5) Compile expenses and incomes from vouchers and supporting documents. (6) Prepare adjusted trading account, P&L account, and balance sheet. The conversion method is more accurate than the statement of affairs method and gives a true and fair view, but it is laborious. Auditors typically use this method to audit unrecorded businesses.

Q296 Marks

Compare the merits and demerits of single entry system vs double entry system.

View sample solutionHide solution

Single entry system — Merits: simple, easy to maintain, less time-consuming, suited to small operations. Demerits: incomplete, no arithmetic check, profit calculation unreliable, errors and frauds undetected, not legally recognised for companies. Double entry system — Merits: complete, scientific, allows trial balance preparation, true and fair view, mandatory for companies under Companies Act 2013, accepted by tax and audit authorities, helps detect errors and frauds. Demerits: complex, time-consuming, requires trained staff, higher cost. Conclusion: small unincorporated traders may use single entry for routine business, but for any business of size or seeking external finance/audit, double entry is essential.

Q306 Marks

From the following information of M/s Sushil Stores who maintains accounts on single entry, calculate profit and prepare a statement of affairs as on 31 March 2024: Capital on 1 April 2023 ₹80000; Drawings during the year ₹16000; Additional capital introduced ₹10000; Cash balance on 31 March 2024 ₹12000; Stock ₹40000; Debtors ₹35000; Furniture ₹15000; Creditors ₹25000.

View sample solutionHide solution

Statement of Affairs as on 31 March 2024: Liabilities — Capital (balancing figure) ₹X; Creditors ₹25000. Assets — Cash 12000; Stock 40000; Debtors 35000; Furniture 15000. Total assets = ₹102000. So Capital + 25000 = 102000 ⇒ Closing Capital = ₹77000. Profit = Closing Capital − Opening Capital + Drawings − Additional Capital = 77000 − 80000 + 16000 − 10000 = ₹3000. Statement of Affairs (with capital filled in): Liabilities — Capital ₹77000; Creditors ₹25000; Total ₹102000. Assets — Cash 12000; Stock 40000; Debtors 35000; Furniture 15000; Total ₹102000. Both sides balance.

Q316 Marks

Explain the concept of 'Statement of Affairs' in the context of incomplete records. How does it differ from a traditional balance sheet?

View sample solutionHide solution

The Statement of Affairs is a financial statement used in the single entry system to summarize the assets and liabilities of a business when complete records are not maintained. Unlike a traditional balance sheet, which is prepared under the double entry system and reflects the financial position at a specific point in time, the Statement of Affairs is a snapshot that helps ascertain the net worth of the business by listing all assets and liabilities. It serves as a basis for calculating profit or loss by comparing the opening and closing capital.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): Single entry system does not record both debit and credit aspects of every transaction.

Reason (R): A single entry system is incomplete and is used mainly by small traders.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Profit under single entry is estimated through the capital comparison method.

Reason (R): The difference between closing and opening capital after adjusting for drawings and fresh capital represents profit.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): Drawings are added to closing capital when computing profit.

Reason (R): Drawings have already reduced the closing capital so they must be added back to find the true profit.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Statement of affairs is similar to a balance sheet but is prepared from incomplete records.

Reason (R): Capital in statement of affairs is the balancing figure not derived from the books.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): The conversion method gives a more accurate profit than the capital comparison method.

Reason (R): The conversion method reconstructs full double entry records using available evidence.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): The single entry system is less complex than the double entry system.

Reason (R): The single entry system records only one aspect of each transaction, while the double entry system records both debit and credit.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): In incomplete records, the profit or loss can be ascertained accurately without any adjustments.

Reason (R): Adjustments are necessary to account for items like depreciation and outstanding expenses.

Show explanationHide explanation

Correct answer: Option 4 —

A is false, but R is true.

Q391 Mark

Assertion (A): A statement of affairs can be used to ascertain the financial position of a business.

Reason (R): It lists assets and liabilities similar to a balance sheet, providing a snapshot of net worth.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: Single entry is suitable for small traders.

Statement 2: It is simple but does not give complete and accurate records.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Capital comparison estimates profit from changes in capital.

Statement 2: The method ignores actual revenues and expenses.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Opening capital is found by preparing a statement of affairs at the start of the period.

Statement 2: Opening capital is needed to compute profit by capital comparison.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Additional capital introduced is deducted from closing capital when computing profit.

Statement 2: Such capital was not earned from operations so it must be excluded.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: The conversion method reconstructs full double-entry records using available evidence.

Statement 2: The conversion method gives more accurate profit than capital comparison.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: The statement of affairs is a method used to ascertain the financial position of a business at a specific point in time.

Statement 2: The single entry system records all transactions in a systematic manner similar to the double entry system.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q461 Mark

Statement 1: In incomplete records, the profit or loss can be determined by comparing the opening and closing capital.

Statement 2: The preparation of a balance sheet is not possible under the single entry system.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: Adjustments in incomplete records may include accounting for outstanding expenses.

Statement 2: The single entry system is more complex than the double entry system.

Show answerHide answer

Correct answer: Option 4 —

Both statements are false.

Case Study / Passage Questions4 questions

Q483 Marks

Mr Sushil keeps no proper books. From his records: Capital on 1 April 2023 ₹120000; Drawings during year ₹15000; Additional capital introduced ₹10000; Closing capital on 31 March 2024 ₹160000.

Profit by capital comparison method =

AClosing capital + Drawings − Additional capital − Opening capital

BClosing capital − Drawings + Additional capital − Opening capital

CDrawings + Additional capital − Closing capital

DOpening capital − Closing capital

Profit for the year is:

A₹40000

B₹45000

C₹35000

D₹20000

Compute the profit and explain the reasoning.

Show answersHide answers

1. Option 1 — Closing capital + Drawings − Additional capital − Opening capital

2. Option 2 — ₹45000

3. Capital comparison method: Profit = Closing capital − Opening capital + Drawings − Additional capital. Substituting: = 160000 − 120000 + 15000 − 10000 = ₹45000. Logic: Closing capital reflects all changes during the year. Drawings reduced capital so they must be added back (they are not losses but distributions to owner). Additional capital increased capital from external source so it is subtracted (not earned from operations). The remaining increase is the profit. This method is the simplest under single entry but gives only the bottom line — no information on revenues, expenses, or what drove profit.

Q493 Marks

M/s Sushil uses single entry but his CA wants to convert to double entry to prepare proper financial statements. The CA gathers source documents — bank statements vouchers receipts and stock records.

The conversion method is used:

ATo audit only

BTo convert single entry to double entry

CTo skip year-end

DTo replace ledgers

The first step is to gather:

AStatement of affairs

BTrial balance

CBank statement

DSource documents

List the steps of conversion method.

Show answersHide answers

1. Option 2 — To convert single entry to double entry

2. Option 4 — Source documents

3. Conversion method steps: (1) Gather source documents — bills vouchers receipts bank statements stock records salary records. (2) Reconstruct opening statement of affairs to find opening capital. (3) Build a debtors' control account from sales invoices and customer payments to derive total credit sales. (4) Build a creditors' control account similarly for credit purchases. (5) Aggregate cash receipts and payments from cash records or bank statements. (6) Compile expenses and incomes from vouchers. (7) Prepare adjusted trading account P&L account and balance sheet. The conversion is laborious but yields a true and fair view much better than the simple capital comparison method.

Q503 Marks

On 31 March 2024 M/s Anil Stores has: Cash ₹15000; Stock ₹40000; Debtors ₹30000; Furniture ₹20000; Bank balance ₹25000; Creditors ₹15000; Bank loan ₹10000.

To find capital from incomplete records prepare:

AStatement of affairs

BTrial balance

CCash flow statement

DP&L account

Capital on 31 March 2024 is:

A₹105000

B₹130000

C₹150000

D₹80000

Prepare the statement of affairs and find the capital.

Show answersHide answers

1. Option 1 — Statement of affairs

2. Option 1 — ₹105000

3. Statement of Affairs as on 31 March 2024: Liabilities = Capital (balancing figure) + Creditors 15000 + Bank loan 10000. Assets = Cash 15000 + Stock 40000 + Debtors 30000 + Furniture 20000 + Bank 25000 = ₹130000. So Capital + 25000 = 130000 ⇒ Capital = ₹105000. The statement of affairs is similar to a balance sheet but capital is the balancing figure (Assets − Liabilities) rather than derived from books. This is the essential difference: in proper books capital comes from the ledger; under single entry it must be back-calculated.

Q513 Marks

In the context of incomplete records, the single entry system is often utilized by small businesses. This system records only cash transactions and does not maintain a complete set of accounts. As a result, it becomes challenging to ascertain the exact profit or loss of the business. To prepare financial statements, a statement of affairs is created, which lists assets and liabilities to determine the owner's equity. Understanding the limitations of incomplete records is crucial for accurate financial reporting.

What is the primary limitation of the single entry system?

AIt records all transactions accurately.

BIt does not provide complete financial information.

CIt requires extensive documentation.

DIt is suitable for large corporations.

Define the statement of affairs in the context of incomplete records.

Which of the following is NOT a characteristic of the single entry system?

ARecords only cash transactions.

BMaintains a complete ledger.

CDifficult to ascertain profit or loss.

DUsed by small businesses.

Show answersHide answers

1. Option 2 — It does not provide complete financial information.

2. The statement of affairs is a financial statement that lists the assets and liabilities of a business to determine the owner's equity.

3. Option 2 — Maintains a complete ledger.

Table-Based Questions4 questions

Q523 Marks

Compare single entry and double entry systems:

Aspect

Single entry

Double entry

Recording

Partial (mostly personal accounts)

Both debit and credit

Reliability

Less reliable

Reliable

Trial balance

Cannot be prepared

Always preparable

Profit determination

Capital comparison method

P&L account

Suitability

Small traders

All sizes

Legal recognition

Not for companies

Mandatory for companies

Which is generally used by very small traders?

ASingle entry

BDouble entry

CBoth

DNeither

Which is mandatory for companies under the Companies Act?

ASingle entry

BDouble entry

CCash basis

DAccrual basis

Why is double entry mandatory for companies?

Show answersHide answers

1. Option 1 — Single entry

2. Option 2 — Double entry

3. Single entry is incomplete and unscientific — only personal accounts (debtors creditors) are routinely maintained while real and nominal accounts are partial or absent. Double entry is complete: every transaction has both debit and credit aspects so a trial balance can verify arithmetic accuracy. Profit under single entry is estimated by comparing capital across periods (not separating revenues from expenses); under double entry profit is computed properly from the P&L Account. Single entry is acceptable only for very small unincorporated businesses; companies and most growing enterprises must use double entry.

Q533 Marks

Steps in conversion method (single entry to double entry):

Step

Action

Output

1

Gather source documents

List of bills vouchers receipts

2

Prepare opening statement of affairs

Opening capital

3

Reconstruct debtors control account

Total credit sales

4

Reconstruct creditors control account

Total credit purchases

5

Compile cash and bank summary

Total cash receipts and payments

6

List expenses and incomes from vouchers

Trading and P&L items

7

Prepare trading P&L and balance sheet

Final accounts

The opening capital is found in:

AStep 1

BStep 2

CStep 3

DStep 7

Total credit sales and purchases come from:

AStep 3 and 4

BStep 1

CStep 6

DStep 7

Why is the conversion method preferred over capital comparison?

Show answersHide answers

1. Option 2 — Step 2

2. Option 1 — Step 3 and 4

3. The conversion method systematically rebuilds full double-entry records from incomplete data. Step 1 gathers ALL available evidence — paper bills vouchers receipts bank statements stock registers customer correspondence. Step 2 fills gaps in opening balances. Steps 3-4 use the debtors and creditors accounts as control accounts: opening balance + credit sales (or purchases) − collections (or payments) = closing balance — solve for the unknown. Steps 5-6 build up cash flows and operating items. Step 7 produces the final statements. The output is far more reliable than a simple capital-comparison estimate but takes significantly more effort.

Q546 Marks

Compute capital and prepare statement of affairs from the data below; ascertain profit for the year by capital comparison method.

Item

1 Apr 2023

31 Mar 2024

Cash

₹10000

₹15000

Stock

₹35000

₹50000

Debtors

₹25000

₹35000

Furniture

₹20000

₹18000

Creditors

₹15000

₹20000

Drawings during year

—

₹18000

Additional capital

—

₹12000

Q556 Marks

Find profit for M/s Sushil Stores by capital comparison method using the figures below.

Item

Amount

Opening capital (1 Apr 2023)

₹120000

Closing capital (31 Mar 2024)

₹160000

Drawings during the year

₹15000

Additional capital introduced

₹10000

Picture-Based Questions4 questions

Q563 Marks

Study the comparison of single and double entry systems and answer:

Which system records both debit and credit aspects?

ASingle entry

BDouble entry

CBoth

DNeither

Which is mandatory for companies under the Companies Act 2013?

ASingle entry

BDouble entry

CEither

DNeither

Distinguish between single and double entry systems.

Show answersHide answers

1. Option 2 — Double entry

2. Option 2 — Double entry

3. Single entry is INCOMPLETE: only some transactions are recorded with both aspects, mostly personal accounts (debtors, creditors). Real and nominal accounts are partial or absent. Profit is estimated by comparing capital across periods rather than from a P&L Account. No trial balance can be prepared. Suitable only for very small unincorporated traders. Double entry is COMPLETE: every transaction has both debit and credit aspects, all account types are maintained, a trial balance can be prepared to check arithmetic accuracy, and proper financial statements (Trading + P&L + Balance Sheet) can be drawn up. Mandatory for companies under the Companies Act 2013, accepted by tax authorities, and required by banks for credit. The cost of double entry is higher (training, time) but its benefits (accuracy, comparability, compliance) far outweigh the cost for any business of size.

Q576 Marks

Based on the given flowchart, answer the following:

What is the first step in the conversion method?

AIdentify Assets

BIdentify Liabilities

CDetermine Capital

DPrepare Statement of Affairs

What does the final step involve?

AIdentify Assets

BDetermine Capital

CPrepare Statement of Affairs

DIdentify Liabilities

Explain the importance of identifying liabilities in the conversion method.

What is one major limitation of incomplete records?

ALack of Detailed Records

BExcessive Documentation

CHigh Accuracy

DNone of the above

How does incomplete records affect profit calculation?

List one consequence of having an inaccurate financial position.

What is the first step in preparing the Trading and Profit & Loss Account?

ACollect Data

BCalculate Gross Profit

CDetermine Expenses

DCalculate Net Profit

What do you calculate after determining gross profit?

ANet Profit

BTotal Revenue

CTotal Assets

DTotal Liabilities

Describe the significance of calculating net profit.

Show answersHide answers

1. Option 1 — Identify Assets

2. Option 3 — Prepare Statement of Affairs

3. Identifying liabilities is crucial to determine the net worth of the business.

4. Option 1 — Lack of Detailed Records

5. It makes it difficult to ascertain the actual profit.

6. It can lead to poor decision-making.

7. Option 1 — Collect Data

8. Option 1 — Net Profit

9. It indicates the overall profitability of the business.

Q583 Marks

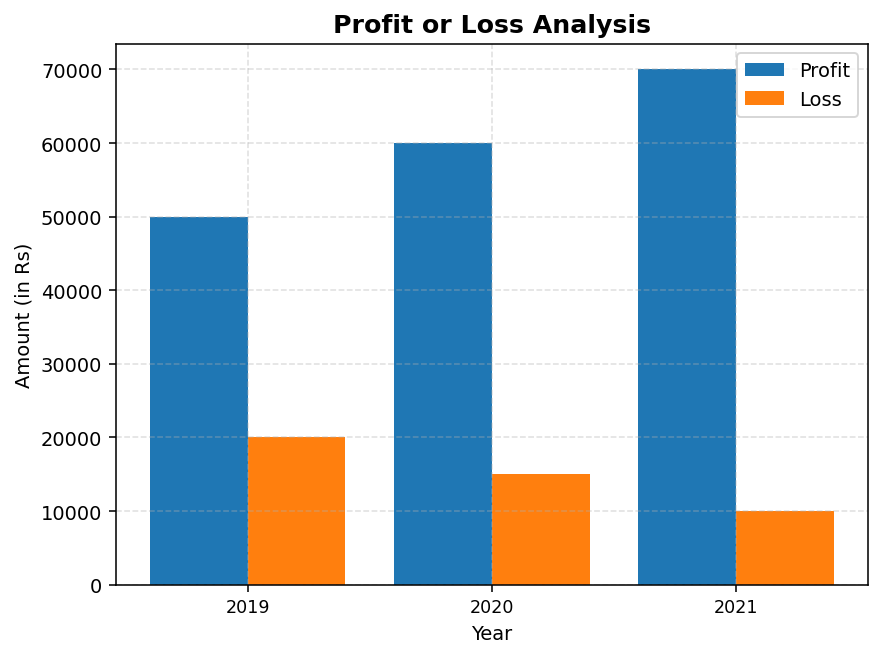

Based on the given chart, answer the following:

In which year was the profit highest?

A2019

B2020

C2021

DNone of the above

What was the total loss over the three years?

Calculate the net profit for the year 2020.

Which expense category has the highest percentage?

ARent

BSalaries

CUtilities

DMiscellaneous

What is the percentage of Salaries in total expenses?

Explain the importance of tracking expense distribution.

Show answersHide answers

1. Option 3 — 2021

2. 45000

3. 45000

4. Option 1 — Rent

5. 25%

6. It helps in budgeting and controlling costs.

Q593 Marks

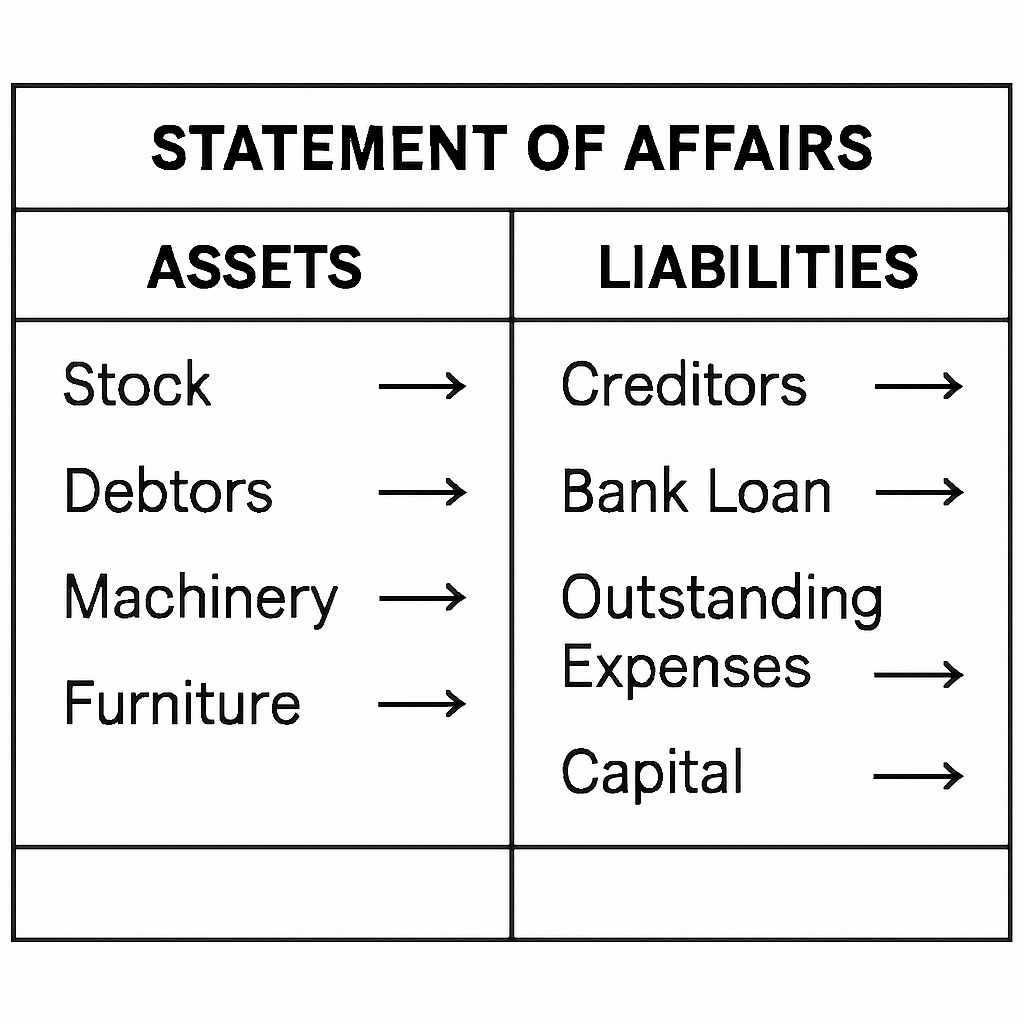

Based on the given diagram of a Statement of Affairs, answer the following:

Identify one asset from the Statement of Affairs.

ACash

BLiabilities

CExpenses

DRevenue

What is the purpose of a Statement of Affairs?

Explain how liabilities are presented in the Statement of Affairs.

Show answersHide answers

1. Option 1 — Cash

2. To provide a snapshot of the financial position of a business.

3. Liabilities are listed separately to show the obligations of the business.