SUMMARY: The chapter "Introduction to Accounting" provides an overview of the fundamental concepts and objectives of accounting, its role in business, and the basic principles that govern accounting practices. KEY TOPICS: definition of accounting, objectives of accounting, functions of accounting, users of accounting information, branches of accounting, basic accounting terms, accounting principles, accounting standards, importance of accounting, limitations of accounting

BTo provide a systematic record of financial transactions

CTo manage employee performance

DTo enhance customer satisfaction

Check answerHide answer

Correct answer: Option 2 — To provide a systematic record of financial transactions

Q141 Mark

Which accounting term refers to the difference between total assets and total liabilities?

ARevenue

BEquity

CExpense

DProfit

Check answerHide answer

Correct answer: Option 2 — Equity

Q151 Mark

In which branch of accounting would you find budgeting and performance evaluation?

AFinancial Accounting

BCost Accounting

CManagement Accounting

DTax Accounting

Check answerHide answer

Correct answer: Option 3 — Management Accounting

Short Answer Questions10 questions

Q163 Marks

Define accounting and state any two of its objectives.

View sample solutionHide solution

Accounting is the process of identifying, measuring, recording, classifying, summarizing, analyzing and communicating financial information to users for decision making. Two objectives: (i) Maintaining systematic records of all financial transactions; (ii) Ascertaining the profit/loss and financial position of the business at the end of a period.

Q173 Marks

Distinguish between book-keeping and accounting.

View sample solutionHide solution

Book-keeping is the routine recording and classifying of financial transactions in journals and ledgers. Accounting is broader: it includes book-keeping plus summarising (trial balance, financial statements), analysing, interpreting and communicating the results to users. Book-keeping is a subset of accounting.

Q183 Marks

List any three users of accounting information and state their information needs.

View sample solutionHide solution

(i) Owners/shareholders — want profitability and return on investment. (ii) Lenders/creditors — want solvency and ability to repay debt. (iii) Government/tax authorities — want correct tax liability. Other users include employees (job security and bonuses), customers (continuity of supply), and management (planning and control).

Q193 Marks

State any three qualitative characteristics that accounting information should possess.

View sample solutionHide solution

(i) Reliability: information must be free from material error and bias. (ii) Relevance: must be useful for decision-making (timely and capable of influencing decisions). (iii) Understandability: presented in a form that users can comprehend. (Comparability and consistency are also qualitative characteristics.)

Q203 Marks

Differentiate between financial accounting and management accounting.

View sample solutionHide solution

Financial accounting prepares standardised financial statements (P&L, Balance Sheet) for external users; mandatory; based on past data; follows GAAP. Management accounting prepares customised reports for internal managers; voluntary; future-oriented; uses any technique that aids decisions.

Q213 Marks

What are the primary functions of accounting?

View sample solutionHide solution

The primary functions of accounting include recording financial transactions, classifying and summarizing financial data, and interpreting financial information to assist in decision-making.

Q223 Marks

Explain the importance of accounting in business decision-making.

View sample solutionHide solution

Accounting provides critical financial information that helps stakeholders make informed decisions regarding resource allocation, performance evaluation, and strategic planning.

Q233 Marks

What are the branches of accounting? Name at least two.

View sample solutionHide solution

The branches of accounting include financial accounting, management accounting, cost accounting, and tax accounting. Financial accounting focuses on reporting financial information to external users, while management accounting aids internal decision-making.

Q243 Marks

Define the term 'accounting standards'. Why are they important?

View sample solutionHide solution

Accounting standards are formal guidelines that dictate how financial transactions and events should be reported in financial statements. They ensure consistency, comparability, and transparency in financial reporting.

Q253 Marks

What is the role of accounting information for investors?

View sample solutionHide solution

Investors use accounting information to assess the financial health and performance of a business, enabling them to make informed decisions about buying, holding, or selling shares.

Long Answer Questions6 questions

Q266 Marks

Explain the meaning and process of accounting and discuss its role in modern business.

View sample solutionHide solution

Accounting is the process by which financial information is identified, recorded, classified, summarised, analysed and communicated. The process flow: identify a transaction → record in journal → post to ledger → balance the ledger → prepare trial balance → prepare financial statements → analyse and interpret → communicate to users. Roles in modern business: (1) Maintains systematic records — replaces memory; (2) Ascertains profit or loss through P&L Account; (3) Ascertains financial position through Balance Sheet; (4) Provides information for tax authorities and statutory compliance; (5) Helps in decision-making through cost and management accounting; (6) Builds investor and creditor confidence; (7) Acts as legal evidence in disputes. Without accounting, no large enterprise could function — modern accounting is the language of business.

Q276 Marks

Discuss the various branches of accounting with examples of the kind of information each provides.

View sample solutionHide solution

(1) Financial accounting — recording and reporting of past transactions; produces P&L Account, Balance Sheet, Cash Flow Statement for owners, creditors, government. (2) Cost accounting — ascertaining cost of products and services; useful for pricing decisions and cost control. (3) Management accounting — providing customised information for managers; uses budgets, variance analysis, ratio analysis for planning and control. (4) Tax accounting — preparing tax computations and filing returns under income-tax and GST laws. (5) Social responsibility accounting — measuring social and environmental impact (e.g., carbon footprint). (6) Human resource accounting — valuing the workforce as a corporate asset. Each branch serves a different decision-maker and uses different techniques.

Q286 Marks

Explain the qualitative characteristics of accounting information: relevance, reliability, comparability, and understandability.

View sample solutionHide solution

(1) Relevance — information must influence the decisions of users; must be timely and capable of altering judgements. Irrelevant information clutters reports. (2) Reliability — information must be free from material errors and bias; should faithfully represent the transactions. Achieved through verifiability and prudence. (3) Comparability — users should be able to compare the financial information of an enterprise across periods (intra-period) and with other enterprises (inter-period). Requires consistency in accounting policies. (4) Understandability — information must be presented in a form that users with reasonable knowledge of business and accounting can comprehend. Together these characteristics ensure that accounting information is useful for decision-making.

Q296 Marks

Discuss the limitations of financial accounting that have led to the development of other branches of accounting.

View sample solutionHide solution

(1) Records only monetary transactions — qualitative factors (employee morale, customer goodwill) are excluded. (2) Records past events only — does not provide forward-looking information for planning. (3) Uses historical cost — ignores price-level changes and current values. (4) Aggregated information — does not show product-wise or department-wise profitability. (5) Window dressing possible — manipulation of accounting policies can mislead. (6) Subjective judgements — depreciation methods, inventory valuation involve choice. These limitations led to: cost accounting (product-wise costs), management accounting (forward-looking information for managers), responsibility accounting (department-wise control), inflation accounting (price-level adjustments), and human resource accounting (people as assets).

Q306 Marks

What is meant by the qualitative characteristics of accounting information? Explain in brief, indicating their interrelationships.

View sample solutionHide solution

Qualitative characteristics are attributes that make accounting information useful to users. The four primary characteristics are reliability, relevance, comparability, and understandability. Reliability and relevance can sometimes conflict — fully verified information may be too late to be relevant; timely estimates may be less reliable. Comparability requires consistency in policies; if a change is needed for greater relevance, it should be disclosed. Understandability puts a duty on the preparer to present information clearly and on the user to have reasonable accounting knowledge. Together, these characteristics ensure that financial reports are decision-useful.

Q316 Marks

Differentiate between book-keeping and accounting in tabular form on five points.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): Accounting is referred to as the language of business.

Reason (R): Accounting communicates the results of business operations to users in monetary terms.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Book-keeping is part of accounting.

Reason (R): Book-keeping is concerned only with the recording phase of accounting.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): Management accounting reports are not prepared in any prescribed format.

Reason (R): Management accounting is meant for internal use and is not regulated by external standards.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Investors are interested in the profitability of an enterprise.

Reason (R): Investors decide on continuing or withdrawing investment based on the return earned by the enterprise.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Accounting information must be reliable.

Reason (R): Reliability ensures that information is free from material error and faithfully represents the transactions.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): Accounting helps in making informed business decisions.

Reason (R): It provides financial information that is essential for planning and control.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): The primary objective of accounting is to record financial transactions.

Reason (R): This helps in maintaining a systematic record of all business activities.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q391 Mark

Assertion (A): Users of accounting information include only internal stakeholders.

Reason (R): External stakeholders such as investors and creditors also rely on accounting information.

Show explanationHide explanation

Correct answer: Option 3 —

A is true, but R is false.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: Accounting is the process of recording financial transactions.

Statement 2: Accounting is also concerned with summarizing and communicating financial information.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Cost accounting helps in determining product costs.

Statement 2: Tax accounting helps in computing tax liability under different tax laws.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Financial accounting reports the past performance of the business.

Statement 2: Financial accounting prepares the P&L Account and Balance Sheet for external users.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Owners and managers are internal users of accounting information.

Statement 2: Internal users rely on detailed and customised accounting reports for decision-making.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Accounting helps in ascertaining profits or losses of a business.

Statement 2: Accounting also assists in ascertaining the financial position through the Balance Sheet.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: Accounting is primarily concerned with the recording of financial transactions.

Statement 2: The main objective of accounting is to provide information for decision-making.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q461 Mark

Statement 1: Users of accounting information include only external parties such as investors and creditors.

Statement 2: Accounting helps in maintaining systematic records of financial transactions.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: Branches of accounting include financial accounting, management accounting, and tax accounting.

Statement 2: Accounting standards are optional guidelines that can be ignored by businesses.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Case Study / Passage Questions3 questions

Q483 Marks

Sundar starts a small grocery store on 1 April 2024 with cash ₹50000 and a delivery cycle worth ₹8000 brought from home. In the first month he buys goods worth ₹30000 (paid ₹20000 cash, ₹10000 on credit) and sells goods for ₹25000 cash. He pays rent ₹3000 and salary ₹2000.

The journal in which Sundar first records each transaction is called:

AProfit-only book

BA book of original entry

CThe trial balance

DA trial run

To know what Sundar's business owns and owes at the end of the month he should prepare a:

ATrading account

BProfit and loss account

CBalance sheet

DCash book

Explain how accounting will help Sundar manage his grocery business better.

Show answersHide answers

1. Option 2 — A book of original entry

2. Option 3 — Balance sheet

3. Accounting helps Sundar by (i) maintaining systematic records of every transaction so nothing is forgotten; (ii) ascertaining profit or loss for the month through a P&L Account; (iii) ascertaining financial position through a Balance Sheet showing assets (cash, stock, cycle, debtors) and liabilities (creditors, capital); (iv) helping him compute taxes; (v) demonstrating creditworthiness to banks if he ever needs a loan; (vi) acting as legal evidence in case of disputes. Without accounting Sundar would rely on memory which is unreliable as the business grows.

Q493 Marks

Maple Public School is moving from a manual accounting register kept by the cashier to a computerised system. The principal wants to know who the users of the school's accounting information will be and what each user will look for.

Accounting information of the school will be used by:

AInternal users only

BExternal users only

CBoth internal and external users

DNo users at all

Which of the following will the principal want the system to track?

AIncome from fees

BSalaries paid

CBuildings owned

DAll of these

Identify the various users of the school's accounting information and what each will look for.

Show answersHide answers

1. Option 3 — Both internal and external users

2. Option 4 — All of these

3. Internal users include the principal, governing body, teachers, and finance officer who use detailed reports for budgeting, decision-making, and control. External users include parents (interested in financial soundness and fee utilisation), donors and CSR partners (interested in expense reporting), banks (for any loans), and government regulators (for grants and tax compliance). The school management would want monthly fee collection reports, expense breakdowns by category, and balance sheet showing buildings, equipment, and reserves. Accounting software supports all these reports automatically.

Q503 Marks

Anita runs a corner bookshop. She maintains a simple cash book and stock register but no formal ledgers or financial statements. Her CA tells her she should adopt full double-entry book-keeping. She is unsure whether the additional effort is worthwhile.

The CA explains the relationship between bookkeeping and accounting:

ABookkeeping is the same as accounting

BBookkeeping is part of accounting

CAccounting is part of bookkeeping

DNeither is related

Adopting full accounting will help Anita because:

ATrial balance can be prepared

BErrors are easier to detect

CProfit and financial position can be ascertained

DAll of these

Should Anita adopt full accounting? Explain.

Show answersHide answers

1. Option 2 — Bookkeeping is part of accounting

2. Option 4 — All of these

3. Anita should adopt full accounting because: (i) it gives a true and fair view of the bookshop's profit and financial position rather than just cash flows; (ii) it allows preparation of a trial balance that catches arithmetic errors; (iii) tax authorities and banks expect proper books; (iv) it helps her compare year-on-year performance; (v) it provides legal evidence in disputes. The additional effort is small once a routine is established and modern accounting software (Tally, Zoho Books) automates most of the work — the benefits far outweigh the cost.

Table-Based Questions3 questions

Q513 Marks

Study the branches of accounting and their main users:

Branch

Main user

Information provided

Financial accounting

External (investors, creditors, govt.)

P&L Account, Balance Sheet, Cash Flow

Cost accounting

Production manager

Cost per unit, variance reports

Management accounting

Top management

Forecasts, budgets, ratio analysis

Tax accounting

Tax authorities

Tax computations and returns

Social accounting

Public, NGOs

CSR and environmental impact reports

Which branch produces P&L Account and Balance Sheet for external users?

ACost accounting

BFinancial accounting

CManagement accounting

DTax accounting

Budgets and forecasts are typically the output of:

ACost accounting

BTax accounting

CManagement accounting

DSocial accounting

Why does a modern enterprise need more than one branch of accounting?

Show answersHide answers

1. Option 2 — Financial accounting

2. Option 3 — Management accounting

3. Each branch of accounting serves a different decision-maker. Financial accounting serves external users with standardised statements. Cost accounting helps production managers control unit costs. Management accounting provides forward-looking information for internal decisions. Tax accounting handles compliance with tax laws. Social/responsibility accounting reports on the firm's impact on society. A modern enterprise typically maintains several of these in parallel — one accounts department but multiple report types feeding different audiences.

Q523 Marks

Compare the qualitative characteristics of accounting information:

Characteristic

Definition

Practical example

Reliability

Free from bias and material error

Audited statements

Relevance

Influences user's decision

Quarterly results before AGM

Comparability

Comparable across periods/firms

Same format in P&L year-on-year

Understandability

Comprehensible to users

Plain-language disclosures

Using the same format of P&L every year reflects:

AReliability

BRelevance

CComparability

DUnderstandability

Quarterly results published just before the AGM illustrate:

AReliability

BMateriality

CRelevance

DUnderstandability

Discuss conflicts among reliability, relevance and comparability.

Show answersHide answers

1. Option 3 — Comparability

2. Option 3 — Relevance

3. Sometimes characteristics conflict — for example, fully audited information may be late and lose relevance, while fast estimates may sacrifice reliability. Comparability requires consistency in policies; if a change is needed for greater relevance, it must be disclosed. Understandability puts a duty on the preparer to present information clearly and on the user to have reasonable accounting knowledge. Together these characteristics ensure that financial reports are useful for decision-making.

Q536 Marks

Match each user of accounting information with the kind of information they primarily need.

User

Information needed

Investor

? (return on investment)

Lender / Bank

? (solvency, repayment ability)

Government

? (tax compliance)

Employees

? (job security, bonus)

Customers

? (continuity of supply)

Picture-Based Questions1 question

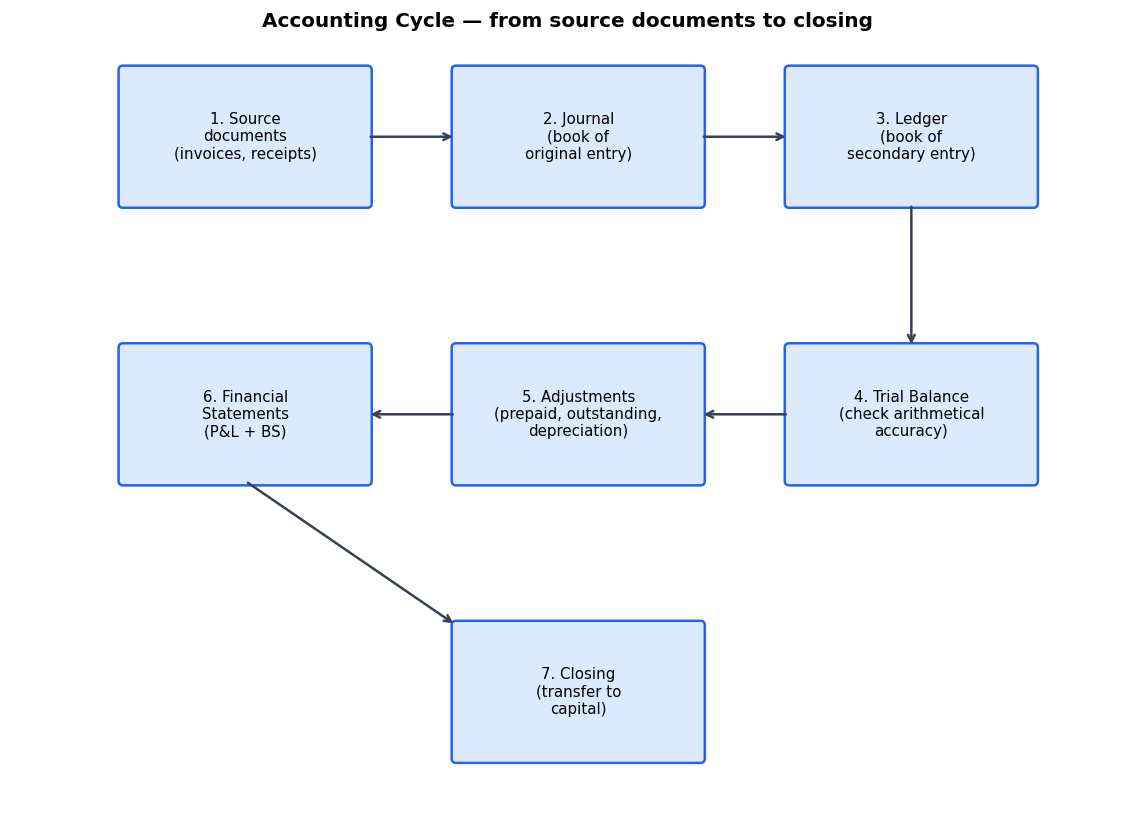

Q543 Marks

Study the accounting cycle flowchart and answer:

The first step of the accounting cycle is:

ASource documents

BTrial balance

CFinancial statements

DClosing entries

Step 4 in the cycle (after the ledger) is:

ATrial balance

BAdjustments

CFinancial statements

DClosing

Describe each step of the accounting cycle.

Show answersHide answers

1. Option 1 — Source documents

2. Option 1 — Trial balance

3. The accounting cycle is the sequence of steps an accountant follows from raw transactions to final financial statements: (1) Source documents — bills, vouchers, receipts authenticate every transaction. (2) Journal — book of original entry; each transaction recorded chronologically with debit and credit. (3) Ledger — book of secondary entry; transactions from journal posted account-wise. (4) Trial balance — checks arithmetical accuracy of ledger postings. (5) Adjustments — accruals, prepayments, depreciation, provisions are passed at year-end. (6) Financial statements — Trading + P&L Account and Balance Sheet prepared. (7) Closing — nominal accounts closed and net profit transferred to capital. The cycle repeats every accounting period.