Recording of Transactions - I — Important Questions

55 questions

With answersCBSE format

SUMMARY: This chapter focuses on the fundamental principles and procedures involved in recording financial transactions in the books of accounts. KEY TOPICS: Double-entry system, journal entries, ledger accounts, accounting equations, source documents, vouchers, cash book, subsidiary books, trial balance, accounting cycle.

Which of the following statements about the trial balance is true?

AIt is prepared to check the accuracy of transactions

BIt includes only cash transactions

CIt is prepared at the end of the accounting period only

DIt lists only income and expense accounts

Check answerHide answer

Correct answer: Option 1 — It is prepared to check the accuracy of transactions

Q151 Mark

In a journal entry, the account to be credited is written on which side?

ALeft side

BRight side

CBoth sides

DNeither side

Check answerHide answer

Correct answer: Option 2 — Right side

Short Answer Questions10 questions

Q163 Marks

State the three golden rules of accounting (traditional approach).

View sample solutionHide solution

(1) Personal account — Debit the receiver; Credit the giver. (2) Real account (assets) — Debit what comes in; Credit what goes out. (3) Nominal account (expenses and incomes) — Debit all expenses and losses; Credit all incomes and gains.

Q173 Marks

Show the effect on the accounting equation of the following: (i) Started business with cash ₹100000; (ii) Purchased goods on credit ₹20000.

View sample solutionHide solution

(i) Cash (asset) +₹100000; Capital +₹100000. New equation: 100000 = 0 + 100000. (ii) Stock (asset) +₹20000; Creditors (liability) +₹20000. New equation: 120000 = 20000 + 100000. The equation balances after each transaction.

Q183 Marks

Distinguish between a journal and a ledger.

View sample solutionHide solution

Journal — book of original entry; transactions are recorded chronologically; each entry shows debit and credit accounts; called day book. Ledger — book of secondary entry; transactions from journal are posted account-wise; helps in finding the balance of each account; called the principal book. Journal is the source for the ledger.

Q193 Marks

What is meant by source documents and give two examples.

View sample solutionHide solution

Source documents are the written evidence of a transaction on which book entries are based. They authenticate transactions and provide audit trails. Examples: invoice (supports sale or purchase), receipt (supports cash received), debit note, credit note, cheque counterfoil, pay-in-slip, voucher, bank statement.

Q203 Marks

Explain compound journal entry with one example.

View sample solutionHide solution

A compound journal entry is one where more than two accounts are involved — either multiple debits and one credit or one debit and multiple credits or multiple of both. Example: paid salary ₹10000 and rent ₹5000 by cheque. Salary A/c Dr ₹10000; Rent A/c Dr ₹5000; To Bank A/c ₹15000. (Being salary and rent paid by cheque.) This saves time vs separate entries for each.

Q213 Marks

What is the double-entry system of accounting and why is it important?

View sample solutionHide solution

The double-entry system of accounting is a method where every financial transaction affects at least two accounts, ensuring that the accounting equation (Assets = Liabilities + Equity) remains balanced. This system is important as it provides a complete record of financial transactions and helps in detecting errors and fraud.

Q223 Marks

Define a journal entry and provide an example of a simple transaction recorded as a journal entry.

View sample solutionHide solution

A journal entry is a record of a financial transaction in the accounting books, detailing the accounts affected, the amounts, and whether they are debited or credited. For example, if a business sells goods for ₹5,000 in cash, the journal entry would be: Cash Account Dr. ₹5,000; Sales Account Cr. ₹5,000.

Q233 Marks

What are subsidiary books? Name any two types of subsidiary books.

View sample solutionHide solution

Subsidiary books are specialized accounting books used to record specific types of transactions before they are transferred to the ledger. Two types of subsidiary books are the Purchases Book and the Sales Book.

Q243 Marks

Explain the purpose of a cash book in accounting.

View sample solutionHide solution

A cash book is a financial journal that records all cash receipts and cash payments, including bank deposits and withdrawals. It serves as both a journal and a ledger for cash transactions, helping businesses track their cash flow effectively.

Q253 Marks

What is a trial balance and what is its significance in the accounting cycle?

View sample solutionHide solution

A trial balance is a statement that lists all the balances of the general ledger accounts at a specific point in time. Its significance lies in its ability to verify that total debits equal total credits, ensuring the accuracy of the financial records before preparing financial statements.

Long Answer Questions6 questions

Q266 Marks

Explain the modern (American) approach of classifying accounts and state the rules of debit and credit for each class: assets, liabilities, capital, expenses, and revenue.

View sample solutionHide solution

Modern approach classifies accounts by element of the accounting equation. Five classes: (1) Asset accounts — increase by Debit; decrease by Credit. (2) Liability accounts — increase by Credit; decrease by Debit. (3) Capital accounts — increase by Credit; decrease by Debit. (4) Revenue / Income accounts — increase by Credit; decrease by Debit. (5) Expense / Loss accounts — increase by Debit; decrease by Credit. Memory tip: assets and expenses (left side of the equation) take Debit when increasing; liabilities, capital, and revenues (right side) take Credit when increasing. This approach is logically consistent with the accounting equation Assets = Liabilities + Capital + (Revenues − Expenses).

Q276 Marks

Pass journal entries for the following transactions in the books of Mohan: (i) Started business with cash ₹50000 and goods ₹30000; (ii) Purchased goods from Ram on credit ₹10000; (iii) Sold goods for cash ₹15000 (cost ₹12000); (iv) Paid rent by cheque ₹4000.

View sample solutionHide solution

(i) Cash A/c Dr ₹50000; Purchases A/c (Stock) Dr ₹30000; To Capital A/c ₹80000. (ii) Purchases A/c Dr ₹10000; To Ram A/c ₹10000. (iii) Cash A/c Dr ₹15000; To Sales A/c ₹15000. (iv) Rent A/c Dr ₹4000; To Bank A/c ₹4000. Total debits ₹109000 = total credits ₹109000.

Q286 Marks

Define an accounting voucher and explain its types with examples.

View sample solutionHide solution

An accounting voucher is a written document prepared as evidence of a transaction. Each voucher contains: date, account heads, amount, narration, signature of preparer/authoriser. Types: (1) Cash voucher — for cash receipts and payments (e.g., paid wages ₹2000). (2) Bank voucher — for bank receipts and payments (cheque issue/receipt). (3) Transfer voucher — for non-cash transactions (e.g., depreciation). (4) Journal voucher — for adjustments and rectifications. Vouchers serve as primary evidence, ensure proper authorisation, and provide an audit trail.

Q296 Marks

Show the analysis of the following transactions using the accounting equation: (i) Bought goods ₹20000; (ii) Sold goods for cash ₹15000 (cost ₹10000); (iii) Paid salary ₹3000; (iv) Withdrew cash for personal use ₹5000.

View sample solutionHide solution

Starting equation: Assets = Liabilities + Capital. (i) Stock +₹20000 (asset increase); Cash −₹20000 (asset decrease). Net change: 0 to assets, 0 to capital. (ii) Cash +₹15000; Stock −₹10000; Capital +₹5000 (profit). (iii) Cash −₹3000; Capital −₹3000 (expense reduces capital). (iv) Cash −₹5000; Capital −₹5000 (drawings reduce capital). Each transaction maintains the equation balance.

Q306 Marks

Distinguish between the traditional approach and the modern approach to recording transactions, with an example for each.

View sample solutionHide solution

Traditional approach (English): classifies accounts as personal (related to persons), real (assets), and nominal (expenses, incomes). Three rules of debit and credit. Example: paid salary to Ramesh ₹5000 — Salary A/c (nominal) Dr ₹5000; To Cash A/c (real) ₹5000. Modern approach (American): classifies accounts by element of accounting equation — assets, liabilities, capital, expenses, revenues. Five rules. Example: Salary A/c (expense, increases by debit) Dr ₹5000; To Cash A/c (asset, decreases by credit) ₹5000. The modern approach is more logical and links directly to the accounting equation; traditional is widely used in introductory accounting in India.

Q316 Marks

Compare debit and credit with the help of a table on at least four points.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): Every business transaction affects at least two accounts.

Reason (R): The dual aspect concept ensures that the accounting equation always balances.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): A profit increases the capital of the owner.

Reason (R): Profits earned by the business belong to the owner and are added to capital.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): When goods are sold to Ram on credit Ram's A/c is debited.

Reason (R): Personal accounts are debited when the person receives the benefit.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): The journal is called the book of original entry.

Reason (R): Transactions are first recorded in the journal in chronological order.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Source documents support every entry in the books.

Reason (R): Source documents serve as legal evidence and audit trail of transactions.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): The cash book is used to record all cash transactions.

Reason (R): The cash book serves as both a journal and a ledger for cash transactions.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): A trial balance is prepared to ensure that the total debits equal total credits.

Reason (R): The trial balance helps in detecting errors in the ledger accounts.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q391 Mark

Assertion (A): Every transaction recorded in the journal must have a corresponding entry in the ledger.

Reason (R): The ledger summarizes all transactions for each account.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: Assets always equal liabilities plus capital.

Statement 2: Each transaction maintains the equality of the accounting equation.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Real accounts include all asset accounts.

Statement 2: The rule for real accounts is: debit what comes in credit what goes out.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: A journal entry has at least one debit and one credit.

Statement 2: The total of debits in a journal entry must equal the total of credits.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Salaries paid is a nominal account and is debited.

Statement 2: Expenses and losses are debited; incomes and gains are credited.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Drawings reduce the capital of the owner.

Statement 2: Drawings represent withdrawals by the owner and are not treated as business expenses.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: The double-entry system requires that every transaction be recorded in at least two accounts.

Statement 2: A ledger account summarizes all transactions related to a specific account.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q461 Mark

Statement 1: A source document is not necessary for recording a transaction in the journal.

Statement 2: Vouchers serve as proof of financial transactions.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: The cash book is a subsidiary book that records all cash transactions.

Statement 2: The trial balance is prepared to check the accuracy of the accounting records.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Case Study / Passage Questions3 questions

Q483 Marks

Pooja sets up a stationery shop. On 1 April 2024 she invests cash ₹100000 and a computer ₹40000 (her personal). She buys goods on credit from Stationer Mart ₹50000. She pays rent ₹3000 in cash. She sells goods for ₹25000 on credit to a school.

Stationer Mart's account in Pooja's books is a:

AReal account

BPersonal account

CNominal account

DAll of these

The credit for the opening investment is to:

ACapital A/c

BCash A/c

CComputer A/c

DDrawings A/c

Pass journal entries for Pooja's transactions.

Show answersHide answers

1. Option 2 — Personal account

2. Option 1 — Capital A/c

3. Journal entries on 1 April 2024: (i) Cash A/c Dr ₹100000; Computer A/c Dr ₹40000; To Capital A/c ₹140000. (Being capital introduced as cash and computer.) (ii) Purchases A/c Dr ₹50000; To Stationer Mart A/c ₹50000. (Being goods purchased on credit.) (iii) Rent A/c Dr ₹3000; To Cash A/c ₹3000. (Being rent paid.) (iv) School A/c Dr ₹25000; To Sales A/c ₹25000. (Being sales on credit.) Total debits = total credits. The journal forms the source for ledger postings.

Q493 Marks

Anil runs a hardware shop. Each day he receives several pieces of paper — bills, cheques, receipts, debit notes. He needs to know which document supports which kind of entry.

A cash receipt issued by Anil to a customer paying in cash supports:

ACash memo

BSales invoice

CReceipt

DDebit note

A bill received from a supplier on credit purchase is a:

ASales invoice

BPurchase invoice

CCash memo

DBank pay-in-slip

List the source documents Anil receives and explain what each supports.

Show answersHide answers

1. Option 3 — Receipt

2. Option 2 — Purchase invoice

3. Source documents authenticate every entry: (1) Cash memo — issued for a cash sale; entered in cash book and sales account. (2) Invoice (sales/purchase) — for credit transactions; supports debtor/creditor entries. (3) Receipt — acknowledges money received; supports cash book entry. (4) Debit note — issued by buyer when returning goods; supports purchase return. (5) Credit note — issued by seller when goods returned; supports sales return. (6) Cheque counterfoil and pay-in-slip — bank transactions. (7) Voucher — internal authorisation for journal entries. Anil should file each document in chronological order and number it for easy retrieval.

Q503 Marks

Mr Nair starts a business with cash ₹200000 (capital). He buys furniture for ₹40000 cash and goods on credit for ₹60000. He sells goods worth ₹30000 (cost) for ₹40000 cash (profit ₹10000). He pays rent ₹5000 cash.

After all transactions the capital figure:

AStays the same

BIncreases by profit

CDecreases by expense

DBoth 2 and 3

Selling goods for cash affects:

ACash A/c

BSales A/c

CCapital A/c

DBoth 1 and 2

Show the effect of each transaction on the accounting equation.

Show answersHide answers

1. Option 4 — Both 2 and 3

2. Option 4 — Both 1 and 2

3. Track each transaction's effect: Start: Cash 200000 = Capital 200000. (1) Buy furniture: Cash −40000, Furniture +40000. Equation: (Cash 160000 + Furniture 40000) = Capital 200000. (2) Goods on credit: Stock +60000, Creditors +60000. Equation: (Cash 160000 + Furniture 40000 + Stock 60000) = Creditors 60000 + Capital 200000. (3) Sale of goods: Cash +40000, Stock −30000, Capital +10000 (profit). New equation: (Cash 200000 + Furniture 40000 + Stock 30000) = Creditors 60000 + Capital 210000. (4) Rent paid: Cash −5000, Capital −5000. Final: (Cash 195000 + Furniture 40000 + Stock 30000) = Creditors 60000 + Capital 205000. Both sides total ₹265000.

Table-Based Questions4 questions

Q513 Marks

Study the rules of debit and credit (modern approach):

Account type

Increase

Decrease

Asset

Debit

Credit

Liability

Credit

Debit

Capital (Owner's Equity)

Credit

Debit

Expense / Loss

Debit

Credit

Revenue / Income

Credit

Debit

An increase in the Cash A/c (an asset) is recorded as:

ADebit

BCredit

CEither

DNeither

A decrease in capital is recorded as:

ADebit

BCredit

CEither

DNeither

Why is the modern approach considered more logical than the traditional?

Show answersHide answers

1. Option 1 — Debit

2. Option 1 — Debit

3. The modern approach is logical because it derives directly from the accounting equation Assets = Liabilities + Capital + Revenues − Expenses. Items on the LEFT of the equation (Assets, Expenses) increase by Debit; items on the RIGHT (Liabilities, Capital, Revenues) increase by Credit. Decreases follow the opposite side. Memory shortcut: A-E debit increase, L-C-R credit increase. This approach replaces the traditional 3-rule classification (personal/real/nominal) with 5 rules but is more consistent and is widely used in modern textbooks.

Q523 Marks

Study common journal entries and their effects:

Transaction

Debit

Credit

Cash sale ₹5000

Cash A/c

Sales A/c

Credit purchase ₹3000

Purchases A/c

Supplier A/c

Salary paid ₹2000

Salary A/c

Cash/Bank A/c

Drawings ₹1000

Drawings A/c

Cash A/c

Asset bought on credit

Asset A/c

Vendor A/c

For a cash sale of ₹5000 the credit account is:

ACash

BSales

CCapital

DDrawings

When a fixed asset is bought on credit the credit goes to:

AAsset A/c

BCash A/c

CVendor A/c

DCapital A/c

Explain the dual aspect by tracing the entries in the table.

Show answersHide answers

1. Option 2 — Sales

2. Option 3 — Vendor A/c

3. Each transaction has a giving and receiving side. (1) Cash sale — cash comes in (debit), revenue earned (credit Sales). (2) Credit purchase — goods come in (debit Purchases), liability to supplier increases (credit). (3) Salary paid — expense incurred (debit Salary), cash decreases (credit). (4) Drawings — owner takes from business (debit Drawings, which reduces capital), cash decreases (credit). (5) Asset on credit — asset increases (debit), liability increases (credit). Once the rules are mastered, posting any transaction becomes routine.

Q536 Marks

Show the effect of each transaction on the accounting equation and verify that it remains balanced after each step.

Transaction

Effect on Asset

Effect on Liability

Effect on Capital

Started with Cash ₹100000

+100000

0

+100000

Bought goods on credit ₹30000

+30000

+30000

0

Cash sale ₹20000 (cost ₹15000)

+5000 (net)

0

+5000

Paid salary ₹2000

-2000

0

-2000

Drawings ₹3000

-3000

0

-3000

Q546 Marks

Pass journal entries for the following transactions of M/s Sangam Stores in April 2024.

Date

Transaction

Amount

Apr 1

Started business with cash

₹50000

Apr 5

Bought goods from Ram on credit

₹20000

Apr 10

Sold goods for cash

₹15000

Apr 15

Paid rent in cash

₹3000

Apr 20

Drew cash for personal use

₹2000

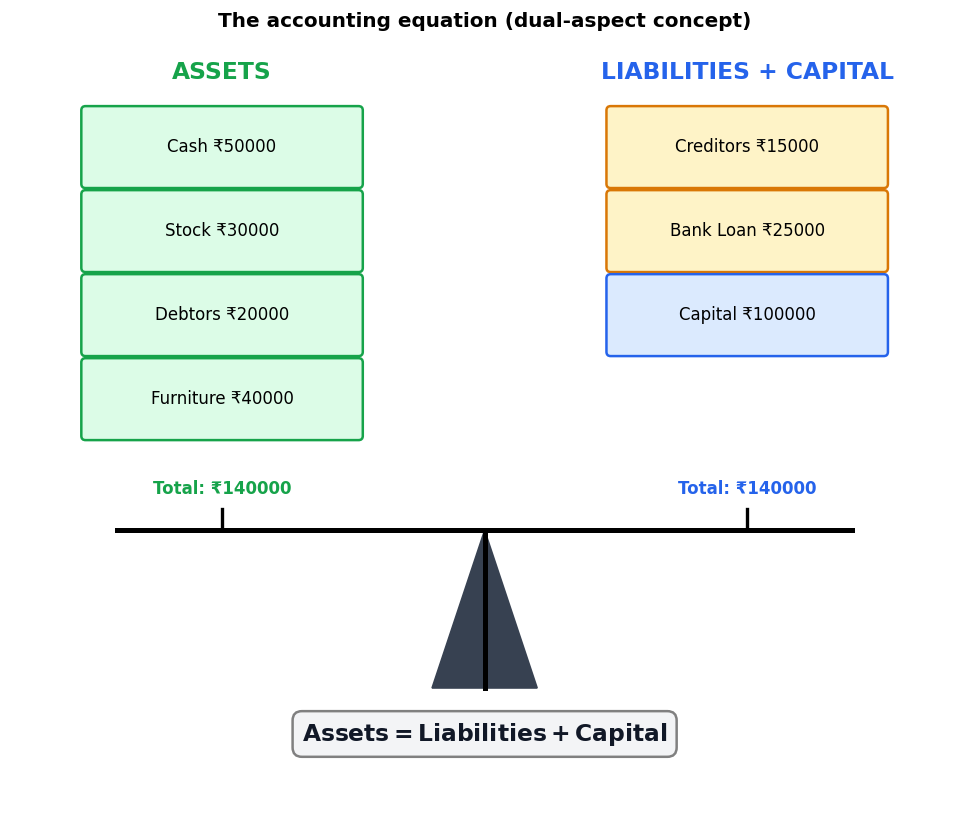

Picture-Based Questions1 question

Q553 Marks

Study the accounting-equation balance scale and answer:

The accounting equation is:

AAssets = Liabilities + Capital

BAssets = Capital − Liabilities

CCapital = Assets + Liabilities

DLiabilities = Assets + Capital

The balance is maintained because of which concept?

ASingle aspect

BDual aspect

CGoing concern

DCost concept

Explain how each transaction maintains the accounting equation.

Show answersHide answers

1. Option 1 — Assets = Liabilities + Capital

2. Option 2 — Dual aspect

3. The accounting equation Assets = Liabilities + Capital reflects the dual-aspect concept: every transaction has two equal effects — what the business OWNS (assets) must equal what it OWES to outsiders (liabilities) plus what is owed to the owner (capital). When the owner introduces ₹100000 cash, both Cash (asset) and Capital (owner's equity) increase by ₹100000. When goods are bought on credit, Stock (asset) and Creditors (liability) both increase. When goods are sold for profit, Cash (asset) increases more than Stock (asset) decreases, and Capital increases by the profit. Drawings reduce both Cash and Capital. The equation must always balance — if it doesn't, an error has been made. This is the foundation of double-entry book-keeping.