Trial Balance and Rectification of Errors — Important Questions

55 questions

With answersCBSE format

SUMMARY: This chapter focuses on the preparation of a trial balance and the identification and rectification of errors in accounting records. KEY TOPICS: Trial balance, types of errors, suspense account, error of omission, error of commission, error of principle, compensating errors, rectification of errors, adjusted trial balance, impact of errors on financial statements.

Correct answer: Option 2 — Check arithmetical accuracy of ledger

Q21 Mark

Which of the following errors will NOT affect the agreement of the trial balance?

AError of omission

BError of commission with wrong amount in one account

CError of principle

DBoth 1 and 3

Check answerHide answer

Correct answer: Option 4 — Both 1 and 3

Q31 Mark

A suspense account is opened when:

AThe trial balance does not agree

BThe trial balance agrees

CProfit is too high

DProfit is too low

Check answerHide answer

Correct answer: Option 1 — The trial balance does not agree

Q41 Mark

An error of compensating nature:

AAffects the trial balance

BDoes not affect the trial balance

CDoubles the profit

DNone of these

Check answerHide answer

Correct answer: Option 2 — Does not affect the trial balance

Q51 Mark

Which of the following is an error of principle?

ARecording wages spent on installation as Wages A/c

BPosting purchase to sales

CForgetting to record

DWrong totalling

Check answerHide answer

Correct answer: Option 1 — Recording wages spent on installation as Wages A/c

Q61 Mark

What is the primary purpose of preparing a trial balance?

ATo identify errors in the ledger accounts

BTo calculate the net profit or loss

CTo ensure that total debits equal total credits

DTo prepare financial statements

Check answerHide answer

Correct answer: Option 3 — To ensure that total debits equal total credits

Q71 Mark

Which of the following is an example of an error of omission?

ARecording a transaction in the wrong account

BNot recording a sale transaction at all

CIncorrectly calculating depreciation

DFailing to record an expense

Check answerHide answer

Correct answer: Option 2 — Not recording a sale transaction at all

Q81 Mark

If a transaction is recorded twice in the books, this is known as a:

AError of omission

BError of commission

CError of principle

DCompensating error

Check answerHide answer

Correct answer: Option 2 — Error of commission

Q91 Mark

Which of the following errors will lead to a mismatch in the trial balance?

AError of principle

BError of omission

CError of commission

DAll of the above

Check answerHide answer

Correct answer: Option 4 — All of the above

Q101 Mark

A suspense account is primarily used to:

ARecord all types of errors

BTemporarily hold unclassified transactions

CAdjust the trial balance

DRecord only errors of principle

Check answerHide answer

Correct answer: Option 2 — Temporarily hold unclassified transactions

Q111 Mark

Which of the following statements about adjusted trial balance is correct?

AIt is prepared after rectifying all errors

BIt includes only the errors of omission

CIt is prepared before the financial statements

DIt is not necessary for preparing final accounts

Check answerHide answer

Correct answer: Option 1 — It is prepared after rectifying all errors

Q121 Mark

Compensating errors are defined as:

AErrors that cancel each other out

BErrors that affect the financial statements

CErrors that are recorded in the wrong account

DErrors that are not detected during auditing

Check answerHide answer

Correct answer: Option 1 — Errors that cancel each other out

Q131 Mark

Which error will NOT be revealed by preparing a trial balance?

AError of omission

BError of commission

CError of principle

DError in addition

Check answerHide answer

Correct answer: Option 1 — Error of omission

Q141 Mark

An error of principle occurs when:

AA transaction is recorded incorrectly in the books

BA fundamental accounting principle is violated

CA transaction is omitted from the books

DA transaction is recorded in the wrong period

Check answerHide answer

Correct answer: Option 2 — A fundamental accounting principle is violated

Q151 Mark

Which of the following is NOT a type of error that affects the trial balance?

AError of omission

BError of commission

CError of principle

DError of calculation

Check answerHide answer

Correct answer: Option 4 — Error of calculation

Short Answer Questions10 questions

Q163 Marks

Define a trial balance and state any two of its objectives.

View sample solutionHide solution

A trial balance is a statement prepared on a particular date showing the debit and credit balances of all ledger accounts arranged in two columns (debit total and credit total). Objectives: (i) to check the arithmetical accuracy of postings (debits should equal credits); (ii) to provide a summary basis for preparing the financial statements (P&L Account and Balance Sheet).

Q173 Marks

Explain any three types of errors with one example each.

View sample solutionHide solution

(1) Error of omission — transaction not recorded at all (e.g., goods sold to Mohan ₹500 not entered). (2) Error of commission — recorded but with wrong amount or wrong account (e.g., ₹50 entered as ₹500). (3) Error of principle — wrong classification (e.g., capital expenditure recorded as revenue: cost of installing machinery debited to Wages A/c). Other types: compensating errors, errors of duplication, posting errors.

Q183 Marks

What is a suspense account and when is it closed?

View sample solutionHide solution

A suspense account is a temporary account opened when the trial balance does not agree; the balancing figure is debited or credited to it so that the trial balance can be carried forward. As errors are detected and rectified, the suspense account is reduced. It is closed completely when all errors are located and corrected. If accounts are finalised before all errors are found, the suspense balance is shown on the balance sheet.

Q193 Marks

Distinguish between an error of commission and an error of principle.

View sample solutionHide solution

Error of commission — recording an entry in the right kind of account but with wrong amount or wrong sub-account; example: ₹500 to Ramesh entered as ₹50. Such errors usually affect trial balance agreement. Error of principle — recording in a fundamentally wrong type of account (capital vs revenue, asset vs expense); example: cost of machinery installation recorded as wages expense. Errors of principle do NOT affect trial balance agreement because both debit and credit are made (just in wrong account categories).

Q203 Marks

Why does a trial balance not detect all errors? Give two examples of undetected errors.

View sample solutionHide solution

A trial balance only checks that total debits equal total credits — it cannot detect errors that affect both sides equally or affect neither. Undetected errors: (i) error of omission (no entry made); (ii) error of principle (wrong head but both debit and credit done); (iii) compensating errors (two errors of equal effect cancelling each other); (iv) errors of original entry where same wrong amount is on both sides. Hence trial balance agreement is necessary but not sufficient for accuracy.

Q213 Marks

What is the purpose of preparing a trial balance in accounting?

View sample solutionHide solution

The purpose of preparing a trial balance is to ensure that the total debits equal the total credits in the ledger accounts. It serves as a preliminary check on the accuracy of the bookkeeping processes and helps identify any discrepancies that may exist.

Q223 Marks

Explain the term 'error of omission' with an example.

View sample solutionHide solution

An error of omission occurs when a financial transaction is completely omitted from the accounting records. For example, if a sale of goods worth ₹10,000 is not recorded in the sales account, it represents an error of omission.

Q233 Marks

What is meant by 'adjusted trial balance'?

View sample solutionHide solution

An adjusted trial balance is prepared after all adjustments have been made to the accounts, such as accruals and deferrals. It reflects the updated balances of accounts and is used to prepare financial statements.

Q243 Marks

Describe what compensating errors are in accounting.

View sample solutionHide solution

Compensating errors occur when two or more errors offset each other, resulting in no overall impact on the trial balance. For example, if a purchase is understated by ₹5,000 and a sale is overstated by ₹5,000, the trial balance may still appear correct despite the errors.

Q253 Marks

How can errors impact financial statements?

View sample solutionHide solution

Errors can lead to incorrect financial statements, which can misinform stakeholders about the financial health of a business. For instance, an understatement of expenses can inflate net income, misleading investors and management.

Long Answer Questions6 questions

Q266 Marks

Pass rectification entries for the following errors detected after preparing the trial balance: (i) Goods sold to Ram ₹1500 omitted from sales day book; (ii) Cash ₹500 received from Mohan posted to Mohan's account as ₹50; (iii) ₹2000 paid for installation of machinery debited to Wages A/c; (iv) Total of purchases book overcast by ₹800; (v) Goods returned to Suresh ₹600 not recorded.

View sample solutionHide solution

(i) Ram A/c Dr ₹1500; To Sales A/c ₹1500. (Being credit sale to Ram omitted from books.) (ii) Mohan A/c Dr ₹450; To Suspense A/c ₹450. (Being short credit of ₹450 to Mohan rectified — actual ₹500, recorded ₹50, shortfall ₹450.) (iii) Machinery A/c Dr ₹2000; To Wages A/c ₹2000. (Being installation cost wrongly debited to wages now corrected.) (iv) Suspense A/c Dr ₹800; To Purchases A/c ₹800. (Being purchases overcast rectified.) (v) Suresh A/c Dr ₹600; To Purchases Return A/c ₹600. (Being goods returned to Suresh not recorded.) Errors (i) and (v) are pure omissions and do not affect trial balance; errors (ii) and (iv) needed suspense entries.

Q276 Marks

Explain the methods of preparing a trial balance and their advantages and disadvantages.

View sample solutionHide solution

Three methods of preparing a trial balance: (1) Total Method — list each ledger account showing total debits and credits separately; not commonly used because totals can be unwieldy. Advantage: shows full activity of each account. Disadvantage: trial balance is bulky. (2) Balance Method — list only the closing balance (debit or credit) of each ledger account. Most popular. Advantage: concise; directly fed into financial statements. Disadvantage: agreement does not detect errors where both sides are equally wrong. (3) Total-cum-Balance Method — combination showing both totals and balance for each account in four columns. Advantage: most informative. Disadvantage: bulky, time-consuming. The balance method is normally followed by businesses; many software packages produce trial balances directly from ledger postings.

Q286 Marks

Trial balance does not agree by ₹1500 (debit short). After investigation, the following errors were found: (i) sales day book undercast by ₹500; (ii) wages paid ₹400 was not posted to wages account; (iii) bought goods from Sita ₹600 not entered. Pass rectification entries and prepare suspense account.

View sample solutionHide solution

Rectification entries: (i) Suspense A/c Dr ₹500; To Sales A/c ₹500. (Being sales day book undercast.) (ii) Wages A/c Dr ₹400; To Suspense A/c ₹400. (Being wages not posted earlier.) (iii) Purchases A/c Dr ₹600; To Sita A/c ₹600. (Being purchase from Sita not recorded — error of omission, no suspense involvement.) Suspense Account: Dr side — Cash short b/d ₹1500, To Sales A/c ₹500; Cr side — By Wages A/c ₹400, By Balance c/d ₹1600. The suspense balance of ₹1600 indicates further errors remain to be located.

Q296 Marks

Differentiate between errors that affect and errors that do not affect the trial balance, with examples.

View sample solutionHide solution

Errors affecting trial balance (one-sided errors): only one aspect is incorrect, so debit and credit totals do not match. Examples: (i) wrong totalling of subsidiary book — sales overcast or undercast; (ii) failure to post one side of a transaction; (iii) wrong amount posted on one side only; (iv) wrong balancing of an account. Such errors require a suspense account till rectified. Errors not affecting trial balance (two-sided errors): both debit and credit are equally affected, so totals still match. Examples: (i) error of omission (no entry made); (ii) error of principle (wrong head used); (iii) error of original entry where same wrong amount appears on both sides; (iv) compensating errors. These are harder to detect because the trial balance gives no warning.

Q306 Marks

Explain how rectification entries are passed (a) before preparing trial balance and (b) after preparing trial balance — with one example each.

View sample solutionHide solution

(a) Before preparing trial balance — errors are corrected by passing simple rectification journal entries; suspense account is NOT involved. Example: ₹500 received from Mohan was credited to Sohan's A/c. Rectification: Sohan A/c Dr ₹500; To Mohan A/c ₹500. (b) After preparing trial balance — if the trial balance does not agree, a suspense account is opened. Errors are then rectified by passing journal entries, with one-sided errors involving the suspense account. Example: Total of purchases book undercast by ₹500. Rectification: Purchases A/c Dr ₹500; To Suspense A/c ₹500. Once all errors are detected and rectified, the suspense account closes automatically. If financial statements are prepared with suspense balance still open, that balance appears on the balance sheet pending location of remaining errors.

Q316 Marks

Compare trial balance and balance sheet with the help of a table on five features.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): A trial balance is prepared to verify the arithmetical accuracy of ledger postings.

Reason (R): If total debits equal total credits in the trial balance the postings are arithmetically correct.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): A suspense account is opened when the trial balance does not agree.

Reason (R): The difference is debited or credited to the suspense account so that the trial balance balances temporarily.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): An error of principle does not affect the agreement of the trial balance.

Reason (R): Both debit and credit aspects are recorded in the books although they are recorded under wrong heads of accounts.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): An error of omission of a complete entry is hard to detect.

Reason (R): Since neither debit nor credit was recorded the trial balance still agrees.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Compensating errors are not detected by the trial balance.

Reason (R): Two or more errors cancel out their effects on debit and credit totals.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): A trial balance lists all the debit and credit balances of accounts in the ledger.

Reason (R): The purpose of a trial balance is to ensure that total debits equal total credits, confirming the arithmetical accuracy of the accounts.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): Errors of commission can be easily detected during the preparation of a trial balance.

Reason (R): Errors of commission occur when an entry is made in the wrong account but still affects the trial balance.

Show explanationHide explanation

Correct answer: Option 2 —

Both A and R are true, but R is not the correct explanation of A.

Q391 Mark

Assertion (A): Rectification of errors is necessary only if the trial balance does not agree.

Reason (R): Even if the trial balance agrees, errors may still exist that need rectification for accurate financial statements.

Show explanationHide explanation

Correct answer: Option 3 —

A is true, but R is false.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: The balance method is the most commonly used method.

Statement 2: Balance method shows only the closing debit or credit balance of each account.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Errors of omission do not affect trial balance agreement.

Statement 2: Errors of commission may or may not affect trial balance agreement depending on whether one or both sides are wrong.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: A suspense account closes automatically as errors are rectified.

Statement 2: If errors remain undetected the suspense balance appears on the balance sheet.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Errors detected before preparing trial balance are corrected by simple journal entries.

Statement 2: Errors detected after preparing trial balance may need a suspense account if one-sided.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Errors discovered after preparing financial statements require profit and loss adjustments.

Statement 2: Some errors affect the profit figure and need to be rectified through prior period adjustments.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: A trial balance is prepared to ensure that total debits equal total credits in the ledger accounts.

Statement 2: A trial balance can be used to identify all types of errors in accounting records.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q461 Mark

Statement 1: An error of commission occurs when a transaction is recorded in the wrong account but the correct amount is used.

Statement 2: Errors of principle involve incorrect application of accounting principles.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q471 Mark

Statement 1: A suspense account is used to temporarily hold discrepancies until they are resolved.

Statement 2: The use of a suspense account is only necessary for errors of omission.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Case Study / Passage Questions3 questions

Q483 Marks

On preparing the trial balance Mr Kapur finds the debit total exceeds the credit total by ₹1500. He decides to open a suspense account to balance the trial balance and continue with financial statements. Three errors are later found: (i) sales day book undercast by ₹400; (ii) rent ₹600 paid not posted to rent account; (iii) bought goods from Ram ₹500 not entered.

The suspense account is opened:

ATo balance the trial balance temporarily

BTo find profit

CTo save tax

DTo audit accounts

Which errors will involve a suspense account entry?

AYes — both posted with rectification

BOnly the first two

COnly the third

DAffects no error

Pass rectification entries and prepare the suspense account.

Show answersHide answers

1. Option 1 — To balance the trial balance temporarily

2. Option 2 — Only the first two

3. Rectification entries: (i) Suspense A/c Dr ₹400; To Sales A/c ₹400. (Sales day book undercast — one-sided error so suspense involved.) (ii) Rent A/c Dr ₹600; To Suspense A/c ₹600. (Rent not posted — one-sided.) (iii) Purchases A/c Dr ₹500; To Ram A/c ₹500. (Both sides missed — not a suspense item.) Suspense Account: Dr — Original difference ₹1500, To Sales ₹400; Cr — By Rent ₹600. Closing balance Suspense = 1500 + 400 − 600 = ₹1300 still unaccounted for, indicating more errors. Note: only one-sided errors flow through suspense; two-sided errors (omissions, principle, compensating) do not.

Q493 Marks

After preparing trial balance, M/s Reema Stores discovers: (i) Wages ₹2000 paid for installing a new machine debited to Wages A/c instead of Machinery A/c; (ii) Cash ₹1000 received from Sohan posted to Sohan A/c as ₹100; (iii) Total of purchase return book overcast by ₹300.

The wages on installation error is an error of:

AError of omission

BError of principle

CError of commission

DCompensating

The Sohan posting error is a:

AOne-sided

BTwo-sided

CBoth

DNeither

Pass rectification entries for each error.

Show answersHide answers

1. Option 2 — Error of principle

2. Option 1 — One-sided

3. Rectifications: (i) Machinery A/c Dr ₹2000; To Wages A/c ₹2000. (Wages on installation should be capitalised — error of principle, both sides equally affected, no suspense involved.) (ii) Sohan A/c Dr ₹900; To Suspense A/c ₹900. (Short credit ₹900 — Sohan was credited only ₹100 instead of ₹1000 received, so only one side affected.) (iii) Purchase Return A/c Dr ₹300; To Suspense A/c ₹300. (Overcast purchase return reduced effective debit, so suspense to balance.) These corrections restore both ledgers and trial balance to the proper figures.

Q503 Marks

At year-end M/s Sangam Stores prepares its trial balance with these balances: Capital ₹100000 (Cr); Cash 25000; Bank 35000; Debtors 18000; Creditors 12000; Stock 15000; Furniture 20000; Sales 80000; Purchases 50000; Salaries 8000; Rent 5000; Discount allowed 2000; Discount received 1000; Drawings 3000; Outstanding salary 2000; Closing stock 18000.

The most popular method of preparing trial balance is:

ATotal method

BBalance method

CTotal-cum-balance method

DAll of these

In the trial balance closing stock and outstanding salary appear:

AYes

BNo only some

CNo, all balances are listed

DEither side

Explain trial balance preparation and the role of closing stock/outstanding salary.

Show answersHide answers

1. Option 2 — Balance method

2. Option 3 — No, all balances are listed

3. Trial Balance as on 31 March: Debit side — Cash 25000, Bank 35000, Debtors 18000, Stock (opening) 15000, Furniture 20000, Purchases 50000, Salaries 8000, Rent 5000, Discount allowed 2000, Drawings 3000. Total Dr = ₹181000. Credit side — Capital 100000, Creditors 12000, Sales 80000, Discount received 1000, Outstanding salary 2000 (if shown in trial balance separately). Total Cr = ₹195000. Note: closing stock typically does NOT appear in the trial balance; it is an adjustment given outside. Outstanding salary is the result of an adjustment too — only if these adjustments have already been made would they appear in the trial balance. The agreement of debits and credits suggests no arithmetic errors. The numbers above are illustrative — actual trial balance preparation requires verifying every ledger balance.

Table-Based Questions4 questions

Q513 Marks

Study the types of errors and their effect on trial balance:

Error type

Description

Effect on TB

Omission (full)

Transaction not recorded

No effect

Omission (partial)

One side recorded only

Disagrees

Commission

Wrong amount or wrong account

May or may not

Principle

Wrong head used

No effect

Compensating

Two errors cancel

No effect

Which type definitely causes the trial balance to disagree?

ACompensating

BPrinciple

CPartial omission

DFull omission

A compensating error makes the trial balance:

ADisagree

BAgree

CDoubled

DHalved

Why is trial balance agreement not a guarantee of error-free books?

Show answersHide answers

1. Option 3 — Partial omission

2. Option 2 — Agree

3. Trial balance agreement does not guarantee error-free books — only one-sided errors (partial omissions, one-sided wrong postings, totalling errors) cause disagreement. Two-sided errors (full omissions, principle errors, compensating errors, errors of original entry where same wrong amount is on both sides) leave the totals matching. Hence the trial balance is necessary but not sufficient for accuracy. Auditors and accountants must be vigilant for the silent errors that hide behind a balanced trial balance — typically by reviewing source documents, vouchers, and analytical procedures.

Q523 Marks

Compare methods of preparing trial balance:

Method

Information shown

Use

Total method

Total of debits and credits per account

Detailed; rarely used

Balance method

Closing balance only (Dr or Cr)

Most common; concise

Total-cum-balance

Both totals and balance

Used when both detail and summary needed

The most concise and commonly used method is:

ATotal method

BBalance method

CTotal-cum-balance method

DAll equally

The balance method directly feeds into financial statements.

AYes

BNo

CSometimes

DAlways

Compare the trade-offs of the three trial balance methods.

Show answersHide answers

1. Option 2 — Balance method

2. Option 1 — Yes

3. Each method has trade-offs. Total method shows full activity (debits and credits separately) for each account but is bulky for businesses with many transactions. Balance method shows only the closing balance — concise, easy to use, and directly fed into financial statements. Total-cum-balance method combines both but is the most laborious. In practice, most enterprises use the balance method; software accounting packages (Tally, Zoho) generate it instantly from the ledger. The choice of method affects the size of the trial balance but not the correctness check itself.

Q536 Marks

Prepare a trial balance from the following ledger balances of M/s Sangam Stores as on 31 March 2024.

Account

Dr/Cr

Amount

Capital

Cr

₹100000

Cash

Dr

₹25000

Bank

Dr

₹35000

Debtors

Dr

₹18000

Creditors

Cr

₹12000

Stock (opening)

Dr

₹15000

Furniture

Dr

₹20000

Sales

Cr

₹80000

Purchases

Dr

₹50000

Salaries

Dr

₹8000

Rent

Dr

₹5000

Discount allowed

Dr

₹2000

Discount received

Cr

₹1000

Drawings

Dr

₹3000

Q546 Marks

Pass rectification entries for the errors below detected after preparing the trial balance.

Error

Amount

Sales to Ram omitted from sales book

₹1500

Cash received from Mohan posted as wrong amount

actual ₹500 / posted ₹50

Wages on installation wrongly debited to Wages A/c

₹2000

Total of purchases book overcast

₹800

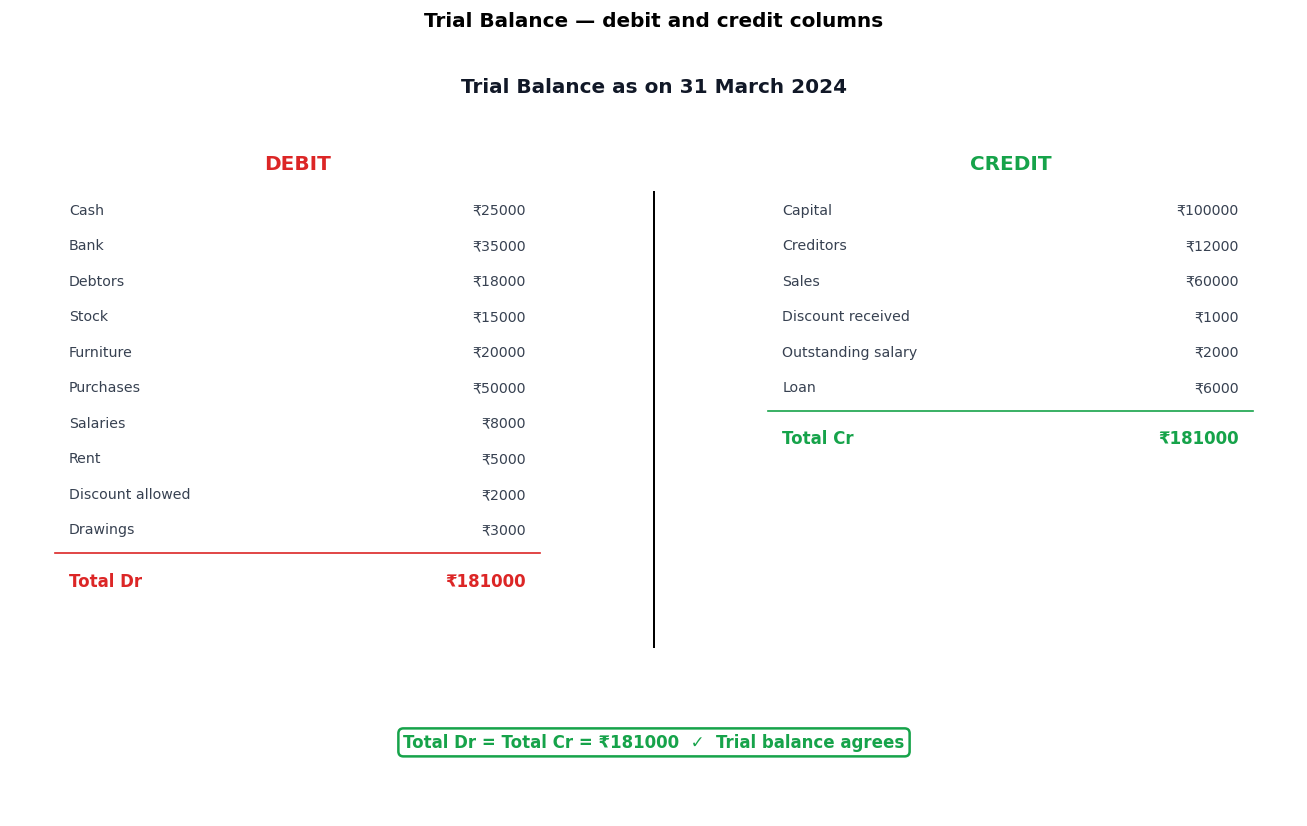

Goods returned to Suresh not recorded

₹600

Picture-Based Questions1 question

Q553 Marks

Study the trial balance T-format and answer:

The main purpose of trial balance is:

ATo find profit

BTo check arithmetical accuracy

CTo pay tax

DTo audit

If totals match, are all errors guaranteed absent?

AAlways

BNever

CSometimes

DOnly with errors

Explain why trial balance agreement is necessary but not sufficient.

Show answersHide answers

1. Option 2 — To check arithmetical accuracy

2. Option 2 — Never

3. A trial balance lists all ledger account balances at a date in two columns — debit and credit — and verifies that their totals match. Equal totals indicate that the books are ARITHMETICALLY balanced — every debit has a corresponding credit. However, agreement of totals does NOT guarantee error-free books because many errors leave both sides equally affected: errors of omission (transaction not recorded), errors of principle (wrong account head used), compensating errors (two errors that cancel), or errors of original entry where the same wrong amount is on both sides. If the totals don't match, the difference is parked in a Suspense Account until the errors are located and rectified. The trial balance is necessary but not sufficient for the books to be correct.