SUMMARY: This chapter introduces the preparation and presentation of financial statements for sole proprietorship businesses. KEY TOPICS: financial statements, trading account, profit and loss account, balance sheet, capital account, liabilities, assets, revenue, expenses, adjustments in final accounts

Correct answer: Option 3 — In both trading account and balance sheet

Q31 Mark

Wages paid for installing machinery should be shown in:

AWages A/c

BProfit and Loss Account

CCapital A/c

DMachinery A/c

Check answerHide answer

Correct answer: Option 4 — Machinery A/c

Q41 Mark

The order in which assets are arranged in the balance sheet is:

APermanence or liquidity

BAlphabetical

CRandom

DNumerical

Check answerHide answer

Correct answer: Option 1 — Permanence or liquidity

Q51 Mark

Goodwill is classified as:

ATangible asset

BIntangible asset

CCurrent asset

DLiability

Check answerHide answer

Correct answer: Option 2 — Intangible asset

Q61 Mark

Which of the following is not a component of the Profit and Loss Account?

ARevenue from Operations

BCost of Goods Sold

CDrawings

DOperating Expenses

Check answerHide answer

Correct answer: Option 3 — Drawings

Q71 Mark

In the Balance Sheet, which of the following is classified as a current liability?

ADebentures

BBank Overdraft

CLand and Building

DLong-term Loans

Check answerHide answer

Correct answer: Option 2 — Bank Overdraft

Q81 Mark

Which account is prepared to determine the gross profit or loss of a business?

AProfit and Loss Account

BBalance Sheet

CTrading Account

DCapital Account

Check answerHide answer

Correct answer: Option 3 — Trading Account

Q91 Mark

What is the primary purpose of the Balance Sheet?

ATo show the profitability of the business

BTo present the financial position of the business

CTo calculate the gross profit

DTo summarize cash flows

Check answerHide answer

Correct answer: Option 2 — To present the financial position of the business

Q101 Mark

Which of the following adjustments is made in the Profit and Loss Account?

ADepreciation on Fixed Assets

BClosing Stock

CDrawings

DCapital Introduced

Check answerHide answer

Correct answer: Option 1 — Depreciation on Fixed Assets

Q111 Mark

Which of the following items is shown on the liabilities side of the Balance Sheet?

AStock

BCash in Hand

CCreditors

DDebtors

Check answerHide answer

Correct answer: Option 3 — Creditors

Q121 Mark

The net profit or loss is transferred to which account at the end of the accounting period?

ACapital Account

BDrawings Account

CTrading Account

DLiabilities Account

Check answerHide answer

Correct answer: Option 1 — Capital Account

Q131 Mark

Which of the following is considered an expense while preparing the Profit and Loss Account?

ASales Revenue

BPurchases of Goods

COwner's Capital

DDrawings

Check answerHide answer

Correct answer: Option 2 — Purchases of Goods

Q141 Mark

What does the term 'Drawings' refer to in the context of a sole proprietorship?

AInvestments made by the owner

BWithdrawals made by the owner for personal use

CProfits retained in the business

DLiabilities incurred by the business

Check answerHide answer

Correct answer: Option 2 — Withdrawals made by the owner for personal use

Q151 Mark

Which of the following is an example of a fixed asset?

AInventory

BAccounts Receivable

CMachinery

DBank Balance

Check answerHide answer

Correct answer: Option 3 — Machinery

Short Answer Questions10 questions

Q163 Marks

Distinguish between trading account and profit and loss account.

View sample solutionHide solution

Trading account computes the gross profit (or loss) by comparing net sales with cost of goods sold. It includes only direct expenses related to production/purchase of goods (purchases, wages, freight inwards, carriage on purchases). Profit and Loss account starts with gross profit (or loss) and computes net profit by deducting all indirect/operating expenses (salaries, rent, advertising) and adding other incomes. Trading account precedes the P&L account in the financial statements.

Q173 Marks

What is the difference between revenue expenditure and capital expenditure?

View sample solutionHide solution

Revenue expenditure is incurred for day-to-day operations and yields benefits within the current accounting period; charged to P&L Account; example: rent paid, repairs, salaries. Capital expenditure is for acquiring fixed assets or improving them; benefits extend over multiple years; capitalised on balance sheet; example: purchase of machinery, building extension. Misclassifying these is an error of principle.

Q183 Marks

Define balance sheet and state its main purpose.

View sample solutionHide solution

A balance sheet is a statement of assets and liabilities of a business at a particular date. Its purpose: (i) shows the financial position of the business — what is owned (assets) and what is owed (liabilities and capital); (ii) helps users assess solvency, liquidity, and capital structure; (iii) provides basis for borrowing and investment decisions. The balance sheet must always satisfy: Total Assets = Total Liabilities + Capital.

Q193 Marks

List any three direct expenses charged to trading account.

View sample solutionHide solution

(i) Wages — paid to factory workers directly involved in production. (ii) Carriage inwards / freight on purchases — cost of bringing goods to the business location. (iii) Customs duty / import duty on imported goods. (iv) Power and fuel consumed in factory. (v) Manufacturing expenses, packing, and storage of raw materials.

Q203 Marks

Explain the matching principle and its application in preparing financial statements.

View sample solutionHide solution

The matching principle requires that expenses be matched with the revenues they helped earn during the same accounting period. Application: (i) cost of goods sold matched with sales (not goods unsold); (ii) salaries, rent, depreciation, and other expenses for the period are charged even if cash is paid in another period; (iii) prepaid expenses are excluded; outstanding expenses are added. This principle ensures the P&L account reflects true profit, not just cash flows.

Q213 Marks

What is a trading account and what information does it provide?

View sample solutionHide solution

A trading account is a financial statement that summarizes the direct costs and revenues associated with the sale of goods during a specific period. It provides information on gross profit or loss by comparing sales revenue with the cost of goods sold.

Q223 Marks

Explain the purpose of the profit and loss account in financial statements.

View sample solutionHide solution

The profit and loss account summarizes the revenues and expenses of a business over a particular period, showing the net profit or loss. Its purpose is to provide insights into the operational efficiency and profitability of the business.

Q233 Marks

What are liabilities in the context of a balance sheet?

View sample solutionHide solution

Liabilities are obligations that a business owes to external parties, which can include loans, accounts payable, and other debts. They are classified as current or non-current based on their due dates.

Q243 Marks

Define capital account and its significance in financial statements.

View sample solutionHide solution

The capital account reflects the owner's equity in the business, including the initial investment and retained earnings. It is significant as it shows the net worth of the business and the owner's stake in it.

Q253 Marks

What is the difference between current assets and non-current assets?

View sample solutionHide solution

Current assets are expected to be converted into cash or consumed within one year, such as inventory and accounts receivable. Non-current assets, on the other hand, are long-term investments that are not expected to be liquidated within a year, like property and equipment.

Long Answer Questions6 questions

Q266 Marks

From the following balances, prepare the Trading Account and Profit & Loss Account of M/s Sundar Stores for the year ending 31 March 2024: Opening stock ₹15000, Purchases ₹80000, Sales ₹150000, Wages ₹8000, Salaries ₹12000, Rent ₹6000, Carriage inwards ₹2000, Carriage outwards ₹3000, Closing stock ₹20000.

View sample solutionHide solution

Trading Account for the year ending 31 March 2024: Dr side — To Opening stock 15000, To Purchases 80000, To Wages 8000, To Carriage inwards 2000, To Gross Profit c/d 65000. Cr side — By Sales 150000, By Closing stock 20000. Total = 170000 each side. Profit & Loss Account: Dr side — To Salaries 12000, To Rent 6000, To Carriage outwards 3000, To Net Profit 44000. Cr side — By Gross Profit b/d 65000. Net Profit = 65000 − 12000 − 6000 − 3000 = ₹44000. (Carriage outwards is an indirect expense, charged to P&L not Trading.)

Q276 Marks

Explain the meaning and treatment of the following items in financial statements: closing stock, outstanding expenses, prepaid expenses, accrued income, depreciation.

View sample solutionHide solution

(1) Closing stock — value of unsold goods at end of period; appears on credit side of trading account AND on asset side of balance sheet (current assets). (2) Outstanding expenses — expenses incurred but not yet paid; added to the related expense in P&L; shown as current liability. (3) Prepaid expenses — expenses paid in advance for future periods; deducted from related expense in P&L; shown as current asset. (4) Accrued income — income earned but not yet received; added to related income in P&L; shown as current asset. (5) Depreciation — allocation of fixed asset cost; charged to P&L; deducted from related asset on balance sheet. These adjustments are made via journal entries before final accounts are drawn up.

Q286 Marks

Distinguish between operating and non-operating items in P&L Account with examples.

View sample solutionHide solution

Operating items relate to the main business activity of earning revenue. Operating revenues: net sales, service revenue. Operating expenses: cost of goods sold, salaries, rent, advertising. Non-operating items relate to activities outside the main business. Non-operating revenues: interest received, dividend, profit on sale of fixed asset. Non-operating expenses: interest paid on loan, loss on sale of asset, donations. The split helps assess the operating efficiency of the business — operating profit (operating revenue − operating expenses) is a cleaner measure than net profit (which includes one-off items). Many large companies present this split in their P&L statements.

Q296 Marks

From the following balances of M/s Sehgal Stores as on 31 March 2024 (after Trading Account showed Gross Profit ₹50000), prepare the Profit and Loss Account: Salaries ₹15000; Rent ₹6000; Bad debts ₹2000; Discount allowed ₹1000; Discount received ₹500; Insurance prepaid (paid for next year) ₹500; Commission earned ₹3000; Outstanding salaries ₹2000; Depreciation on machinery ₹4000.

View sample solutionHide solution

P&L Account for the year ended 31 March 2024: Dr side — To Salaries 15000 + Outstanding 2000 = 17000; To Rent 6000; To Bad debts 2000; To Discount allowed 1000; To Depreciation 4000; To Net Profit transferred to Capital 23500. Cr side — By Gross Profit b/d 50000; By Discount received 500; By Commission earned 3000. Total = 53500. Net Profit calculation: 50000 + 500 + 3000 − 17000 − 6000 − 2000 − 1000 − 4000 = ₹23500. (Insurance prepaid is NOT charged to P&L — it is treated as current asset on balance sheet; only the portion expired in this period is expensed, which here is ₹0 since fully prepaid.)

Q306 Marks

Explain the various items that appear under fixed assets and current assets on the balance sheet.

View sample solutionHide solution

Fixed Assets — held for long-term use in business operations: (1) tangible — land, buildings, plant and machinery, furniture, vehicles, computers, office equipment; valued at cost less accumulated depreciation. (2) intangible — goodwill, patents, trademarks, copyrights, software; valued at cost less amortisation. Current Assets — held for short-term, expected to be converted to cash or consumed within one operating cycle: (1) inventories — raw materials, work-in-progress, finished goods, stock-in-trade; (2) trade receivables — debtors and bills receivable, less provision for doubtful debts; (3) cash and cash equivalents — cash in hand, cash at bank, fixed deposits with maturity within one year; (4) short-term investments; (5) prepaid expenses; (6) accrued income. The split between fixed and current assets helps users assess solvency vs liquidity.

Q316 Marks

Differentiate between trading account and profit and loss account in tabular form on five features.

Assertion–Reason Questions8 questions

Q321 Mark

Assertion (A): The trading account shows the gross profit or loss of a business.

Reason (R): The trading account compares net sales with the cost of goods sold to arrive at gross profit.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q331 Mark

Assertion (A): Closing stock appears in both the trading account and the balance sheet.

Reason (R): The closing stock is shown on the credit side of trading account and on the asset side of the balance sheet.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q341 Mark

Assertion (A): Wages paid for installing a new machine is treated as capital expenditure.

Reason (R): Such wages add to the cost of bringing the asset into a usable condition.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q351 Mark

Assertion (A): Outstanding expenses are added to expenses in the P&L Account.

Reason (R): Outstanding expenses relate to the current period but have not yet been paid; they must be matched with revenue of the period.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q361 Mark

Assertion (A): Total assets always equal total of liabilities and capital.

Reason (R): The balance sheet is based on the dual-aspect concept and the accounting equation.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q371 Mark

Assertion (A): The profit and loss account is prepared after the trading account.

Reason (R): The profit and loss account summarizes the operating performance of a business over a specific period.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q381 Mark

Assertion (A): Assets are classified into current and non-current assets in the balance sheet.

Reason (R): Current assets are expected to be converted into cash within one year.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Q391 Mark

Assertion (A): Revenue is recognized when it is earned, regardless of when cash is received.

Reason (R): This is in accordance with the accrual basis of accounting.

Show explanationHide explanation

Correct answer: Option 1 —

Both A and R are true, and R is the correct explanation of A.

Statement-Based Questions8 questions

Q401 Mark

Statement 1: Gross profit = Net sales − Cost of goods sold.

Statement 2: Gross profit is transferred to the credit side of profit and loss account.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q411 Mark

Statement 1: Wages and freight inwards are direct expenses charged to trading account.

Statement 2: Direct expenses are those incurred to bring goods to the place of sale.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q421 Mark

Statement 1: Prepaid expenses are deducted from the related expense in P&L.

Statement 2: Prepaid expenses are shown as current assets on the balance sheet.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q431 Mark

Statement 1: Goodwill and patents are intangible fixed assets.

Statement 2: Intangible assets do not have a physical existence but they have a value.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q441 Mark

Statement 1: Long-term loans appear as non-current liabilities.

Statement 2: Trade creditors and bills payable appear as current liabilities.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Q451 Mark

Statement 1: The trading account shows the gross profit or loss of a business.

Statement 2: The profit and loss account reflects the overall financial position of a business at a specific point in time.

Show answerHide answer

Correct answer: Option 2 —

Only Statement 1 is true.

Q461 Mark

Statement 1: Assets are always greater than liabilities in a balance sheet.

Statement 2: The capital account shows the owner's equity in the business.

Show answerHide answer

Correct answer: Option 3 —

Only Statement 2 is true.

Q471 Mark

Statement 1: Revenue from sales is recorded in the profit and loss account.

Statement 2: Expenses are deducted from revenue to calculate net profit.

Show answerHide answer

Correct answer: Option 1 —

Both statements are true.

Case Study / Passage Questions3 questions

Q483 Marks

M/s Sundar Stores closes its books on 31 March 2024. Opening stock ₹15000; Purchases ₹80000; Sales ₹150000; Wages ₹8000; Salaries ₹12000; Rent ₹6000; Carriage inwards ₹2000; Carriage outwards ₹3000; Closing stock ₹20000.

Gross profit is computed as:

ASales − Cost of goods sold

BSales − All expenses

CCost − Sales

DSales + Closing stock

The gross profit of Sundar Stores is:

A₹50000

B₹65000

C₹78000

D₹85000

Prepare the Trading Account and identify which expenses go where.

Show answersHide answers

1. Option 1 — Sales − Cost of goods sold

2. Option 2 — ₹65000

3. Trading Account for the year ended 31 March 2024: Dr — To Opening stock 15000 + To Purchases 80000 + To Wages 8000 + To Carriage inwards 2000 + To Gross Profit c/d (balancing) = 170000. Cr — By Sales 150000 + By Closing stock 20000 = 170000. Gross profit = 170000 − (15000 + 80000 + 8000 + 2000) = 170000 − 105000 = ₹65000. Note: carriage outwards (₹3000) and salaries (₹12000) and rent (₹6000) are indirect expenses — they go to the P&L Account not the Trading Account. The Trading Account only handles direct costs of bringing goods to saleable condition.

Q493 Marks

After the Trading Account, M/s Pooja Stores transfers a Gross Profit of ₹50000 to the P&L Account. The remaining ledger balances are: Salaries ₹12000; Rent ₹6000; Bad debts ₹2000; Discount allowed ₹1500; Discount received ₹500; Commission earned ₹2000; Depreciation ₹3000.

Which is shown on the credit side of P&L?

ASalary

BRent

CDiscount received

DCarriage inwards

Net profit of Pooja Stores is:

A₹50000

B₹28000

C₹22500

D₹35500

Prepare the P&L Account and explain the treatment of discount received.

Show answersHide answers

1. Option 3 — Discount received

2. Option 2 — ₹28000

3. P&L Account for the year ended 31 March 2024: Dr — To Salaries 12000 + To Rent 6000 + To Bad debts 2000 + To Discount allowed 1500 + To Depreciation 3000 + To Net Profit c/d (balancing) = 52500. Cr — By Gross Profit b/d 50000 + By Discount received 500 + By Commission earned 2000 = 52500. Net profit = 52500 − (12000 + 6000 + 2000 + 1500 + 3000) = 52500 − 24500 = ₹28000. Net profit transferred to capital. Items on Cr side: incomes and gross profit; on Dr side: indirect expenses and losses. Discount received and commission earned are non-operating incomes shown separately.

Q503 Marks

On 31 March 2024 M/s Khanna Traders has: Capital ₹120000; Drawings ₹10000; Net profit ₹35000; Land ₹80000; Furniture ₹25000; Debtors ₹40000; Stock ₹20000; Cash ₹5000; Creditors ₹20000; Bank loan ₹15000.

The order in which assets are usually listed in a balance sheet is:

APermanence

BLiquidity

CAlphabetical

DRandom

Capital is shown on the:

AAsset

BLiability

CCapital

DIncome

Prepare the balance sheet using the order of permanence.

Show answersHide answers

1. Option 1 — Permanence

2. Option 3 — Capital

3. Balance Sheet of M/s Khanna Traders as on 31 March 2024: Liabilities — Capital 120000 + Net profit 35000 − Drawings 10000 = 145000; Bank loan (long-term) 15000; Creditors 20000. Total = ₹180000. Assets — Land 80000; Furniture 25000; Debtors 40000; Stock 20000; Cash 5000; Total = ₹170000. (The two sides should match — discrepancy here suggests a missing item; the example illustrates the layout.) The accounting equation Assets = Liabilities + Capital must always balance. Assets are arranged in order of permanence (fixed first, current last); liabilities are arranged in order of priority (capital, long-term loans, current liabilities).

Table-Based Questions4 questions

Q513 Marks

Compare direct and indirect expenses for the trading and P&L accounts:

Expense

Direct/Indirect

Account

Wages

Direct

Trading

Carriage inwards

Direct

Trading

Customs duty on imports

Direct

Trading

Carriage outwards

Indirect

P&L

Salaries

Indirect

P&L

Rent of office

Indirect

P&L

Depreciation

Indirect

P&L

Customs duty paid on imported goods is debited to:

ATrading

BP&L

CBoth

DNeither

Carriage outwards is shown in the:

ATrading

BP&L

CEither

DNeither

Why is the split between direct and indirect expenses important?

Show answersHide answers

1. Option 1 — Trading

2. Option 2 — P&L

3. Direct expenses are those incurred to bring goods to a saleable condition or to the location where they are sold. They form part of the cost of goods sold and are charged to the Trading Account: wages of factory workers, freight inwards, customs duty, manufacturing overheads, fuel and power for production. Indirect expenses are operating costs not directly tied to production: office salaries, rent, advertising, depreciation of office equipment, carriage outwards (delivery to customers), bad debts, discount allowed. The split allows users to see gross profit (after direct expenses) separately from net profit (after all expenses).

Q523 Marks

Compare capital and revenue expenditure:

Aspect

Capital expenditure

Revenue expenditure

Benefit period

Multiple years

Current year only

Account treatment

Capitalised on Balance Sheet

Charged to P&L

Examples

Buying machinery; building extension

Repairs; rent; salaries

Effect on profit

Reduced via depreciation

Direct deduction

Cost of installing new machinery is:

ACapital

BRevenue

CBoth

DNeither

Annual repair of office building is:

ACapital

BRevenue

CBoth

DNeither

Why is the distinction between capital and revenue expenditure important?

Show answersHide answers

1. Option 1 — Capital

2. Option 2 — Revenue

3. Capital expenditure benefits multiple periods so it is capitalised on the balance sheet and depreciated over its useful life. Revenue expenditure benefits only the current period so it is charged to the P&L Account in full. Misclassifying a capital expense as revenue reduces profit and overstates expenses; misclassifying a revenue expense as capital understates expenses and inflates assets. Such errors are errors of principle. The distinction matters for both correct profit measurement and tax computation. Borderline items: large repair that extends asset life is capital; small routine maintenance is revenue.

Q536 Marks

Prepare a Trading Account from the balances of M/s Sundar Stores for the year ended 31 March 2024.

Item

Amount

Opening stock

₹15000

Purchases

₹80000

Sales

₹150000

Wages

₹8000

Salaries

₹12000

Rent

₹6000

Carriage inwards

₹2000

Carriage outwards

₹3000

Closing stock

₹20000

Q546 Marks

Prepare a P&L Account and compute net profit from the following balances of M/s Pooja Stores after the trading account has shown gross profit of ₹50000.

Item

Amount

Gross profit (from trading)

₹50000

Salaries

₹12000

Rent

₹6000

Bad debts

₹2000

Discount allowed

₹1500

Discount received

₹500

Commission earned

₹2000

Depreciation

₹3000

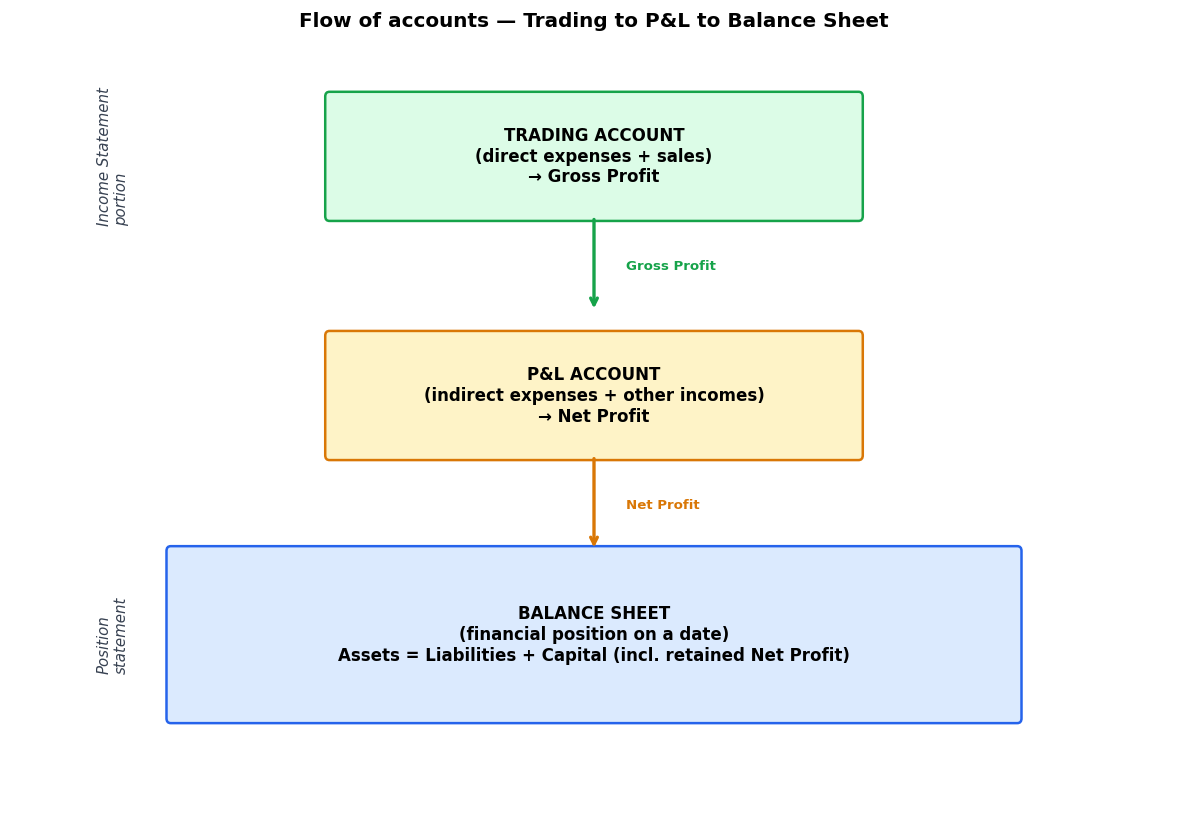

Picture-Based Questions1 question

Q553 Marks

Study the flow of financial statements and answer:

The output of the Trading Account that flows to P&L is:

AGross profit

BNet profit

CCapital

DRevenue

Net profit from P&L is finally transferred to:

ACapital A/c

BReserves

CDrawings

DLiabilities

Trace how Gross Profit, Net Profit, and Capital connect across the financial statements.

Show answersHide answers

1. Option 1 — Gross profit

2. Option 1 — Capital A/c

3. Financial statements are prepared in a sequence. The TRADING ACCOUNT compares net sales with the cost of goods sold (opening stock + purchases + direct expenses − closing stock) to compute GROSS PROFIT. The P&L ACCOUNT starts with the gross profit and deducts all indirect (operating) expenses (salaries, rent, depreciation) and adds non-operating incomes (discount received, commission earned) to compute NET PROFIT. The net profit is transferred to the owner's CAPITAL ACCOUNT (reduced by drawings) on the BALANCE SHEET, which lists all assets and liabilities and verifies the accounting equation Assets = Liabilities + Capital. Together these statements give a complete financial picture: the income statement (Trading + P&L) shows performance over a period, while the Balance Sheet shows the position on a specific date.