Recording of Transactions - II — Important Questions

55 questions

With answersCBSE format

SUMMARY: This chapter focuses on the process of recording transactions in subsidiary books and the preparation of ledger accounts. KEY TOPICS: subsidiary books, cash book, purchase book, sales book, journal proper, ledger accounts, posting, balancing of accounts, trial balance, rectification of errors

Correct answer: Option 3 — Cash and bank transactions

Q21 Mark

Which subsidiary book is used to record cash purchases?

APurchases book

BCash book

CSales book

DJournal proper

Check answerHide answer

Correct answer: Option 2 — Cash book

Q31 Mark

A petty cash book is maintained on the:

ASingle column system

BDouble column system

CImprest system

DCash basis

Check answerHide answer

Correct answer: Option 3 — Imprest system

Q41 Mark

Sales return book records:

AAll sales

BGoods returned by customers

CGoods returned to suppliers

DAll returns

Check answerHide answer

Correct answer: Option 2 — Goods returned by customers

Q51 Mark

The journal proper is used for recording:

ACash purchases

BCredit purchases

CAdjustment and rare transactions

DSales returns

Check answerHide answer

Correct answer: Option 3 — Adjustment and rare transactions

Q61 Mark

What is the primary purpose of a purchase book?

ATo record cash sales

BTo record credit purchases

CTo record all transactions

DTo record cash receipts

Check answerHide answer

Correct answer: Option 2 — To record credit purchases

Q71 Mark

Which of the following is NOT a type of subsidiary book?

ACash book

BPurchase book

CSales ledger

DSales book

Check answerHide answer

Correct answer: Option 3 — Sales ledger

Q81 Mark

In which book would you record a transaction involving the return of goods sold on credit?

ACash book

BSales return book

CPurchase book

DJournal proper

Check answerHide answer

Correct answer: Option 2 — Sales return book

Q91 Mark

What does the cash book combine features of?

AJournal and ledger

BPurchase book and sales book

CTrial balance and journal

DSales return and purchase return

Check answerHide answer

Correct answer: Option 1 — Journal and ledger

Q101 Mark

Which of the following is true about the ledger accounts?

AThey are used only for cash transactions

BThey summarize all transactions for a specific account

CThey are not required for trial balance preparation

DThey only record credit transactions

Check answerHide answer

Correct answer: Option 2 — They summarize all transactions for a specific account

Q111 Mark

What is the first step in posting transactions to the ledger?

ABalancing the accounts

BRecording in the journal

CPreparing the trial balance

DIdentifying errors

Check answerHide answer

Correct answer: Option 2 — Recording in the journal

Q121 Mark

Which of the following errors would NOT be detected in the trial balance?

ATransposition error

BOmission error

CAddition error

DRecording error

Check answerHide answer

Correct answer: Option 2 — Omission error

Q131 Mark

What is the main function of the trial balance?

ATo record errors

BTo summarize the balances of all accounts

CTo prepare financial statements

DTo record cash transactions only

Check answerHide answer

Correct answer: Option 2 — To summarize the balances of all accounts

Q141 Mark

When a transaction is recorded in the journal proper, which of the following is true?

AIt is recorded in chronological order

BIt is recorded in alphabetical order

CIt is recorded only for cash transactions

DIt is recorded for assets only

Check answerHide answer

Correct answer: Option 1 — It is recorded in chronological order

Q151 Mark

Which book would you use to record a cash sale?

ASales book

BPurchase book

CCash book

DJournal proper

Check answerHide answer

Correct answer: Option 3 — Cash book

Short Answer Questions10 questions

Q163 Marks

Distinguish between a single column and a double column cash book.

View sample solutionHide solution

Single column cash book records only cash transactions; has one amount column on each side. Double column cash book has both cash and bank columns; records all cash and bank transactions; useful when both cash and bank accounts have many transactions. Some firms use a triple column cash book that adds a discount column to record cash discounts allowed and received.

Q173 Marks

What is a contra entry? Give an example.

View sample solutionHide solution

A contra entry involves both cash and bank accounts: cash deposited into bank or cash withdrawn from bank. The same transaction is debited and credited within the cash book itself. Example: ₹5000 cash deposited into bank — Bank A/c Dr ₹5000 (in bank column); Cash A/c Cr ₹5000 (in cash column). The letter 'C' is written in the L.F. column to indicate a contra entry.

Q183 Marks

Explain the imprest system of petty cash.

View sample solutionHide solution

Under the imprest system, the petty cashier is given a fixed amount (the float) at the start of a period to meet small expenses. At the end of the period, the cashier presents vouchers and the main cashier reimburses the exact amount spent, restoring the petty cash to the original imprest. Advantages: control over petty expenses, regular checking of vouchers, the petty cashier always has a known balance.

Q193 Marks

List any three advantages of subsidiary books.

View sample solutionHide solution

(i) Division of work — different staff can maintain different books concurrently, speeding up recording. (ii) Saving time — similar transactions are recorded together in a single book. (iii) Specialisation — clerks become expert in one type of transaction. (iv) Easier ledger posting — periodic totals are posted instead of each transaction. (v) Easier reference — historical information on each type of transaction is concentrated in one book.

Q203 Marks

What is the purpose of the journal proper?

View sample solutionHide solution

The journal proper records transactions that do not fit into any other subsidiary book. Common entries: (i) opening entries at the start of a year; (ii) closing entries at year-end; (iii) adjustment entries (depreciation, prepaid items); (iv) rectification of errors; (v) transfer entries; (vi) transactions of a non-routine nature like purchase of fixed assets on credit. It works with the other subsidiary books to capture every transaction.

Q213 Marks

What are subsidiary books and why are they used in accounting?

View sample solutionHide solution

Subsidiary books are specialized accounting books used to record specific types of transactions, such as sales, purchases, and cash transactions. They help in organizing financial data and simplifying the recording process before posting to the ledger.

Q223 Marks

Define a cash book and explain its significance in accounting.

View sample solutionHide solution

A cash book is a financial journal that records all cash transactions, both receipts and payments. It serves as both a journal and a ledger, providing a clear view of cash flow and helping in cash management.

Q233 Marks

What is a purchase book and what types of transactions are recorded in it?

View sample solutionHide solution

A purchase book is a subsidiary book used to record all credit purchases of goods. It does not include cash purchases and helps in tracking liabilities and inventory.

Q243 Marks

Explain the process of posting transactions from subsidiary books to the ledger.

View sample solutionHide solution

Posting involves transferring the recorded transactions from subsidiary books to the respective accounts in the ledger. Each entry is posted to ensure that the ledger reflects the updated financial position of the business.

Q253 Marks

What is a sales book and how does it differ from a sales journal?

View sample solutionHide solution

A sales book records all credit sales transactions, while a sales journal is a broader term that can include both cash and credit sales. The sales book specifically focuses on credit sales for better tracking of receivables.

Long Answer Questions6 questions

Q266 Marks

Prepare a triple-column cash book of M/s Sona Trading from the following: 2024 Apr 1 cash balance ₹15000, bank balance ₹40000; Apr 5 sold goods for cash ₹8000; Apr 8 deposited ₹5000 into bank; Apr 12 paid rent by cheque ₹3000; Apr 20 received ₹4900 from Hari and allowed discount ₹100.

View sample solutionHide solution

Triple column cash book has Date | Particulars | L.F. | Discount | Cash | Bank columns on each side. Receipts (Dr): Apr 1 To Balance b/d (Cash 15000, Bank 40000); Apr 5 To Sales A/c — Cash 8000; Apr 8 To Cash A/c (contra C) — Bank 5000; Apr 20 To Hari A/c — Discount Allowed 100, Cash 4900. Payments (Cr): Apr 8 By Bank A/c (contra C) — Cash 5000; Apr 12 By Rent A/c — Bank 3000. Closing balances: Cash = 15000 + 8000 + 4900 − 5000 = ₹22900; Bank = 40000 + 5000 − 3000 = ₹42000. Discount allowed total ₹100 will be posted to discount allowed account.

Q276 Marks

Distinguish between a trade discount and a cash discount with examples.

View sample solutionHide solution

Trade discount — a reduction in catalogue price allowed by seller to buyer to facilitate sale; deducted from invoice price; not recorded in books (only the net amount is). Example: catalogue price ₹1000, trade discount 10% = ₹100, invoice price ₹900 — entry is made for ₹900. Cash discount — a reduction in the amount payable to encourage early payment; recorded in books as discount allowed (by seller) or discount received (by buyer). Example: ₹900 invoice, 2% cash discount on payment within 7 days = ₹18; if customer pays in 5 days, customer pays ₹882 and seller records discount allowed ₹18.

Q286 Marks

Explain the various subsidiary books with the type of transactions recorded in each.

View sample solutionHide solution

(1) Cash book — all cash and bank receipts and payments. (2) Purchases book — credit purchases of goods only (not assets). (3) Sales book — credit sales of goods only. (4) Purchases return (returns outward) book — goods returned to suppliers. (5) Sales return (returns inward) book — goods returned by customers. (6) Bills receivable book — bills accepted by customers. (7) Bills payable book — bills accepted to creditors. (8) Journal proper — opening, closing, adjusting, rectifying, and other rare entries. Each subsidiary book records a specific kind of transaction; together they replace a single huge journal and divide work among accountants.

Q296 Marks

From the following information, prepare a Sales Day Book for January 2024 of Suresh & Co.: Jan 5 sold to Manoj 100 chairs @ ₹500 each less 10% trade discount; Jan 12 sold to Verma 50 chairs @ ₹500 each less 10% trade discount; Jan 18 sold for cash 30 chairs @ ₹500 each (do not record in sales book).

View sample solutionHide solution

Sales Day Book records only credit sales of goods. Computation: Jan 5 Manoj — gross 100×500 = 50000; less trade discount 10% = 5000; net invoice ₹45000. Jan 12 Verma — gross 50×500 = 25000; less 10% = 2500; net ₹22500. Jan 18 cash sale — recorded in cash book, NOT in sales book. Sales Day Book entries: Jan 5 Manoj ₹45000; Jan 12 Verma ₹22500. Total ₹67500. Posting: each customer's account is debited individually; the total ₹67500 is credited to Sales A/c at month end.

Q306 Marks

Explain the special features and advantages of a triple column cash book.

View sample solutionHide solution

Triple column cash book has three amount columns on each side: discount, cash, bank. Features: (a) acts as both journal (records transactions) and ledger (cash and bank A/c); (b) records all cash and bank receipts/payments and discounts allowed/received; (c) contra entries are recorded by 'C' in L.F. column. Advantages: (1) saves time — one book instead of three; (2) facilitates daily cash and bank balances; (3) controls cash and bank movement; (4) enables ready computation of total discounts. Used by most small and mid-sized firms in India where cash, bank, and discounts are routine.

Q316 Marks

Compare double-column and three-column cash book with the help of a table.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): The cash book serves as both journal and ledger.

Reason (R): The cash book records cash transactions chronologically and also gives the cash balance at any time.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): A contra entry is marked with 'C' in the L.F. column.

Reason (R): A contra entry is recorded on both sides of the cash book and does not require separate ledger posting.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): Under the imprest system the petty cashier is reimbursed periodically for expenses incurred.

Reason (R): The imprest system maintains a fixed float of cash with the petty cashier so that small expenses can be met promptly.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Subsidiary books divide accounting work among multiple staff.

Reason (R): Each subsidiary book records a specific kind of transaction making division of labour possible.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Trade discount is not recorded in the books of accounts.

Reason (R): Trade discount is deducted from the catalogue price before the invoice is prepared so only the net amount is entered.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): The purchase book is used to record all credit purchases of goods.

Reason (R): The purchase book helps in maintaining a separate record for purchases, facilitating easier tracking.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): The sales book records all cash sales made by the business.

Reason (R): The sales book is specifically designed to record credit sales only.

Show explanationHide explanation

Correct answer: Option 3 —

A is true, but R is false.

Q391 Mark

Assertion (A): Posting refers to transferring entries from subsidiary books to the ledger.

Reason (R): Posting is an essential step in the accounting cycle that ensures all transactions are recorded in the ledger.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: The cash book records all cash and bank transactions.

Statement 2: The cash book is one of the most important subsidiary books.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: The purchases book records only credit purchases of goods.

Statement 2: Purchases of fixed assets on credit are recorded in the journal proper not in the purchases book.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: The petty cash book records small cash payments.

Statement 2: The petty cashier is reimbursed at the end of each period to restore the original imprest.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Cash discount allowed is recorded in the cash book.

Statement 2: Cash discount encourages prompt payment by customers.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Goods returned by customers are recorded in the sales return book.

Statement 2: The seller issues a credit note to the customer when goods are returned.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: The cash book is used to record all cash transactions only.

Statement 2: The purchase book can include both cash and credit purchases.

Show answerHide answer

Correct answer: Option 4 —

Both statements are false.

Q461 Mark

Statement 1: Ledger accounts are prepared after posting transactions from subsidiary books.

Statement 2: The trial balance is prepared before the ledger accounts are balanced.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: Errors in the journal can be rectified by making an entry in the journal proper.

Statement 2: The sales book records all sales transactions, whether cash or credit.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Case Study / Passage Questions3 questions

Q483 Marks

M/s Suri Stores opens a triple-column cash book on 1 April 2024 with cash ₹15000 and bank ₹25000. During the month: Apr 5 cash sales ₹8000; Apr 10 deposits ₹5000 into bank; Apr 15 pays rent ₹3000 by cheque; Apr 22 receives ₹4900 from Hari and allows discount ₹100.

A cash book with cash bank and discount columns is called:

ASingle column

BDouble column

CTriple column

DQuadruple column

A triple-column cash book records discounts:

ADiscount allowed and received

BCash and bank only

CDiscount column on Dr side only

DDiscount on Cr side only

Show the entries in the triple-column cash book.

Show answersHide answers

1. Option 3 — Triple column

2. Option 1 — Discount allowed and received

3. Triple-column cash book has columns: Date | Particulars | L.F. | Discount | Cash | Bank on each side. Receipts (Dr): Apr 1 Balances b/d (Cash 15000, Bank 25000); Apr 5 Sales (Cash 8000); Apr 10 Cash A/c (contra C, Bank 5000); Apr 22 Hari A/c (Discount Allowed 100, Cash 4900). Payments (Cr): Apr 10 Bank A/c (contra C, Cash 5000); Apr 15 Rent A/c (Bank 3000). Closing balances: Cash = 15000+8000+4900−5000 = ₹22900; Bank = 25000+5000−3000 = ₹27000. Total discount allowed ₹100 posted to Discount Allowed A/c at month end.

Q493 Marks

M/s Verma Stores maintains an imprest petty cash of ₹2000 on the first of every month. In April the petty cashier records: postage ₹250, conveyance ₹400, stationery ₹350, refreshments ₹200, courier ₹100. At month end she submits vouchers to the chief cashier.

The imprest system means:

AFixed daily reimbursement

BFixed monthly imprest

CRandom pay-as-you-go

DSingle big disbursement

Total expenses for April are ₹1300. The closing petty cash balance is:

A₹0

B₹700

C₹1300

D₹2000

Explain how the imprest system works and compute the reimbursement.

Show answersHide answers

1. Option 2 — Fixed monthly imprest

2. Option 3 — ₹1300

3. Total April expenses = 250+400+350+200+100 = ₹1300. Closing petty cash = 2000 − 1300 = ₹700. The petty cashier submits vouchers totalling ₹1300; the chief cashier reimburses ₹1300 to restore the imprest to ₹2000 for May. Advantages of imprest: (i) keeps petty expenses tightly controlled; (ii) the petty cash never falls below working level; (iii) vouchers are reviewed at every reimbursement; (iv) chief cashier need not handle each small payment. The petty cash book records each expense and totals are posted to the relevant nominal accounts at period end.

Q503 Marks

Sharma Bros has the following credit sales in January 2024: Jan 4 to Anil 100 books @ ₹200 each less 10% trade discount; Jan 12 to Manju 50 books @ ₹200 each less 10% trade discount; Jan 20 cash sale of 30 books @ ₹200 each.

The sales day book records:

AAll three are recorded

BOnly credit sales are recorded

CAll sales except returns

DCash sales only

The total of January credit sales (after trade discount) entered in the sales day book is:

A₹15000

B₹18000

C₹27000

D₹30000

Prepare the sales day book and show postings.

Show answersHide answers

1. Option 2 — Only credit sales are recorded

2. Option 3 — ₹27000

3. Sales day book records only credit sales of goods (not assets, not cash sales). Computation: (i) Jan 4 Anil — 100×200 = 20000; less 10% TD = 2000; net 18000. (ii) Jan 12 Manju — 50×200 = 10000; less 10% = 1000; net 9000. (iii) Jan 20 cash sale — recorded in cash book, NOT in sales book. Sales day book entries: Jan 4 Anil 18000; Jan 12 Manju 9000. Total credit sales = ₹27000. Posting: each customer A/c debited individually (Anil ₹18000, Manju ₹9000); the total ₹27000 credited to Sales A/c at month end.

Table-Based Questions4 questions

Q513 Marks

Study the subsidiary books and their uses:

Subsidiary book

Records

Posting

Cash book

Cash and bank receipts/payments

Both journal and ledger

Purchases book

Credit purchases of goods

Total to Purchases A/c

Sales book

Credit sales of goods

Total to Sales A/c

Purchases return book

Goods returned to suppliers

Total to Purchases Return A/c

Sales return book

Goods returned by customers

Total to Sales Return A/c

Journal proper

Adjustments and rare entries

Direct to ledger

Cash discounts received are recorded in:

ACash book

BPurchases book

CSales book

DJournal proper

A credit purchase of furniture is recorded in:

APurchases book

BSales book

CJournal proper

DSales return book

Why is the purchase of furniture on credit recorded in the journal proper not in the purchases book?

Show answersHide answers

1. Option 1 — Cash book

2. Option 3 — Journal proper

3. Each subsidiary book is dedicated to a specific kind of transaction so that division of work, speed, and specialisation are achieved. The cash book uniquely serves as both journal (records transactions chronologically) and ledger (gives cash and bank balances). Purchases and sales books record only credit transactions of GOODS — credit purchases of fixed assets (furniture, machinery) go to the journal proper. Returns books capture inward and outward returns. The journal proper is a catch-all for opening, closing, adjusting, rectifying, and unusual entries.

Q523 Marks

Compare types of discounts and their accounting treatment:

Type

Purpose

Accounting treatment

Trade discount

Encourage bulk buying

Deducted from invoice; not in books

Cash discount allowed

Encourage prompt payment

Recorded in cash book/journal

Cash discount received

Reward for early payment

Recorded in cash book/journal

Quantity discount

Volume rebate

Treated like trade discount

Seasonal discount

Clear stocks

Treated like trade discount

Trade discount is:

ARecorded in books

BNot recorded in books

CRecorded only by buyer

DRecorded only by seller

Cash discount given by seller for prompt payment is recorded in the seller's books as:

ADiscount Allowed

BDiscount Received

CSales

DPurchases

Why is trade discount not recorded but cash discount is?

Show answersHide answers

1. Option 2 — Not recorded in books

2. Option 1 — Discount Allowed

3. Trade discount reduces the catalogue price to the wholesale or quantity-buyer price; only the net invoice amount is recorded — the discount itself never appears in the books. Cash discount is offered or received as a reward for early payment; it appears in the books as Discount Allowed (expense) for the seller and Discount Received (income) for the buyer. In a triple-column cash book, both are captured in the discount columns. Trade discount is a price adjustment; cash discount is a financial concession for time value.

Q536 Marks

Prepare a triple-column cash book of M/s Suri Stores from the following entries in April 2024.

Date

Transaction

Amount

Apr 1

Opening cash

₹15000

Apr 1

Opening bank balance

₹25000

Apr 5

Cash sales

₹8000

Apr 10

Deposit into bank

₹5000

Apr 15

Rent paid by cheque

₹3000

Apr 22

Received from Hari (₹100 discount allowed)

₹4900

Q546 Marks

Prepare a Sales Day Book and compute the total credit sales for January 2024 of M/s Sharma Bros.

Date

Customer

Quantity

Rate

Trade Discount

Jan 4

Anil (credit)

100

₹200

10%

Jan 12

Manju (credit)

50

₹200

10%

Jan 20

Cash sale

30

₹200

—

Picture-Based Questions1 question

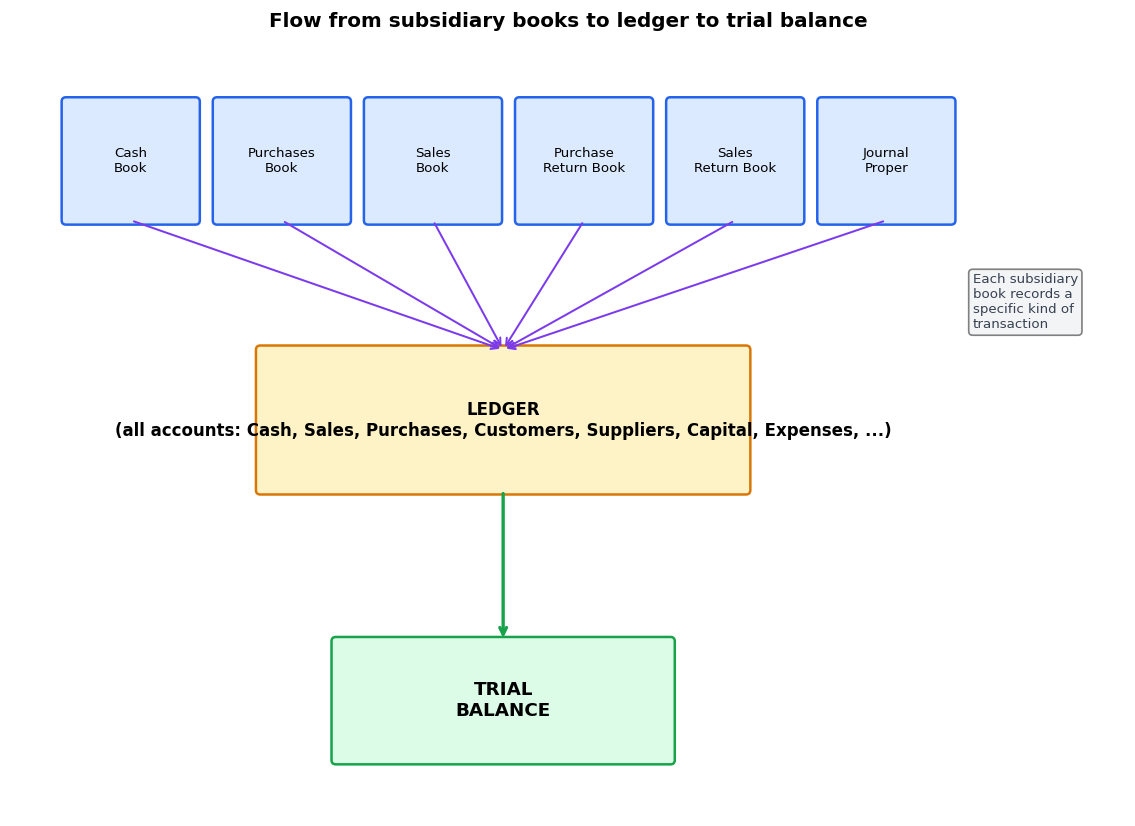

Q553 Marks

Study the flow of subsidiary books to the ledger and answer:

Which subsidiary book records all cash and bank transactions?

ACash book

BPurchases book

CSales book

DJournal proper

A credit purchase of furniture is recorded in:

ACash book

BSales book

CPurchases book

DJournal proper

Explain how subsidiary books reduce work and divide labour.

Show answersHide answers

1. Option 1 — Cash book

2. Option 4 — Journal proper

3. Subsidiary books DIVIDE the recording work among multiple specialised books rather than using one huge journal. Each book records a SPECIFIC kind of transaction: (1) Cash book — all cash and bank receipts/payments; doubles as both journal and ledger. (2) Purchases book — credit purchases of GOODS only (not assets like furniture, which go to journal proper). (3) Sales book — credit sales of goods. (4) Purchases return book — goods returned to suppliers. (5) Sales return book — goods returned by customers. (6) Journal proper — adjustments, opening, closing, rectifying, and rare entries. Each book's totals are posted periodically to the ledger account; the ledger then provides the trial balance. This division enables specialisation, faster posting, and better control.