Bank Reconciliation Statement — Important Questions

56 questions

With answersCBSE format

SUMMARY: The chapter on Bank Reconciliation Statement in Class 11 Accountancy explains the process of reconciling the differences between the bank balance as per the cash book and the bank statement. KEY TOPICS: bank reconciliation, cash book, passbook, causes of differences, timing differences, errors in recording, outstanding checks, deposits in transit, adjusted cash book balance, preparation of bank reconciliation statement

A cheque issued but not yet presented for payment is called a:

ACheque deposited

BCheque issued

CCheque outstanding

DCheque dishonoured

Check answerHide answer

Correct answer: Option 3 — Cheque outstanding

Q31 Mark

Bank charges debited by the bank but not yet recorded in the cash book will:

AIncrease the cash book balance

BDecrease the cash book balance only on entry

CHave no effect

DNone of these

Check answerHide answer

Correct answer: Option 2 — Decrease the cash book balance only on entry

Q41 Mark

A debit balance in the bank column of the cash book represents:

ABank overdraft

BFavourable bank balance

CInsufficient funds

DCheque issued

Check answerHide answer

Correct answer: Option 2 — Favourable bank balance

Q51 Mark

If the pass book shows a credit balance of ₹5000 and a cheque of ₹2000 issued is not yet presented the cash book balance will be:

A₹3000

B₹5000

C₹7000

D₹2000

Check answerHide answer

Correct answer: Option 1 — ₹3000

Q61 Mark

What is the primary purpose of preparing a bank reconciliation statement?

ATo determine the exact cash balance in the cash book

BTo identify discrepancies between bank statement and cash book

CTo calculate total bank charges for the month

DTo record all transactions in the cash book

Check answerHide answer

Correct answer: Option 2 — To identify discrepancies between bank statement and cash book

Q71 Mark

Which of the following is considered a timing difference in bank reconciliation?

AOutstanding checks

BBank errors

CDeposits in transit

DBoth outstanding checks and deposits in transit

Check answerHide answer

Correct answer: Option 4 — Both outstanding checks and deposits in transit

Q81 Mark

If a bank statement shows a balance of ₹10,000 and there are outstanding checks of ₹3,000, what is the adjusted bank balance?

A₹7,000

B₹10,000

C₹13,000

D₹3,000

Check answerHide answer

Correct answer: Option 1 — ₹7,000

Q91 Mark

Which of the following items would NOT cause a difference between the cash book and the bank statement?

ADeposits in transit

BBank service charges

CErrors in cash book entries

DInterest earned on savings account

Check answerHide answer

Correct answer: Option 4 — Interest earned on savings account

Q101 Mark

In a bank reconciliation statement, what does an 'outstanding check' refer to?

AA check that has been deposited but not cleared

BA check that has been issued but not yet cashed

CA check that has been lost

DA check that has been returned due to insufficient funds

Check answerHide answer

Correct answer: Option 2 — A check that has been issued but not yet cashed

Q111 Mark

When preparing a bank reconciliation statement, which of the following adjustments would be made to the cash book?

AAdd outstanding checks

BSubtract bank charges

CAdd deposits in transit

DSubtract interest earned

Check answerHide answer

Correct answer: Option 2 — Subtract bank charges

Q121 Mark

What is the effect of a bank error that resulted in an incorrect debit to the bank statement?

AIt increases the cash book balance

BIt decreases the cash book balance

CIt has no effect on the cash book balance

DIt requires a correction in the cash book

Check answerHide answer

Correct answer: Option 1 — It increases the cash book balance

Q131 Mark

If a deposit is made but not yet reflected in the bank statement, it is known as:

AOutstanding deposit

BDeposits in transit

CBank error

DUncleared deposit

Check answerHide answer

Correct answer: Option 2 — Deposits in transit

Q141 Mark

Which of the following would be added to the bank balance in the reconciliation process?

AOutstanding checks

BDeposits in transit

CBank service charges

DErrors in cash book

Check answerHide answer

Correct answer: Option 2 — Deposits in transit

Q151 Mark

A discrepancy between the cash book and the bank statement can arise from:

AOnly timing differences

BOnly errors in recording

CBoth timing differences and errors in recording

DOnly outstanding checks

Check answerHide answer

Correct answer: Option 3 — Both timing differences and errors in recording

Short Answer Questions10 questions

Q163 Marks

Define a bank reconciliation statement.

View sample solutionHide solution

A Bank Reconciliation Statement (BRS) is a statement prepared periodically by a business to reconcile the bank column balance of its cash book with the balance shown in the bank's pass book (or bank statement). It identifies the reasons for any difference and ensures that the records of the business agree with those of the bank.

Q173 Marks

List any three causes of disagreement between the cash book and the pass book.

View sample solutionHide solution

(i) Cheques issued but not yet presented for payment — recorded in cash book but not in pass book. (ii) Cheques deposited but not yet credited (in transit) — recorded in cash book but not in pass book yet. (iii) Bank charges or interest credited by bank but not yet recorded in cash book. Other causes: direct deposits by customers, dishonoured cheques, errors by either party.

Q183 Marks

What is a bank overdraft and how is it represented in the books?

View sample solutionHide solution

A bank overdraft is a negative bank balance — the firm has withdrawn more from the bank than was deposited (a short-term loan from the bank). In the cash book, it appears as a credit balance in the bank column. In the pass book, it appears as a debit balance (favourable to the bank). When preparing BRS starting from a credit balance in the cash book, items that increase the overdraft are added.

Q193 Marks

Explain the difference between cash book and pass book.

View sample solutionHide solution

Cash book is maintained by the business; records all cash and bank transactions of the business; primary source for cash receipts and payments. Pass book is maintained by the bank; records only the bank-related transactions of the customer from the bank's perspective; debit and credit are reversed compared to the cash book (deposits credit the customer in the bank's books). BRS reconciles the two.

Q203 Marks

How is interest on bank deposits treated in BRS?

View sample solutionHide solution

Interest credited by the bank on deposits is recorded by the bank in the pass book first (credit to customer) but the business may not learn of it until receiving the bank statement. So when reconciling: pass book balance is more than cash book balance; in the BRS starting from cash book (favourable balance), add interest credited; the items moves the cash book up to match the pass book. The business should also pass an entry: Bank A/c Dr; To Interest Received A/c.

Q213 Marks

What are outstanding checks and how do they affect the bank reconciliation statement?

View sample solutionHide solution

Outstanding checks are checks that have been written and recorded in the cash book but have not yet cleared the bank. They reduce the bank balance in the cash book but are not reflected in the bank statement, leading to a difference that needs to be reconciled.

Q223 Marks

Explain the term 'deposits in transit' and its significance in bank reconciliation.

View sample solutionHide solution

Deposits in transit refer to amounts that have been received and recorded in the cash book but have not yet been processed by the bank. They are added to the bank statement balance during reconciliation to ensure accurate matching of the balances.

Q233 Marks

What is the purpose of preparing a bank reconciliation statement?

View sample solutionHide solution

The purpose of preparing a bank reconciliation statement is to identify and explain the differences between the cash book and the bank statement balances, ensuring that both records are accurate and up-to-date.

Q243 Marks

Describe how timing differences can lead to discrepancies in bank reconciliation.

View sample solutionHide solution

Timing differences occur when transactions are recorded at different times in the cash book and the bank statement. For example, a deposit made late in the day may not appear in the bank statement until the next day, causing a temporary mismatch in balances.

Q253 Marks

What role do errors in recording play in bank reconciliation?

View sample solutionHide solution

Errors in recording can arise from mistakes made in the cash book or the bank statement, such as incorrect amounts or missed transactions. These errors must be identified and corrected during the reconciliation process to ensure accurate financial records.

Long Answer Questions6 questions

Q266 Marks

Prepare a BRS as on 31 March 2024 from the following: cash book balance (Dr) ₹35000; cheques issued ₹8000 not yet presented; cheques deposited ₹6000 not yet credited; bank charges ₹500 not in cash book; interest credited ₹400 not in cash book; cheque dishonoured ₹1500 not in cash book.

View sample solutionHide solution

BRS as on 31 March 2024 (start with cash book balance): Cash book balance Dr ₹35000. Add: cheques issued not presented +8000 (increase pass book); interest credited +400. Less: cheques deposited not credited −6000; bank charges −500; cheque dishonoured −1500. Pass book balance = 35000 + 8000 + 400 − 6000 − 500 − 1500 = ₹35400 (Cr). The BRS shows the journey from cash book to pass book balance, identifying each timing or recording difference.

Q276 Marks

From the following extract of a cash book and pass book of Mr Vinod, prepare a BRS as on 31 March 2024: cash book bank column balance ₹50000 Dr; cheques deposited ₹8000 of which ₹3000 credited by bank; cheques issued ₹15000 of which ₹6000 not yet presented; bank paid ₹2000 insurance premium standing instructions not in cash book; bank credited interest ₹1200 not in cash book.

View sample solutionHide solution

BRS as on 31 March 2024 (starting with cash book balance ₹50000 Dr): Add: cheques issued not yet presented +6000; interest credited by bank +1200. Less: cheques deposited not yet credited (8000 deposited − 3000 credited = ₹5000 in transit) −5000; insurance premium paid by bank not in cash book −2000. Balance per pass book = 50000 + 6000 + 1200 − 5000 − 2000 = ₹50200 (Cr). Mr Vinod should also pass adjusting entries in the cash book for ₹2000 (Insurance A/c Dr; To Bank A/c) and ₹1200 (Bank A/c Dr; To Interest Received A/c).

Q286 Marks

Explain the reasons why the cash book balance and pass book balance may differ.

View sample solutionHide solution

The cash book and pass book record the same set of transactions but from different perspectives, so timing and recording differences arise: (1) Cheques issued but not yet presented — entered immediately in cash book; recorded in pass book only when payee presents the cheque. (2) Cheques deposited but not yet collected — entered in cash book on deposit; pass book credits only on bank's receipt of funds. (3) Direct deposits / collections by bank — bank credits customer (e.g., interest, dividend collection) but customer learns later. (4) Direct payments / charges by bank — bank debits customer (insurance, instalments, charges) but customer learns later. (5) Errors — either party could make recording mistakes. (6) Dishonoured cheques — recorded as receipt in cash book but reversed in pass book on dishonour. (7) Interest on deposits credited by bank — known later. BRS systematically lists these to reconcile the two balances.

Q296 Marks

What is meant by an 'amended' or 'adjusted' cash book? Why is it prepared in some BRS questions, and what is the procedure?

View sample solutionHide solution

An amended or adjusted cash book is prepared when the cash book itself contains errors or omissions that the bank has correctly recorded — for example, bank charges or interest that the customer has not yet entered. Procedure: (i) start with the cash book balance; (ii) bring into the cash book all bank-side adjustments that the customer has not yet recorded — bank charges, interest received, direct payments, etc.; (iii) close the amended cash book to find the correct balance. The amended cash book balance should be used as the starting point for BRS instead of the original cash book balance — this gives a cleaner reconciliation focused only on timing differences (cheques in transit, cheques not presented).

Q306 Marks

Distinguish between cash book and pass book, and explain the importance of BRS.

View sample solutionHide solution

Cash book is maintained by the business; records all cash and bank transactions; debit side records receipts; bank column shows bank balance from business's view. Pass book is maintained by the bank; records the customer's account from the bank's perspective; debits and credits are reversed (deposit by customer is a credit in pass book). Importance of BRS: (1) detects errors in cash book or pass book; (2) checks for fraud — unauthorised transactions surface during reconciliation; (3) ensures correct bank balance is reported in financial statements; (4) helps in cash management — reveals cheques in transit and outstanding cheques; (5) provides documentary support for audit. Many businesses prepare BRS monthly as a control measure.

Q316 Marks

Compare cash book and pass book with the help of a table.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): A BRS is prepared to reconcile the cash book balance with the pass book balance.

Reason (R): The cash book and pass book balances may differ due to timing and recording differences.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): A bank overdraft appears as a credit balance in the cash book bank column.

Reason (R): An overdraft means the bank has lent money to the firm and is owed by the firm.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): A cheque deposited into the bank but not yet credited makes the cash book balance higher than the pass book balance.

Reason (R): The cash book records the deposit immediately whereas the bank credits the customer only on collection.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Bank charges debited by the bank reduce the pass book balance.

Reason (R): Bank charges are debits in the bank's books which lower the customer's balance with the bank.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): An adjusted cash book is prepared before BRS in some cases.

Reason (R): Items already recorded by the bank but not yet recorded in the cash book are first updated in the cash book to reduce the number of reconciling items.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): Outstanding checks are checks issued by the bank but not yet presented for payment.

Reason (R): Outstanding checks decrease the balance shown in the cash book.

Show explanationHide explanation

Correct answer: Option 3 —

A is true, but R is false.

Q381 Mark

Assertion (A): Deposits in transit are amounts received and recorded in the cash book but not yet reflected in the bank statement.

Reason (R): Deposits in transit increase the bank balance as per the pass book.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q391 Mark

Assertion (A): Errors in recording transactions can lead to discrepancies between the cash book and the pass book.

Reason (R): Such errors are always in favor of the cash book balance.

Show explanationHide explanation

Correct answer: Option 3 —

A is true, but R is false.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: A BRS is generally prepared every month.

Statement 2: Frequent reconciliation helps detect errors and frauds early.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Outstanding cheques cause the pass book balance to be higher than the cash book.

Statement 2: Cheques issued have already reduced the cash book balance but the bank pays the cheques only when presented.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: A direct deposit by a customer increases the pass book balance.

Statement 2: The business may not know about the deposit until it receives the bank statement.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: A credit balance in the pass book represents a favourable balance for the customer.

Statement 2: The bank owes money to the customer to the extent of the credit balance.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: A BRS helps in detecting fraud.

Statement 2: Comparison between cash book and pass book may reveal unauthorised entries.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: Deposits in transit are amounts that have been recorded in the cash book but not yet reflected in the passbook.

Statement 2: Outstanding checks are checks issued by the bank that have not yet been presented for payment.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q461 Mark

Statement 1: Errors in recording transactions in the cash book can lead to discrepancies in the bank reconciliation statement.

Statement 2: The adjusted cash book balance is always equal to the passbook balance after reconciliation.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: A bank reconciliation statement is prepared to ensure that the cash book and passbook balances match.

Statement 2: Timing differences can occur due to delays in processing transactions by the bank.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Case Study / Passage Questions4 questions

Q483 Marks

On 31 March 2024 Mr Vinod has cash book bank balance ₹50000 (Dr). He notes: cheques issued ₹15000 of which ₹6000 not yet presented; cheques deposited ₹8000 of which ₹3000 still not credited; bank charged ₹500 not in cash book; bank credited interest ₹400 not in cash book.

The cash book and pass book balances may differ due to:

ASame balance

BDifferent balances temporarily

CAlways different

DAlways same

To get the pass book balance from cash book ₹50000:

AAdd both to cash book

BSubtract from cash book

CAdd 6000 less 5000 less 500 plus 400

DSkip these adjustments

Prepare Vinod's BRS and explain the reasoning.

Show answersHide answers

1. Option 2 — Different balances temporarily

2. Option 3 — Add 6000 less 5000 less 500 plus 400

3. BRS as on 31 March 2024 (start cash book balance ₹50000 Dr): Add cheques issued not presented ₹6000; Add interest credited ₹400. Less cheques deposited not credited ₹5000; Less bank charges ₹500. Pass book balance = 50000 + 6000 + 400 − 5000 − 500 = ₹50900 (Cr). Reasoning: items that increase pass book balance vs cash book are added; items that reduce it are subtracted. Vinod should also pass adjusting entries in the cash book for the ₹500 bank charges (Charges A/c Dr; To Bank A/c) and ₹400 interest (Bank A/c Dr; To Interest A/c) so the next period starts with a clean cash book.

Q493 Marks

M/s Kabir Stores has an overdraft of ₹20000 (Cr balance in cash book bank column) on 31 March 2024. Cheques issued ₹8000 not presented; cheques deposited ₹6000 not credited; bank levied charges ₹600 not in cash book.

An overdraft is reflected in the cash book bank column as a:

ADr balance

BCr balance

CBoth

DNeither

Cheques deposited but not yet credited:

AIncreases the overdraft

BDecreases the overdraft

CNo effect

DDoubles the overdraft

Prepare BRS for the overdraft case.

Show answersHide answers

1. Option 2 — Cr balance

2. Option 1 — Increases the overdraft

3. BRS for an overdraft (start with Cr balance in cash book ₹20000): Items that REDUCE the overdraft are added; items that INCREASE the overdraft are subtracted. Add cheques issued not presented +8000 (these have not actually left bank — overdraft is less than recorded). Less cheques deposited not credited −6000 (these have not yet been received by bank — overdraft is more than recorded). Less bank charges −600 (overdraft increased). Pass book overdraft = 20000 − 8000 + 6000 + 600 = ₹18600 (Cr in pass book = Dr in customer's records of bank). The signs are reversed because we're starting from a credit balance.

Q503 Marks

Mrs Patel's cash book shows balance ₹40000 (Dr) on 31 March 2024. She finds: cheque issued ₹3000 not presented; cheque deposited ₹4000 still in transit; bank charges ₹200 not yet recorded; interest credited ₹500 not yet recorded; standing instruction insurance paid by bank ₹1000 not yet recorded.

An adjusted cash book is prepared mainly:

ATo find errors

BTo remove items already in bank books from BRS

CTo replace BRS

DTo save time

The adjusted cash book balance is:

A₹40000

B₹39300

C₹40500

D₹41000

Compute adjusted cash book and final BRS.

Show answersHide answers

1. Option 2 — To remove items already in bank books from BRS

2. Option 2 — ₹39300

3. Adjusted cash book corrects the cash book first for items already in the bank's books: Cash book balance 40000. Add interest credited +500. Less bank charges −200; Less insurance paid by bank −1000. Adjusted balance = 40000 + 500 − 200 − 1000 = ₹39300. BRS now uses only timing items: Adjusted cash book ₹39300. Add cheque issued not presented +3000. Less cheque deposited not credited −4000. Pass book balance = 39300 + 3000 − 4000 = ₹38300 (Cr). The two-step approach (adjusted cash book + BRS) cleanly separates recording differences from timing differences.

Q513 Marks

A Bank Reconciliation Statement (BRS) is a document that compares the cash balance in a company's cash book to the balance shown in its bank statement. The purpose of this statement is to identify any discrepancies between the two records. Discrepancies can arise due to timing differences, such as outstanding checks that have not yet cleared or deposits in transit that have not been recorded by the bank. Additionally, errors in recording transactions in either the cash book or the bank statement can lead to differences. By preparing a BRS, businesses can ensure that their cash records are accurate and up-to-date, which is essential for effective financial management.

What is the primary purpose of preparing a Bank Reconciliation Statement?

ATo calculate net profit

BTo compare cash book balance with bank statement balance

CTo prepare financial statements

DTo determine tax liabilities

List two common causes of discrepancies found in a Bank Reconciliation Statement.

Which of the following is NOT a reason for differences between the cash book and the bank statement?

AOutstanding checks

BDeposits in transit

CBank charges

DSales revenue

Show answersHide answers

1. Option 2 — To compare cash book balance with bank statement balance

2. Outstanding checks and deposits in transit.

3. Option 4 — Sales revenue

Table-Based Questions4 questions

Q523 Marks

Study common reasons for cash-book vs pass-book differences:

Reason

Effect on cash book

Effect on pass book

Cheque issued not presented

Already debited

Not yet recorded

Cheque deposited in transit

Already credited

Not yet recorded

Bank charges

Not recorded

Already debited

Interest credited

Not recorded

Already credited

Direct deposit by customer

Not recorded

Already credited

Cheque dishonour

Already credited

Returned and reversed

A cheque issued but not presented makes the pass book balance ____ relative to the cash book.

ADecrease

BIncrease

CNo change

DCancel

Bank charges debited will ____ the pass book balance relative to the cash book.

AIncrease

BDecrease

CNo change

DEither

Distinguish between timing differences and recording differences in BRS.

Show answersHide answers

1. Option 2 — Increase

2. Option 2 — Decrease

3. Each cause of difference falls into two buckets: (1) Timing differences — both books will eventually record the item but at different points in time (cheques in transit, cheques outstanding). (2) Recording differences — only one book has the item; the other learns later (bank charges, interest, direct deposits, dishonoured cheques). The BRS lists timing differences only; recording differences should be brought into the cash book through adjusting entries before/after BRS. Some firms prepare an adjusted cash book that includes recording adjustments, leaving BRS to handle only timing items.

Q533 Marks

Compare types of cheque transactions and their treatment:

Type

Description

Treatment

Cheque issued

Drawn by us, paid to others

Cash book debit/credit immediately

Cheque deposited

Received from others, deposited

Cash book credited immediately

Cheque outstanding

Issued but not yet presented

Add in BRS to get pass book

Cheque in transit

Deposited but not yet collected

Less in BRS to get pass book

Cheque dishonoured

Returned by bank unpaid

Reverse the original cash book entry

Stale cheque

Older than validity

Bank refuses; reverse entry

A cheque issued but not yet presented should be:

AAdd to cash book

BAdd in BRS

CSubtract in BRS

DSkip

A cheque dishonoured by the bank requires:

AReverse the cash book entry

BIncrease the bank balance

CNo effect

DAdd to BRS

Explain how each type of cheque transaction affects the BRS.

Show answersHide answers

1. Option 2 — Add in BRS

2. Option 1 — Reverse the cash book entry

3. Cheque-related items affect the BRS in different ways. Issued and deposited cheques are recorded in the cash book immediately, but the bank books them only when presented or collected. Outstanding (issued, not presented) cheques cause the pass book balance to be HIGHER than cash book balance — added in BRS. Cheques in transit (deposited, not credited) cause the pass book balance to be LOWER than cash book — subtracted. Dishonoured cheques require reversal in the cash book of the original deposit entry. Stale cheques (older than 3 months in India) are refused by the bank — also need cash book reversal.

Q546 Marks

Prepare a Bank Reconciliation Statement as on 31 March 2024 from the following information.

Item

Amount

Cash book balance (Dr)

₹35000

Cheques issued not yet presented

₹8000

Cheques deposited not yet credited

₹6000

Bank charges debited (not in cash book)

₹500

Interest credited (not in cash book)

₹400

Cheque dishonoured (not in cash book)

₹1500

Q556 Marks

Prepare a BRS for an overdraft as on 31 March 2024 from the following information.

Item

Amount

Cash book overdraft (Cr balance)

₹20000

Cheques issued not presented

₹8000

Cheques deposited not credited

₹6000

Bank charges debited

₹600

Picture-Based Questions1 question

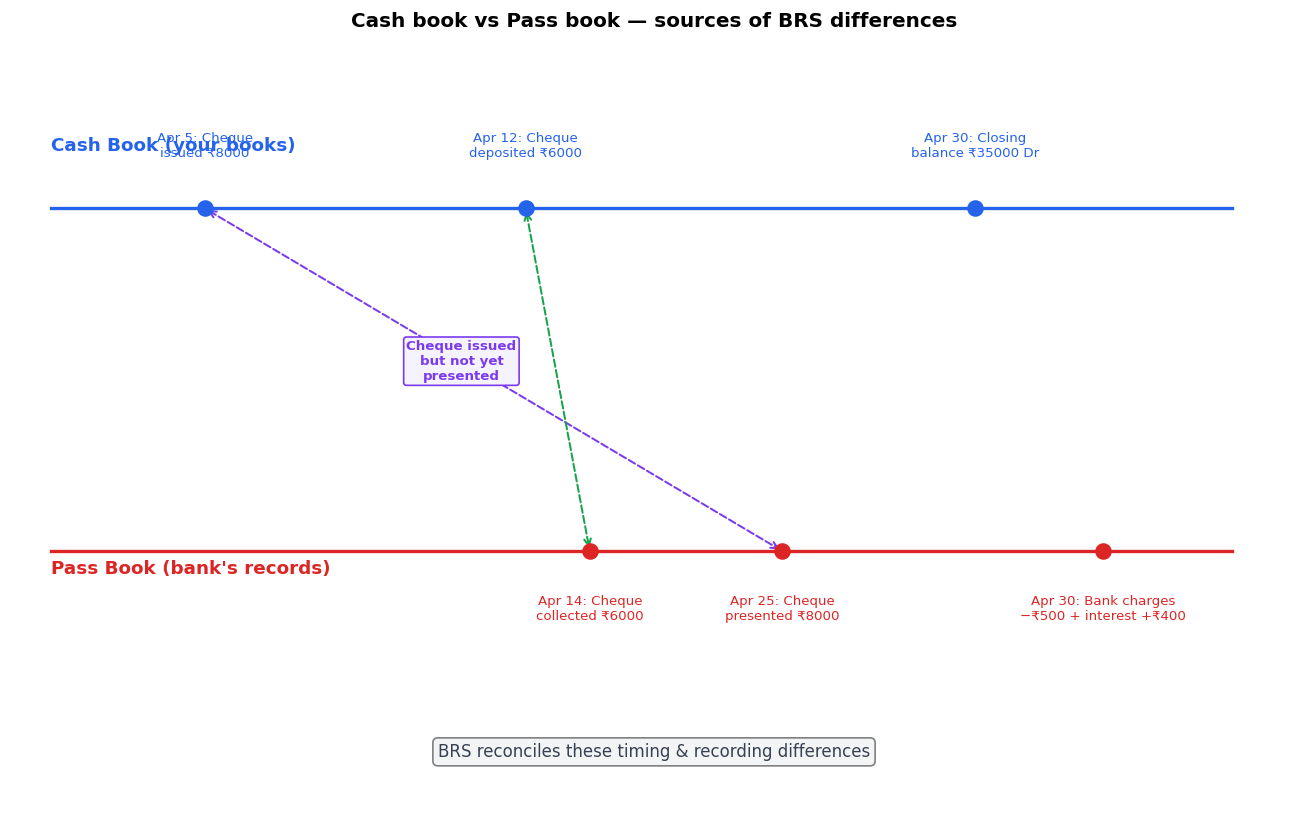

Q563 Marks

Study the cash book and pass book timelines and answer:

A BRS reconciles:

ABank statement

BCash book and pass book

CJournal and ledger

DTrial balance

A cheque issued but not yet presented is an example of:

ARecording difference

BTiming difference

CBoth

DNeither

Distinguish between timing and recording differences with examples.

Show answersHide answers

1. Option 2 — Cash book and pass book

2. Option 2 — Timing difference

3. The cash book and the pass book record the same set of bank transactions but from different perspectives, so timing and recording differences arise. TIMING differences: the firm enters a cheque issued the moment it leaves their hands; the bank debits it only when the payee presents it (could be days later). Similarly cheques deposited are entered immediately in cash book but credited by the bank only when funds clear. RECORDING differences: bank charges, interest, direct deposits, dishonoured cheques may appear first in the pass book; the firm learns of them later through the bank statement. The BRS lists all such differences and reconciles the two balances. Many firms also prepare an 'adjusted cash book' that brings in the recording differences first, leaving the BRS to handle only timing items.